The Canada Mortgage and Housing Corporation (CMHC) has implemented new mortgage rules for 2024. These rules affect various aspects of the mortgage process, including down payment requirements, qualification criteria, and insurance rules. It is important for Canadian homebuyers to understand these changes to navigate the housing market effectively.

Key Takeaways:

- CMHC has introduced new mortgage rules for 2024 in Canada.

- The changes impact down payment requirements, qualification criteria, and insurance rules.

- Homebuyers need to be aware of these changes to make informed decisions.

- The minimum credit score requirement has been adjusted to 600.

- Non-traditional down payment sources, like borrowed funds, are no longer acceptable.

CMHC New Rules for 2024

The Canada Mortgage and Housing Corporation (CMHC) has implemented new rules for 2024, aiming to manage risk in the housing market. These changes make it more challenging for homebuyers to qualify for CMHC-insured mortgages and have implications for eligibility and borrowing capacity.

Adjustments to Minimum Credit Scores

Under the CMHC’s new rules, the minimum credit score requirement has been adjusted. Previously set at 680, the minimum credit score has now been lowered to 600, providing more flexibility for borrowers to qualify for CMHC-insured mortgages.

Changes in Down Payment Sources

Sources of down payment for CMHC-insured mortgages have also undergone modifications. Borrowers are no longer allowed to borrow money for their down payment, limiting the options to personal funds or non-repayable gifts. This change eliminates the use of non-traditional down payment sources like personal loans.

Adjustment in Debt Service Ratios

The CMHC has made adjustments to the debt service ratios used to assess mortgage affordability. The gross debt service (GDS) ratio, comparing housing costs to income, has been increased from 35% to 39%. Similarly, the total debt service (TDS) ratio, which includes all debt payments, has been increased from 42% to 44%. These changes impact the maximum mortgage amount that borrowers can qualify for.

CMHC Insurance Eligibility and Requirements

To obtain CMHC insurance, certain eligibility criteria and requirements must be met. The property must be located within Canada, with a purchase price or property value of up to $1 million. The minimum down payment is 5% of the first $500,000 and 10% of the remaining amount. The maximum amortization period for CMHC-insured residential mortgages is 25 years.

Understanding and navigating the new rules set by CMHC for 2024 is crucial for potential homebuyers in Canada. These changes in credit scores, down payment sources, debt service ratios, and insurance requirements reshape the landscape for CMHC-insured mortgages, impacting affordability and eligibility. Stay informed to make well-informed decisions in the housing market.

Minimum Credit Score Requirements

One of the key changes in the CMHC mortgage rules for 2024 is the adjustment to the minimum credit score requirement. Previously, the minimum credit score was 680, but it has now been lowered to 600. This means that at least one borrower applying for a CMHC-insured mortgage must have a credit score of 600 or higher to meet the qualification criteria.

Impact on Mortgage Qualification Criteria

The reduction in the minimum credit score requirement opens up opportunities for more borrowers to qualify for CMHC-insured mortgages. With a lower credit score requirement, individuals with a slightly lower credit score can still meet the qualification criteria. This change is particularly beneficial for first-time homebuyers or those with limited credit history.

However, it’s important to note that while the minimum credit score requirement has been lowered, having a higher credit score can still be advantageous. A higher credit score demonstrates a borrower’s ability to manage their finances responsibly and may lead to better mortgage terms, such as lower interest rates.

It’s crucial for potential homebuyers to understand the impact of credit scores on their mortgage eligibility and borrowing capacity. Your credit score is a reflection of your creditworthiness and affects lenders’ confidence in your ability to repay the mortgage loan. Evaluating your credit score and taking steps to improve it can help you secure better mortgage options and potentially save money in the long run.

CMHC Minimum Credit Score Requirements

| Credit Score | Qualification Criteria |

|---|---|

| 600 or higher | Meet the minimum credit score requirement for CMHC-insured mortgages |

| Below 600 | May not meet the qualification criteria for CMHC-insured mortgages |

Understanding the credit score requirements and taking steps to maintain or improve your creditworthiness will ensure a smooth mortgage application process. It’s recommended to regularly check your credit report, pay bills on time, and keep credit utilization low to build a strong credit history.

Changes in Down Payment Sources

The Canada Mortgage and Housing Corporation (CMHC) has recently introduced changes to down payment sources for CMHC-insured mortgages. These changes aim to ensure the integrity of the mortgage process and protect borrowers from excessive debt burdens. Under the new rules, borrowers are no longer permitted to borrow money for their down payment.

Prior to these changes, homebuyers had the option to use non-traditional down payment sources, such as personal loans, to supplement their own funds. However, with the new CMHC guidelines, the down payment must come from the borrower’s own savings or a non-repayable gift.

