In the realm of personal finance and lifestyle design, real estate often serves as a cornerstone. It represents not only a significant financial investment but also a profound lifestyle choice. As a former realtor, financial advisor, and mortgage agent, I’ve observed numerous clients navigating the intricate balance between these two aspects. This article explores the delicate equilibrium between financial goals related to real estate and broader lifestyle aspirations, detailing strategies to manage these potentially competing priorities.

Financial Goals in Real Estate

The Conflict: When Financial and Lifestyle Goals Collide

The Continuum of Focus: Financial Goals vs. Lifestyle Goals

Personal Stories: Real Examples

Navigating the Balance: Mortgage Choices and Lifestyle Goals

Examples of Balancing Mortgage Choices and Lifestyle Goals

Financial Goals in Real Estate

For many, financial goals around real estate involve purchasing a home, investing in rental properties, or buying vacation homes. These goals are often driven by the desire for financial security, asset accumulation, and wealth building through appreciation and equity.

Financial Goals

When it comes to acquiring a house, individuals often have a diverse range of financial goals that reflect their personal circumstances, aspirations, and stages of life. Here are some common financial goals people may have around getting a house:

- Homeownership as an Investment: Many view purchasing a house as a long-term investment. The goal is to build equity over time as property values increase and through gradual repayment of the mortgage.

- Stability and Security: Owning a home can provide a sense of stability and security, as it eliminates uncertainties related to renting, such as lease renewals and rent increases.

- Wealth Accumulation: For some, buying a house is a key strategy for wealth accumulation, especially as they consider paying down a mortgage as a form of forced savings which increases their net worth.

- Rental Income: Purchasing a property with the intent to rent it out, either as a primary residence with additional units or as a separate investment property, to generate ongoing passive income.

- Downsizing or Upsizing: Depending on life stages, such as retirement or growing family needs, individuals might aim to downsize for more manageable living and maintenance costs or upsize to accommodate more family members.

- Debt Consolidation: Some might see home equity as a means to consolidate high-interest debts under a lower interest rate, utilizing home equity loans or refinancing options.

- Tax Efficiency: Utilizing the tax advantages associated with homeownership, such as deductions for mortgage interest and property taxes in some regions, can be a significant financial goal.

- Equity Release: Older homeowners might consider strategies like a reverse mortgage to release the equity in their homes while still living there, to supplement their retirement income.

- Customization and Control: Owning a home offers the freedom to customize and remodel the property according to personal tastes and needs without requiring a landlord’s approval.

- Legacy and Estate Planning: For many, a home is seen as a family asset that can be passed down to future generations as part of their estate.

- Financial Flexibility: Building equity in a home can provide financial flexibility, allowing homeowners to access funds for other significant expenses through home equity lines of credit or loans.

- Escape from Renting: Simply escaping the rental cycle and the associated costs is a primary goal for many first-time home buyers. This change can often lead to better financial predictability and personal satisfaction.

These goals can vary greatly based on individual financial situations, life goals, and the economic environment, but they collectively underscore the significance of homeownership in personal financial planning.

Lifestyle Goals

Conversely, lifestyle goals might include travel, career flexibility, family time, or pursuing hobbies and passions that require significant time and financial resources. Homeownership, with its associated costs and maintenance, can potentially restrict these lifestyle pursuits due to the financial and time commitments it demands.

Life & Lifestyle Goals

When it comes to life goals, individuals have a wide array of aspirations that encompass personal, professional, financial, and emotional aspects of their lives. Here are various life goals that people may pursue:

- Career Advancement: Achieving specific professional milestones, climbing the corporate ladder, or becoming a recognized expert in a chosen field.

- Financial Independence: Reaching a point where one no longer needs to work to maintain their lifestyle, often through saving, investing, or building passive income streams.

- Starting a Family: For many, a major life goal is to marry, have children, and nurture a healthy family environment.

- Education and Learning: Pursuing higher education, obtaining degrees, certifications, or simply committing to lifelong learning and personal development.

- Health and Wellness: Maintaining or achieving good physical health through diet, exercise, and healthy living, or finding mental and emotional balance.

- Travel and Adventure: Experiencing different cultures, visiting remote or significant locations around the world, or engaging in adventure sports.

- Home Ownership: Buying a house or creating a dream home, which often represents stability and personal achievement.

- Creative Pursuits: Writing a book, producing music, or engaging in any form of artistic expression as a significant personal accomplishment.

- Community Service: Giving back to the community through volunteering, starting a nonprofit, or engaging in activism to support a cause.

- Spiritual Growth: Pursuing spiritual or religious goals, which could include a deeper understanding of a faith, going on a pilgrimage, or living a life according to spiritual principles.

- Environmental Impact: Living a sustainable life, reducing one’s carbon footprint, or contributing to conservation efforts.

- Entrepreneurship: Starting a business or becoming self-employed to pursue personal passions and achieve financial success.

- Retirement Planning: Preparing for a comfortable and fulfilling retirement, including financial planning, lifestyle choices, and perhaps relocation.

- Personal Relationships: Building lasting and meaningful relationships with friends and family, finding a life partner, or enriching current relationships.

