As a professional mortgage agent committed to finding the best solutions for my clients, I’m always searching for lenders who offer not just competitive products, but also exceptional value through innovation and client-focused service. Today, I’m excited to introduce you to a lender you may not have heard of before — LendHub.

LendHub is an Ontario-based lender with a refreshingly unique offering: fast, equity-based loans with no legal fees, no appraisals, no income documentation, and funding in just 48 to 72 hours. After meeting with their team and exploring their process in depth, I can confidently say they bring a much-needed solution to the Ontario real estate and financing market.

Let me walk you through why LendHub might be the right choice for you or someone you know.

Who Is the Ideal Client for LendHub?

Three Important Reasons Clients Choose LendHub

Who Is LendHub?

LendHub is a private lender based in Ontario, specializing in fast, small-to-mid-size equity loans. As a private lender, LendHub operates outside of the traditional banking system, which means they are not bound by the same regulatory income verification and debt servicing rules as banks and institutional lenders.

This flexibility allows them to focus solely on the property’s equity rather than scrutinizing income documents, employment history, or credit scores.

Private lending, by its nature, offers clients greater speed, flexibility, and accessibility — often stepping in where traditional lenders cannot. With LendHub, clients benefit from straightforward terms, transparent costs, and a genuine commitment to quick and efficient funding, making them a valuable ally in a variety of financial situations.

Who Is the Ideal Client for LendHub?

LendHub’s flexible approach makes them an excellent choice for a wide range of clients, including:

- Homeowners needing small to mid-size loans ($10,000 to $100,000 net) quickly.

- Clients with bruised or imperfect credit. There is no minimum credit score requirement.

- Self-employed individuals who may struggle to prove traditional income.

- Borrowers facing urgent situations like property tax arrears, CRA debts, mortgage arrears, or sheriff eviction notices.

- Clients needing funds for home renovations prior to listing their property.

- Real estate investors needing fast access to equity without disrupting their primary mortgages.

Essentially, if a client owns property in Ontario with available equity — whether in an urban center or a rural town — LendHub can often help where others cannot.

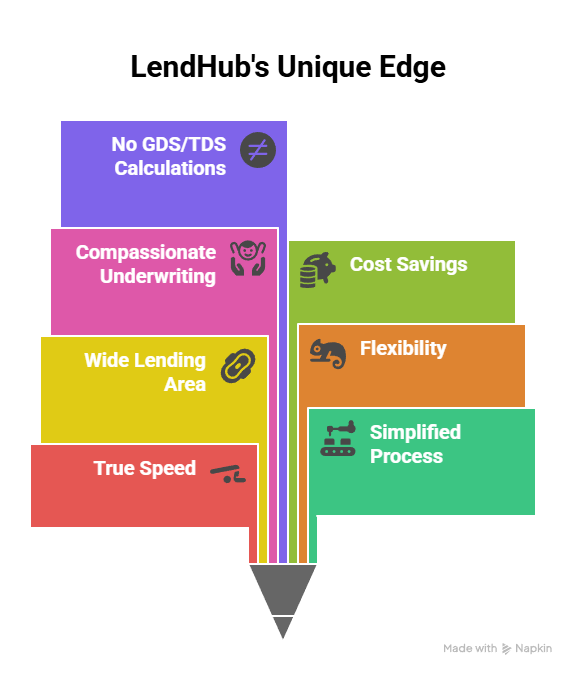

Why LendHub Stands Apart

In a sea of private lenders, LendHub distinguishes itself through several key factors:

- True Speed: Fast funding is not just a marketing promise — it’s their everyday reality. Funds are deposited within 48–72 hours post-commitment.

- Simplified Process: Just two pieces of ID, a recent mortgage statement, and a signed one-page application are required.

- Wide Lending Area: From downtown Toronto to remote rural communities, LendHub funds across all of Ontario.

- Flexibility: They lend behind traditional mortgages, private mortgages, and even reverse mortgages (with an appropriate exit strategy).

- Compassionate Underwriting: Bankruptcies, consumer proposals, and other financial hiccups are not deal-breakers.

- Cost Savings: Particularly on smaller loans ($10,000 to $65,000), LendHub often saves clients significant money when you account for avoided legal, appraisal, and insurance fees.

- No GDS/TDS Calculations: Clients are evaluated on the property and equity alone, not on income or debt servicing ratios.

For clients, realtors, and business owners who need an alternative to traditional, rigid mortgage lending, LendHub is a breakthrough.

Three Important Reasons Clients Choose LendHub

In today’s fast-moving real estate market, having access to reliable, flexible, and efficient financing can make all the difference. LendHub stands out by offering a truly unique combination of speed, simplicity, and transparency that few lenders can match. Whether a client is facing a tight deadline, struggling to navigate the rigid requirements of traditional banks, or simply looking for a straightforward lending experience, LendHub’s approach is designed to meet those needs head-on. Here’s why more and more homeowners, investors, and business owners are turning to LendHub for their real estate financing solutions.

- Speed of Funding — 48 to 72 Hours

- No Legal Fees, No Appraisals, No Income Documents

- True Equity-Based Lending, Open Terms, and Transparency

Speed of Funding — 48 to 72 Hours

Most lenders claim to be fast, but LendHub truly delivers on quick turnaround times. Their simple application process allows approved clients to have funds deposited within just two to three days from a signed commitment. This is invaluable for situations where time is critical, such as stopping a foreclosure, paying urgent debts, or securing a deposit on a new home.

No Legal Fees, No Appraisals, No Income Documents

LendHub’s process eliminates major hurdles that often delay traditional mortgage funding.

- No Legal Costs: They handle registrations in-house.

- No Appraisal Requirements: They rely on automated valuation models (AVMs) instead of formal appraisals.

- No Income Verification: Approval is based purely on equity, not employment status or income paperwork.

This saves clients thousands of dollars in upfront costs and, more importantly, cuts the red tape that often disqualifies good borrowers in today’s tight lending environment.

True Equity-Based Lending, Open Terms, and Transparency

LendHub focuses solely on the value of the property and the borrower’s available equity — not on debt servicing ratios or credit scores.

Their loans are fully open with no early payout penalties, allowing clients to repay whenever they are ready without fear of costly penalties. Moreover, all fees are clearly spelled out at the start, ensuring transparency and peace of mind.

In Closing

As a mortgage professional, my mission is to help clients find real solutions that fit their goals, timelines, and financial needs.

If you — or someone you know — needs fast access to home equity, without the typical headaches of traditional lending, LendHub could be the right partner.

I’m here to answer any questions and walk you through the process from beginning to end, ensuring a smooth, professional experience.

If you would like to explore whether LendHub is right for you, please reach out. Together, we can find the financing solution you deserve.