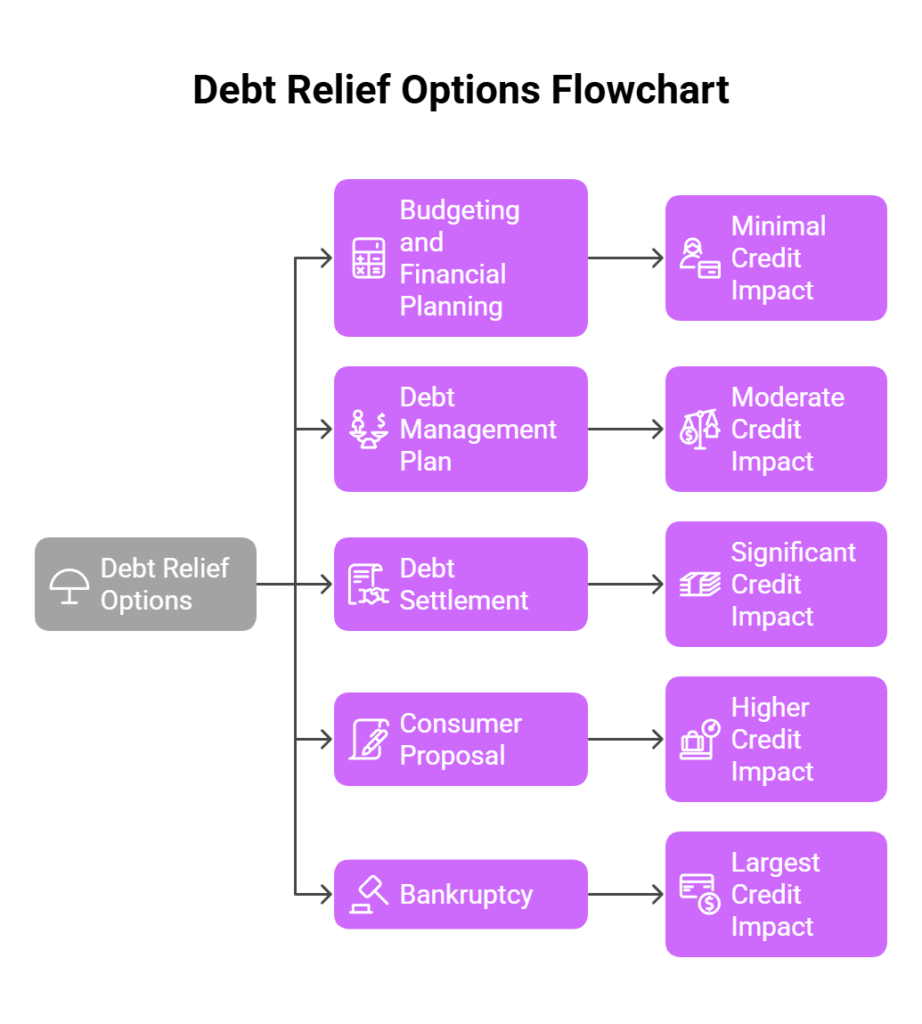

Managing overwhelming debt can feel intimidating, but Canada offers several debt-relief solutions tailored to varying financial situations. Each option comes with distinct implications for your credit score and overall financial health. Here, we outline key solutions—Budgeting and Financial Planning, Debt Management Plans, Debt Settlement, Consumer Proposals, and Bankruptcy—from the smallest to largest in terms of credit impact and severity.

Budgeting and Financial Planning (Minimal Credit Impact)

Debt Management Plan (Moderate Credit Impact)

Debt Settlement (Significant Credit Impact)

Consumer Proposal (Higher Credit Impact, Formal Solution)

Bankruptcy (Largest Credit Impact, Formal Solution)

Debt Relief Option Mortgage Impact

Budgeting and Financial Planning (Minimal Credit Impact)

Budgeting and financial planning is the least invasive debt solution, best suited for individuals experiencing minor financial stress. It involves careful monitoring of expenses, disciplined spending, and proactive debt repayment.

Scenario: If your debt is manageable and you have steady income but struggle with poor spending habits, creating a detailed budget and financial plan may resolve your debt issues without negatively affecting your credit.

