Comparing BMO Homeowner ReadiLine, Scotiabank STEP, and TD Equity FlexLine

The Smith Maneuver is a popular financial strategy in Canada designed to convert non-deductible mortgage debt into tax-deductible investment debt, helping homeowners accelerate wealth creation and reduce their tax liabilities. Successfully executing this manoeuvre requires a specific type of mortgage known as a readvanceable mortgage, combining a traditional mortgage with a home equity line of credit (HELOC).

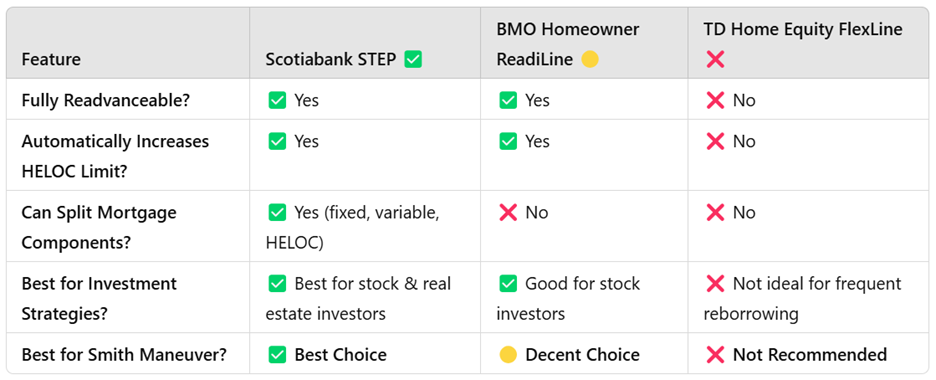

Three popular Canadian mortgage products fit this description: the BMO Homeowner ReadiLine, Scotiabank STEP (Scotia Total Equity Plan), and TD Home Equity FlexLine. However, among these three options, one clearly stands out as the most suitable for implementing the Smith Maneuver effectively.

The Best Choice: Scotiabank STEP Mortgage

Where Do the Other Mortgages Fall Short?

Example Scenario: Executing the Smith Maneuver with the Scotiabank STEP Mortgage

The Best Choice: Scotiabank STEP Mortgage

Among the three options, the Scotiabank STEP mortgage is the most advantageous for homeowners looking to leverage the Smith Maneuver. This mortgage stands out primarily because of its fully readvanceable nature, flexibility, and its ability to segment borrowing into multiple loan components.

The STEP mortgage enables borrowers to structure their debt precisely, using distinct portions for personal, business, or investment purposes. As the homeowner pays down the principal on the mortgage, the available HELOC limit automatically and immediately increases. This seamless reborrowing capacity is critical to effectively executing the Smith Maneuver because it allows continual reinvestment without cumbersome reapplication processes.

Additionally, the STEP mortgage offers a unique flexibility advantage by allowing homeowners to combine fixed and variable-rate mortgages under the same umbrella. This ability to mix loan types allows borrowers to balance the security of fixed rates with the potential savings of variable rates, optimizing their financial strategy.

Where Do the Other Mortgages Fall Short?

While both the BMO Homeowner ReadiLine and TD Home Equity FlexLine offer valuable features, they each have specific limitations when it comes to fully realizing the Smith Maneuver.

The BMO Homeowner ReadiLine, although fully readvanceable, does not permit multiple segmented mortgage components. It has only one primary mortgage portion combined with a HELOC. This limitation restricts the homeowner’s ability to separately track and manage personal versus investment debt, making the process less flexible and potentially complicating tax-deduction calculations.

The TD Home Equity FlexLine, while providing access to home equity, is not fully readvanceable in the automatic manner essential to the Smith Maneuver. With TD, homeowners often have to request manual increases to their HELOC, adding a layer of administrative inconvenience and inefficiency. This manual process can hinder continuous investment activities and diminish the effectiveness of the Smith Maneuver.

Example Scenario: Executing the Smith Maneuver with the Scotiabank STEP Mortgage

Consider Sarah and David, a couple who own a $900,000 home with a $720,000 mortgage (after an initial 20% down payment). They aim to leverage the Smith Maneuver to accelerate their retirement savings and reduce tax liability.

They structure their Scotiabank STEP mortgage as follows:

- Mortgage Portion: $500,000 fixed-rate mortgage at 5.2% to maintain predictable monthly payments.

- Variable Mortgage Portion: $120,000 at a variable rate of 5.0%, providing flexibility for market rate advantages.

- HELOC Portion: Initially $100,000 available credit, increasing automatically as the mortgage principal is repaid.

Every month, as Sarah and David make their regular mortgage payments, the principal component reduces their debt, simultaneously increasing the available credit on their HELOC. They immediately access this newly available HELOC credit to invest in tax-efficient portfolios, such as dividend-paying stocks, ETFs, or income-generating rental properties.

As the investments produce income, Sarah and David apply the returns towards their mortgage debt, continuously expanding the available HELOC limit and reinvesting the increased equity. This cyclical process steadily converts non-deductible mortgage debt into deductible investment debt, creating substantial long-term tax benefits and accelerating their wealth-building goals.

Final Thoughts

For Canadian homeowners interested in employing the Smith Maneuver, the Scotiabank STEP mortgage clearly offers the most robust and effective tool. Its fully readvanceable nature, combined with the ability to segment debt strategically, provides the flexibility and functionality critical for the success of this financial strategy. Conversely, the BMO Homeowner ReadiLine and TD Home Equity FlexLine, while useful for other scenarios, lack key features necessary for the optimal execution of the Smith Maneuver.

Homeowners considering this financial strategy should consult with a mortgage professional experienced in the Smith Maneuver to determine the best approach tailored specifically to their financial circumstances and long-term goals.