- Personal Achievement: Completing a personal challenge, such as running a marathon, learning a new language, or achieving a personal best in a hobby or sport.

- Legacy Creation: Leaving a meaningful impact on the world, whether through one’s professional work, philanthropy, or by raising children who contribute positively to society.

Each of these goals can significantly shape an individual’s life trajectory and provide a sense of purpose and fulfillment. People often pursue a combination of these goals, which may evolve over time as their circumstances and perspectives change.

The Conflict: When Financial and Lifestyle Goals Collide

The pursuit of homeownership can sometimes clash with lifestyle aspirations. For example, owning a large home might secure a financial asset but could limit travel due to mortgage payments and maintenance costs. Similarly, living in a high-cost area might offer career opportunities but could delay homeownership or require compromises on lifestyle choices like travel or leisure activities.

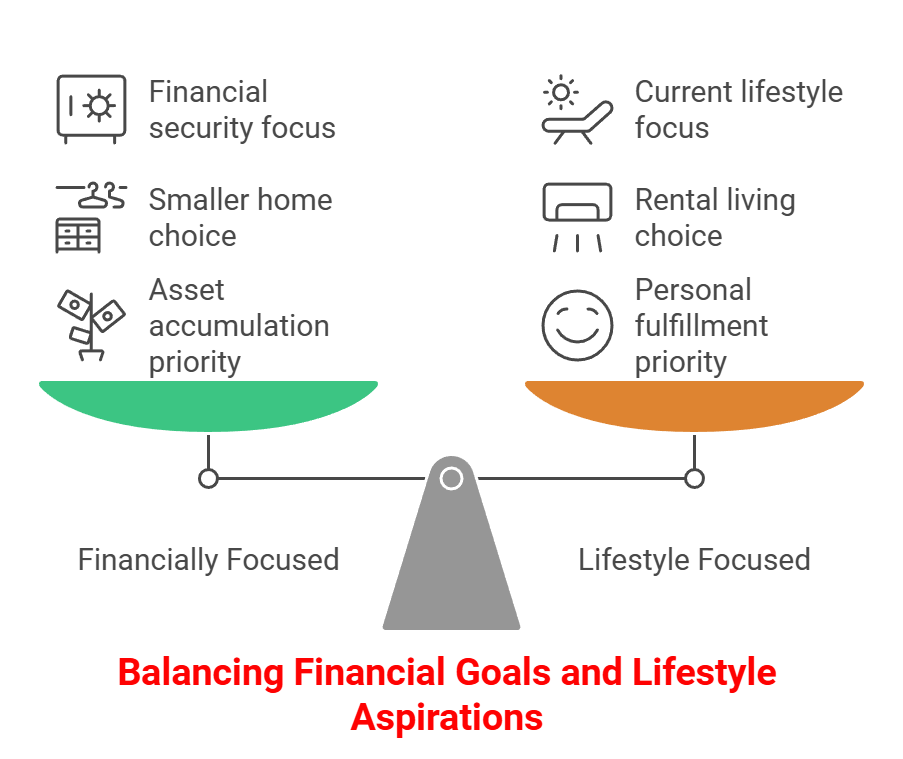

The Continuum of Focus: Financial Goals vs. Lifestyle Goals

Individuals tend to fall somewhere on a continuum between being highly focused on financial goals and being primarily driven by lifestyle aspirations.

- Financially Focused Individuals: These are often investors or savers who prioritize asset accumulation and long-term wealth. They might opt to live in smaller homes or less desirable locations to save and invest more aggressively. Their life choices are frequently dictated by financial considerations, sometimes at the expense of personal satisfaction or immediate lifestyle enjoyment.

- Lifestyle Focused Individuals: These individuals prioritize personal fulfillment, experiences, and quality of life over financial gains. They may choose rental living to avoid the burdens of homeownership, invest in travel, or opt for careers that offer more flexibility and less income. They accept that they may sacrifice long-term financial security for current lifestyle preferences.

- Balanced Approach Advocates: Many strive to find a middle ground, seeking both financial security and fulfilling lifestyles. They might buy homes within their means to keep mortgage costs manageable while still budgeting for travel and leisure. They aim to build wealth slowly without sacrificing significant lifestyle desires.

Personal Stories: Real Examples

Case Study 1: John – The Financial Strategist

John, a 45-year-old software developer, chose to invest in multiple rental properties early in his career. His focus on accumulating assets meant living in smaller, less expensive homes and prioritizing investments over vacations or luxury expenditures. John’s portfolio now provides significant passive income, allowing him more financial freedom as he approaches retirement.

Case Study 2: Sarah – The Lifestyle Pursuer

Sarah, a 30-year-old freelance graphic designer, values flexibility and travel above homeownership. She rents a modest apartment in a vibrant city, using her income to fund regular international trips and art courses. Sarah’s retirement savings are minimal, but she prioritizes experiences over financial growth, accepting the potential long-term implications.

Case Study 3: Alex and Jamie – Balancing Act

Alex and Jamie, a couple in their mid-thirties, carefully chose a home that would not stretch their budget, preserving funds for their passions—culinary classes and photography. They contribute regularly to their retirement accounts and maintain an emergency fund, but they also ensure they live a rich, experience-filled life.