This adjustment reinforces the importance of responsible financial planning and encourages homebuyers to rely on their own resources when securing a down payment. By ensuring that the down payment comes from the borrower’s own funds, CMHC aims to reduce the risk of default and promote sustainable homeownership.

It’s important for potential homebuyers to be aware of these changes in down payment sources and plan their finances accordingly. By saving diligently and exploring options for non-repayable gifts, prospective homeowners can meet the CMHC requirements and fulfill their dream of owning a home.

Adjustment in Debt Service Ratios

The CMHC’s 2024 mortgage rules introduce changes to the debt service ratios used to assess mortgage affordability. These ratios determine the proportion of your income that can go towards housing costs and overall debt payments.

The two key ratios are the Gross Debt Service (GDS) ratio and the Total Debt Service (TDS) ratio.

Gross Debt Service (GDS) Ratio

The GDS ratio compares your monthly housing costs, including mortgage payments, property taxes, and heating expenses, to your total monthly income. With the new CMHC rules, the GDS ratio has been increased from 35% to 39%. This means that you can allocate a slightly higher percentage of your income towards housing costs while still qualifying for a CMHC-insured mortgage.

Total Debt Service (TDS) Ratio

The TDS ratio considers all of your monthly debt payments, including housing costs, credit card payments, and other loans, in relation to your total monthly income. The CMHC has adjusted the TDS ratio from 42% to 44%, allowing you to have a slightly higher overall debt burden while still meeting the mortgage qualification criteria.

These adjustments in the debt service ratios will impact the maximum mortgage amount for which you can qualify. With higher GDS and TDS ratios, you may have the opportunity to borrow more and increase your affordability.

- The GDS ratio has increased from 35% to 39%.

- The TDS ratio has increased from 42% to 44%.

It is essential to note that while these changes widen the borrowing capacity to some extent, it is crucial to consider your overall financial situation and ensure that you can comfortably manage your monthly payments.

CMHC Insurance Eligibility and Requirements

To obtain CMHC insurance, you must meet specific eligibility criteria and requirements. These ensure that you can benefit from the protection and benefits of CMHC insurance for your mortgage. Let’s take a closer look at the key factors involved:

Location of the Property

Firstly, the property you wish to purchase must be located within Canada. CMHC insurance is specifically designed for Canadian homeowners, providing valuable support for your mortgage journey.

Purchase Price or Property Value

CMHC insurance is available for properties with a purchase price or property value of up to $1 million. This ensures that a wide range of homeowners can access and benefit from mortgage insurance, regardless of their property’s value.

Minimum Down Payment

A minimum down payment is required to be eligible for CMHC insurance. For the first $500,000 of the property’s value, your minimum down payment must be at least 5% of the purchase price. For any remaining amount above $500,000, the minimum down payment required is 10%. Maintaining these minimum down payment requirements is essential to secure CMHC insurance for your mortgage.

Maximum Amortization Period

The maximum amortization period for CMHC-insured residential mortgages is 25 years. This means that your mortgage term cannot exceed this duration if you wish to qualify for CMHC insurance. It’s important to consider and plan for this when exploring your mortgage options.

By meeting these eligibility criteria and requirements, you can ensure that your mortgage is CMHC-insured, providing additional protection and benefits. CMHC insurance offers peace of mind by safeguarding your investment and helping you achieve your homeownership goals.

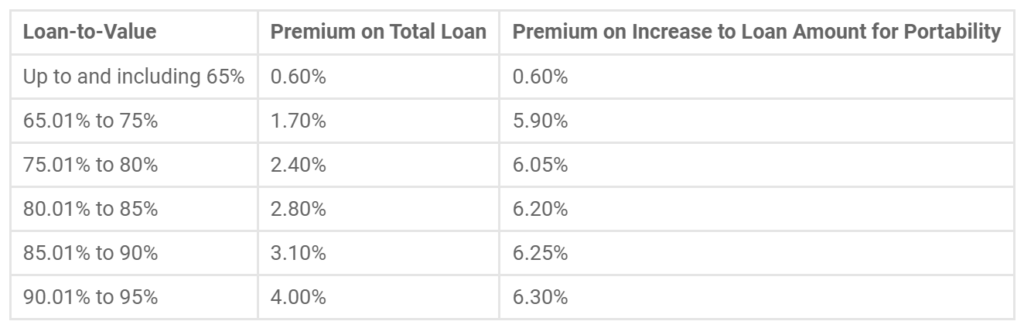

CMHC mortgage loan insurance costs

CMHC Mortgage Loan Insurance information and premium rates.

To obtain CMHC Mortgage Loan Insurance, lenders pay an insurance premium. Typically, your lender will pass these costs on to you. Your lender will give you the exact price when you apply for a mortgage.

