When it comes to securing real estate financing, especially in complex or time-sensitive situations, finding the right lender is critical. As a licensed and experienced mortgage agent, I take pride in introducing my clients to trustworthy lending options that might not yet be household names — but deserve to be.

I am excited to introduce you to Premiere Mortgage, a highly respected private lender with a long-standing track record of success, flexibility, and exceptional service. Established in 1985 and celebrating 40 years in business, Premiere Mortgage is licensed to lend across Ontario, British Columbia, and Alberta. Their reputation, expertise, and genuine client-first approach make them a valuable resource in today’s competitive market.

Who is an Ideal Client for Premiere Mortgage?

How Premiere Mortgage Stands Apart

Who is Premiere Mortgage?

Premiere Mortgage is a well-established private mortgage lender, specializing in equity-based residential and commercial lending. As a private lender, Premiere is not bound by the rigid lending rules imposed on banks or traditional financial institutions. This independence means they can focus on the true value of the property, the overall strength of the deal, and the client’s future potential — rather than solely on credit scores, income documents, or strict debt servicing ratios.

For clients, working with a private lender like Premiere Mortgage implies faster decisions, greater flexibility, creative solutions, and access to financing even when conventional lenders say no. It also means personalized service from underwriters who are empowered to assess every situation with common sense rather than inflexible formulas.

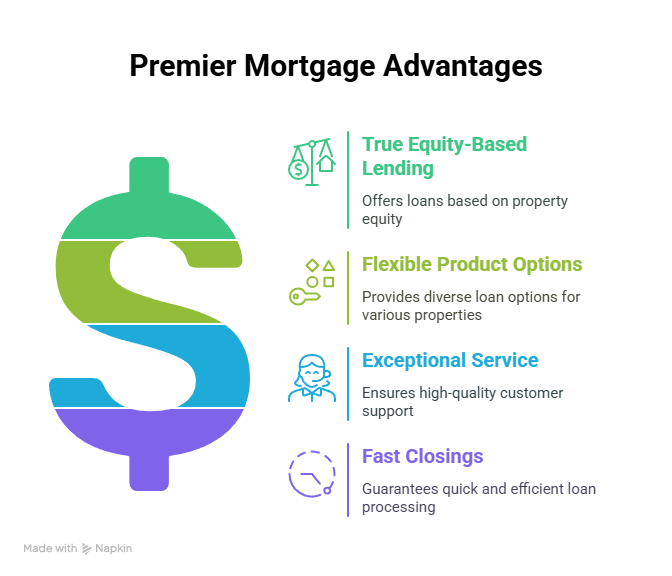

Why Choose Premiere Mortgage?

Here are three powerful reasons why borrowers should seriously consider working with Premiere Mortgage:

- True Equity-Based Lending

- Flexible Product Options for Urban and Rural Properties

- Exceptional Service and Fast Closings

True Equity-Based Lending

Premiere Mortgage stands apart as a true equity lender, meaning their lending decisions are based primarily on the value and quality of the real estate — not the client’s income, employment status, or credit score.

- No minimum credit scores required. Whether a client has bruised credit, is in a consumer proposal, or even undergoing bankruptcy, Premiere looks at the property value and the deal’s overall strength.

- No traditional income verification needed. They use a common-sense approach — sometimes asking for bank statements to establish affordability — but not requiring Notice of Assessments (NOAs), T1 Generals, or pay stubs.

This opens up opportunities for clients who would otherwise be shut out by traditional lenders.

Flexible Product Options for Urban and Rural Properties

Premiere offers flexible first and second mortgages on both urban and rural properties, including:

- Residential homes (urban and small towns)

- Small acreages and agricultural properties (non-working farms)

- Select recreational properties

- Commercial condo units and small warehouse spaces

- Residential building lots (land-only financing)

They offer fully open options for faster refinancing opportunities, and their tiered pricing allows clients to choose lower rates with fees, or no-fee options with slightly higher rates — depending on their needs. This structure ensures clients have real choices to best fit their situation.

Exceptional Service and Fast Closings

Premiere Mortgage is committed to delivering quick, reliable service.

- Initial responses within 2–4 business hours.

- Written quotes with three clear options for every deal.

- Closings in as little as five business days when necessary — critical for urgent files like power of sale redemptions or purchases needing fast action.

Furthermore, Premier’s dedicated underwriting team personally manages files, ensuring that brokers and clients alike receive attentive, knowledgeable support every step of the way.

Who is an Ideal Client for Premiere Mortgage?

Premiere Mortgage specializes in helping borrowers who:

- Are self-employed and show little verifiable income on paper.

- Have damaged credit, collections, judgments, or bankruptcies.

- Are new to Canada without strong Canadian credit histories.

- Require equity take-outs for debt consolidation, CRA payouts, or urgent needs.

- Need fast closings where banks or trust companies cannot meet deadlines.

- Are purchasing, refinancing, or investing in small-town properties or properties with wells or septic systems.

- Require second mortgages behind an existing first mortgage to access additional equity.

In essence, Premiere is ideal for clients who have strong equity but face challenges with traditional mortgage qualification.

How Premiere Mortgage Stands Apart

There are many private lenders in the market, but Premiere Mortgage distinguishes itself in several important ways:

- Longevity and Reputation: 40 years of lending experience with a strong reputation for fairness and reliability.

- Broker-Friendly Model: Brokers retain full control over their fees (within prudent limits), and Premiere supports brokers with immediate funding upon deal closing.

- Client-Focused Renewals: At renewal, clients are not automatically penalized; fees, if any, are capitalized onto the mortgage balance instead of being required upfront.

- Commitment to Exit Strategy: Premiere actively works with brokers and clients to create strategies that allow clients to graduate back to traditional financing when ready.

Their consistent focus is not just on “holding” a loan but on helping clients move forward financially.

My Final Thoughts

As a professional mortgage agent, my responsibility is to open the right doors for my clients — even when the path is not a straight line. Premiere Mortgage offers a refreshing, pragmatic, and client-focused option for borrowers who need flexible solutions.

If you or someone you know needs financing where banks have said no — whether due to credit challenges, income structure, or property type — Premiere Mortgage could be the perfect partner to make the deal happen.

Feel free to reach out to me anytime to discuss how Premiere Mortgage can fit into your real estate financing plan.