Debt Management Plan (Moderate Credit Impact)

A Debt Management Plan (DMP) consolidates multiple unsecured debts into one manageable monthly payment through a credit counselling agency. Interest rates are often reduced or eliminated.

Key features:

- Full repayment of debt over 3-5 years

- Informal creditor cooperation (no legal protections)

- Moderate initial credit impact that improves with consistent payments

Scenario: A DMP is ideal if you have consistent income but face difficulties managing multiple high-interest debts. It simplifies repayment and provides financial education to prevent future issues.

Debt Settlement (Significant Credit Impact)

Debt settlement involves negotiating directly with creditors to repay less than you owe, typically in a lump-sum payment. It’s informal, meaning no legal protections exist during the negotiation process.

Key features:

- Immediate lump-sum settlements at reduced amounts

- No guarantee of creditor acceptance

- Significant short-term credit damage

Scenario: If you have substantial unsecured debts in collections and can secure immediate funds, debt settlement could quickly resolve these obligations, though at the expense of your credit rating.

Consumer Proposal (Higher Credit Impact, Formal Solution)

A consumer proposal is a formal, legally binding agreement prepared by a Licensed Insolvency Trustee (LIT). It enables you to repay a reduced portion of your total debts over up to five years, with immediate protection from creditors.

Key features:

- Legally binding and immediately stops creditor actions

- Debt reduction typically ranging from 30% to 50%

- Remains on credit report for three years after completion

Scenario: Choose a consumer proposal when your debt significantly exceeds your repayment capabilities, but you have sufficient income to repay at least a portion of it. This solution provides strong legal protections and meaningful debt relief.

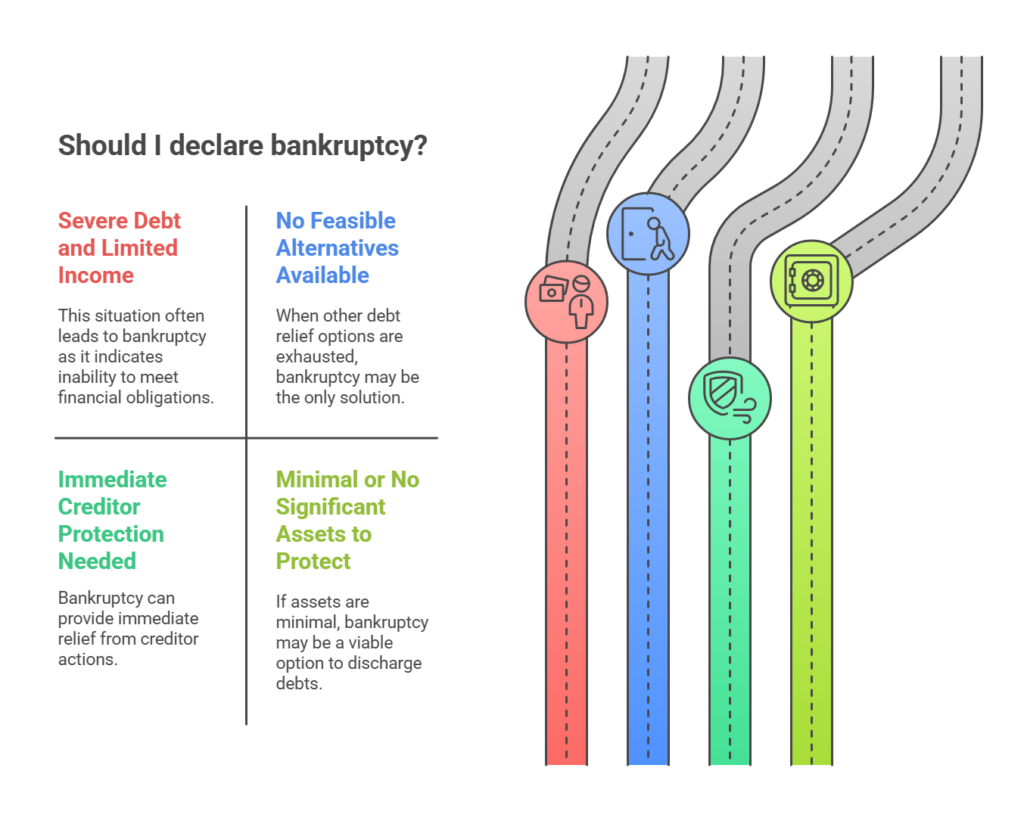

Bankruptcy (Largest Credit Impact, Formal Solution)

Bankruptcy is the most severe debt-relief solution, offering complete discharge of eligible debts but carrying the greatest impact on your credit and assets. It is also administered by an LIT.