Strategies for Balancing Financial and Lifestyle Goals

Goal Setting and Prioritization

Clear, specific goals are crucial. Individuals must identify what they value most—security, wealth, experiences, or flexibility—and plan accordingly. Regular goal reviews are essential to adapt to life’s changes.

Flexible Financial Planning

A flexible financial plan that can evolve with changing priorities and circumstances is vital. This might include choosing less aggressive investments that allow for more liquidity to fund lifestyle needs.

Continuous Learning and Adjustment

Life is dynamic, and so are our desires and needs. Continuously learning about personal finance and lifestyle design can help individuals make informed decisions that align with their evolving goals.

Navigating the Balance: Mortgage Choices and Lifestyle Goals

When considering how to balance financial goals with lifestyle aspirations, the choice of mortgage products plays a pivotal role. Different mortgage options, such as the type of interest rate, prepayment privileges, and amortization periods, can significantly influence one’s financial flexibility and ability to pursue broader life goals. Understanding the interplay between these choices can help homeowners make decisions that align with their overall life plans.

Variable vs. Fixed-Rate Mortgages

Variable Rate Mortgages: Variable mortgages have historically come with lower interest rates compared to fixed-rate mortgages (except during financial periods where the yield curve is inverted), providing a period of lower payments.

Variable rate mortgages come in two varieties: adjustable rate mortgages and variable rate mortgages. For adjustable-rate mortgages, when the interest rate changes, the mortgage payment amount is recalculated to reflect the new rate. This means that if interest rates rise, the borrower’s monthly payment will increase, and if rates fall, the payment will decrease. While this provides less payment stability, it can create opportunities to pay down the mortgage faster or re-allocate holdings. For variable-rate mortgages, the interest rate also fluctuates based on changes in the lender’s prime rate. However, the key difference is that the monthly payment amount typically remains constant, enabling better budgeting, particularly for people who have less disposable income.

Variable rate mortgage varieties can be particularly appealing for those prioritizing either current lifestyle or financial goals, such as travelling or investing. However, the uncertainty associated with potential rate increases can be a significant factor for those who value financial stability and predictability.

Fixed-Rate Mortgages: Offering predictability and stability, fixed-rate mortgages are suitable for those who prioritize long-term budgeting certainty. This is particularly beneficial for individuals who are financially focused, as it helps in planning long-term investments and savings without worrying about fluctuating mortgage costs.

Amortization Periods

Shorter Amortization: Opting for a shorter amortization period typically means higher monthly payments, which can limit monthly cash flow but result in faster equity building and less interest paid over the life of the loan. This choice might appeal to financially focused individuals who are intent on quickly growing their equity and reducing debts.

Longer Amortization: A longer amortization period lowers monthly payments, providing more monthly disposable income that can be used for lifestyle pursuits such as travel, hobbies, or higher day-to-day living standards. However, this comes at the cost of paying more interest over time.

Prepayment Privileges

Prepayment options allow homeowners to pay off their mortgage faster without incurring penalties. These can include lump-sum payments or increasing regular payment amounts.

Financially Oriented Homeowners: Those with extra income who are focused on reducing debt quickly may leverage prepayment privileges to decrease their mortgage principal before term, saving on interest and increasing equity.

Lifestyle-Oriented Homeowners: Individuals who prefer maintaining liquidity for lifestyle expenditures might opt not to use prepayment privileges extensively, keeping their funds available for immediate use in lifestyle pursuits.

Refinancing and Home Equity Lines of Credit (HELOCs)

Refinancing: This can be a strategic tool for those looking to take advantage of lower interest rates or pull out equity for large expenses such as home renovations, which can enhance one’s living environment and lifestyle.

HELOCs: Providing flexible access to funds based on home equity, HELOCs can be used for significant lifestyle expenditures, such as funding a sabbatical or a major travel adventure, while also serving as an emergency fund or investment tool.

Examples of Balancing Mortgage Choices and Lifestyle Goals

- Example 1: John opts for a fixed-rate mortgage to stabilize his monthly expenses, allowing him to plan his long-term financial investments without the worry of changing mortgage costs.

- Example 2: Sarah chooses a variable rate mortgage with a longer amortization period, maximizing her cash flow to support her travel and freelance career, accepting the risk of potential rate increases for greater financial flexibility today.

- Example 3: Alex and Jamie take advantage of prepayment privileges by making annual lump-sum payments when they receive bonuses, which helps them balance between reducing their mortgage term and enjoying their lifestyle hobbies.

Choosing the right mortgage product involves a careful assessment of one’s financial situation, lifestyle aspirations, and risk tolerance. By understanding the various features and implications of different mortgage options, individuals can make informed decisions that support both their financial stability and lifestyle goals, achieving a personalized balance that aligns with their overall life vision.

Summary

The balance between financial objectives and lifestyle goals is deeply personal and varies widely among individuals. By understanding where they fall on the continuum and what sacrifices they are willing to make, individuals can better navigate the path to a fulfilling life that honors both their financial realities and their lifestyle dreams.