The CMHC Mortgage Loan Insurance premium is calculated as a percentage of the loan and is based on the size of your down payment. The higher the percentage of the total house price/value that you borrow, the higher percentage you will pay in insurance premiums.

Remember: without mortgage insurance you may avoid the insurance premium but you’ll typically pay much higher interest rates and additional administrative fees. At the end of the day, for the vast majority of borrowers, the cost of CMHC Mortgage Loan Insurance is more than fully offset by the savings achieved.

CMHC MLI Select for Multi-Unit Properties

When it comes to multi-unit properties with more than five rental units or a minimum of 50 units/beds for retirement homes, the Canada Mortgage and Housing Corporation (CMHC) provides a specialized mortgage loan insurance product known as CMHC MLI Select. This offering is designed to cater to the unique needs of multi-unit property owners and investors.

CMHC MLI Select introduces a point scoring system that rewards borrowers for meeting specific criteria related to affordability, energy efficiency, and accessibility. By satisfying these requirements, borrowers have the opportunity to unlock additional benefits, such as a higher loan-to-value ratio or a longer amortization period, making it easier to finance their multi-unit properties.

The point scoring system evaluates various aspects of the property and the borrower’s qualifications. For example, properties that meet energy efficiency standards may earn higher points, while features enhancing accessibility could contribute to a higher score. The scoring system encourages borrowers to invest in properties that align with CMHC’s goals of sustainability and affordability.

Criteria for CMHC MLI Select

To qualify for CMHC MLI Select, borrowers must adhere to certain criteria. These criteria include:

- A minimum of five rental units or 50 units/beds for retirement homes

- Compliance with energy efficiency standards

- Accessibility features to enhance the property’s inclusivity

- Demonstration of affordability, taking into account rental income and operating costs

Meeting these criteria is essential for borrowers aiming to take advantage of the benefits offered by CMHC MLI Select. By aligning with CMHC’s objectives, borrowers can access mortgage loan insurance tailored to their multi-unit properties, ensuring financial security and peace of mind.

| Benefits of CMHC MLI Select | Eligibility Criteria |

|---|---|

| Higher loan-to-value ratio | Minimum of five rental units or 50 units/beds for retirement homes |

| Longer amortization period | Compliance with energy efficiency standards |

| Enhanced affordability | Accessibility features to enhance inclusivity |

CMHC MLI Select provides borrowers with a tailored mortgage loan insurance solution designed specifically for multi-unit properties. By meeting the necessary criteria and scoring high on the point system, borrowers can access additional benefits that contribute to a more favourable and sustainable financing arrangement.

Conclusion

The implementation of the 2024 CMHC mortgage rules has brought significant changes to the Canadian housing market. These rules have impacted various aspects of the mortgage process, including down payment requirements, credit score criteria, debt service ratios, and insurance eligibility.

By managing risk and ensuring the affordability and accessibility of housing in Canada, these changes aim to create a more stable housing market for both homebuyers and lenders. It is crucial for Canadians looking to buy a home to understand and stay informed about these rules in order to make well-informed decisions.

Whether you are a first-time homebuyer or someone looking to upgrade or invest, being familiar with the CMHC mortgage rules for 2024 will help you navigate the market with confidence. Stay updated on the latest changes, consider the impact these rules may have on your eligibility and borrowing capacity, and consult with mortgage professionals to ensure you are making the right choices for your financial future.

FAQ

What are the CMHC mortgage rules for 2024?

The CMHC has implemented new mortgage rules for 2024, which include changes to down payment requirements, qualification criteria, and insurance rules.

What are the minimum credit score requirements for a CMHC-insured mortgage?

To qualify for a CMHC-insured mortgage, at least one borrower must have a minimum credit score of 600 or higher.

Can I borrow money for my down payment for a CMHC-insured mortgage?

Under the new CMHC rules, borrowers are no longer allowed to borrow money for their down payment. The down payment must come from the borrower’s own funds or a non-repayable gift.

How have the debt service ratios been adjusted under the new CMHC rules?

The gross debt service (GDS) ratio has been increased from 35% to 39%, and the total debt service (TDS) ratio has been increased from 42% to 44%. These changes affect the maximum mortgage amount that borrowers can qualify for.

What are the eligibility criteria and requirements for CMHC insurance?

To obtain CMHC insurance, the property must be located in Canada, the purchase price or property value must be up to $1 million, and the minimum down payment must be 5% of the first $500,000 and 10% of the remaining amount. The maximum amortization period for CMHC-insured residential mortgages is 25 years.

What is CMHC MLI Select for multi-unit properties?

CMHC MLI Select is a mortgage loan insurance product specifically designed for multi-unit properties with more than 5 rental units or a minimum of 50 units/beds for retirement homes. It offers a point scoring system where borrowers can receive incentives for meeting criteria related to affordability, energy efficiency, and accessibility.