Key features:

- Full discharge of eligible unsecured debts

- Immediate and strong legal protection from creditors

- Severe and lasting negative impact on credit (6-14 years)

Scenario: Bankruptcy is suitable when your debts vastly outweigh your income, you lack significant assets, and no other debt solutions are feasible. It offers an immediate fresh start but has long-term implications for credit and financial opportunities.

Debt Relief Option Mortgage Impact

Here’s my analysis of how each debt relief option impacts your mortgage applications:

- Budgeting and Financial Planning (Minimal Impact)

- Debt Management Plan (Moderate Impact)

- Debt Settlement (Significant Impact)

- Consumer Proposal (Higher Impact, Formal Solution)

- Bankruptcy (Largest Impact, Formal Solution)

Budgeting and Financial Planning (Minimal Impact)

Budgeting and financial planning typically have minimal or no negative impact on mortgage applications. In fact, proactively managing your debt through disciplined budgeting is viewed positively by lenders, demonstrating strong financial responsibility and stability. Mortgage lenders are more likely to approve applications from borrowers who exhibit controlled financial behaviours and steady debt repayment.

Debt Management Plan (Moderate Impact)

A Debt Management Plan (DMP) has a moderate effect on your ability to secure a mortgage. While participation in a DMP is noted on your credit report and may initially lower your credit score, lenders generally perceive it more positively than other severe debt relief options. A DMP shows you’re proactively managing and repaying debt fully over a structured period. However, traditional lenders may still require that your DMP is completed or nearly completed before approving a mortgage, and they may request a larger down payment or offer higher interest rates.

Debt Settlement (Significant Impact)

Debt settlement significantly impacts mortgage applications because it indicates debts were not repaid in full. Creditors typically report accounts as “settled for less than full balance,” negatively affecting your credit score and raising red flags for mortgage lenders. Even after settling, lenders may perceive you as a higher-risk borrower, necessitating higher down payments, elevated interest rates, or turning to alternative lenders instead of traditional financial institutions. To regain mortgage eligibility post-settlement, consistent credit rebuilding is essential.

Consumer Proposal (Higher Impact, Formal Solution)

Consumer proposals have a substantial impact on your mortgage application due to their formal nature and the reduction in total debt owed. This option remains on your credit report for three years following completion. Many traditional lenders typically require at least two years of re-established credit following the completion of a consumer proposal before considering mortgage applications. Alternative lenders might consider you sooner, but they typically impose higher interest rates and fees to compensate for perceived risk. Demonstrating consistent credit rebuilding and stable income is crucial to mortgage approval post-proposal.

Bankruptcy (Largest Impact, Formal Solution)

Bankruptcy has the most severe impact on your mortgage prospects. It dramatically reduces your credit score, remains on your credit report for 6 to 14 years (depending on whether it’s a first or second bankruptcy), and is viewed by lenders as the most significant credit risk. Most traditional lenders typically require a minimum waiting period of at least two years after bankruptcy discharge before approving a mortgage application. Some won’t look at a borrower at all if there is a history of bankruptcy. Alternative or private lenders may offer financing sooner but usually at substantially higher interest rates and require significant down payments (often 20% or more). Demonstrating strong financial recovery—stable employment, rebuilt credit, substantial savings—is essential for mortgage approval post-bankruptcy.

Summary

The best debt relief option depends on your unique financial circumstances. Solutions range from informal budgeting strategies with minimal credit impact to formal processes like bankruptcy, which provide strong protection and complete debt elimination but at a greater cost to your financial reputation.

Assess your situation thoroughly and consult a Licensed Insolvency Trustee or credit counselling professional to determine which approach aligns best with your needs, financial goals, and capacity to rebuild your financial future.