As a professional mortgage underwriter in Canada, I often emphasize the importance of the Loan to Value (LTV) ratio in the mortgage qualification process. The LTV ratio is a critical factor in determining the terms of the mortgage for which a borrower qualifies, including the interest rate and the need for mortgage default insurance. Here’s an in-depth look at why LTV matters, how it influences the rates lenders charge, and the role of mortgage default insurance.

What is the Loan to Value (LTV) Ratio?

Examples of LTV Ratios: High Ratio Mortgage

Low-Ratio Mortgage Example without Default Insurance Calculation

Other Mortgage Products, Programs, and Refinancing

What is the Loan to Value (LTV) Ratio?

The Loan to Value ratio is a measure used by financial institutions to assess the risk associated with lending money for a mortgage. It is calculated by dividing the mortgage amount by the appraised value or purchase price of the property, whichever is less. The result is expressed as a percentage. A higher LTV ratio indicates more risk for the lender because it means the borrower is financing a larger portion of the property’s value.

Impact on Mortgage Rates

Lenders use the LTV ratio to determine the level of risk they are taking with a loan. Generally, loans with a higher LTV ratio are viewed as riskier, which can influence the interest rate offered to the borrower:

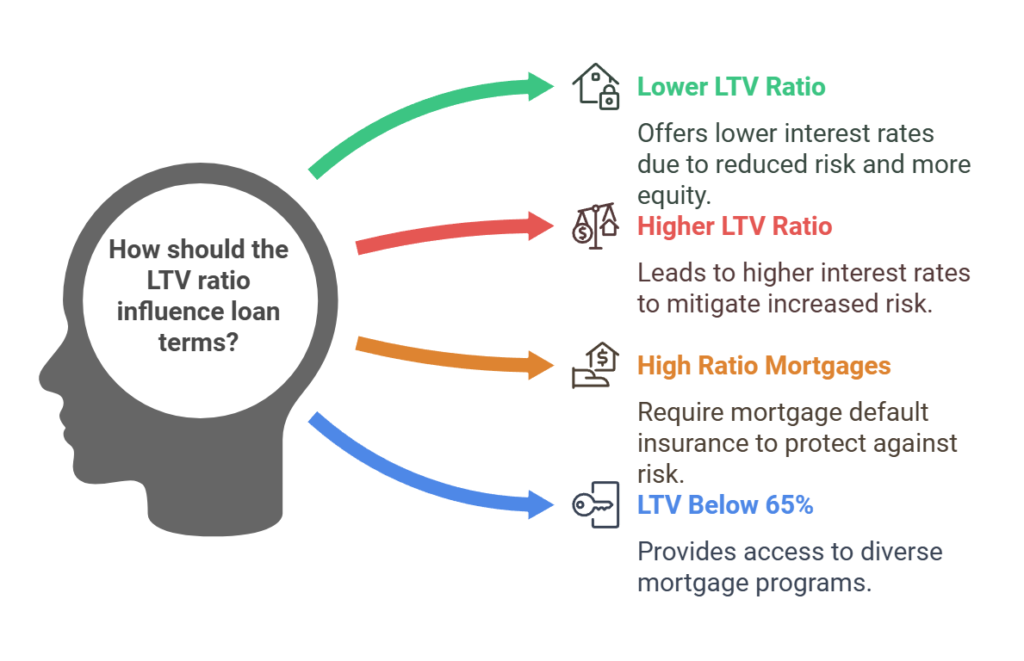

- Lower LTV Ratios: Loans with lower LTV ratios typically qualify for lower interest rates because they represent lower risk to the lender. Borrowers with low LTV ratios have more equity in their property, providing a buffer against fluctuations in property values.

- Higher LTV Ratios: Higher LTV ratios often result in higher interest rates. Lenders may charge these rates to mitigate the increased risk they incur when borrowers finance most of the property’s value.

- High Ratio Mortgages require mortgage default insurance

- LTV Ratios below 65% enable purchasers and mortgage holders to access a wider variety of mortgage programs including those that enable them to skip or suspend mortgage payments or take advantage of interest-only mortgages.

- Reverse Mortgage products usually go to an LTV ratio of 55%.

Mortgage Default Insurance

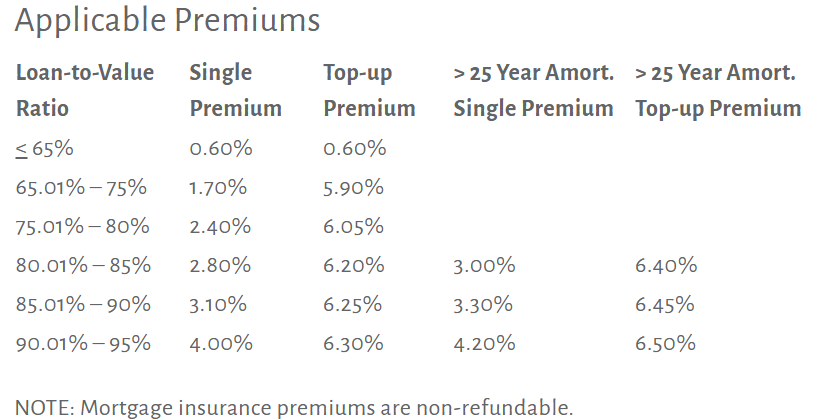

In Canada, mortgage default insurance is required for high-ratio mortgages — those with an LTV ratio greater than 80% (i.e., where the down payment is less than 20% of the purchase price). This insurance protects the lender in case the borrower defaults on the mortgage. The cost of this insurance is typically a percentage of the mortgage amount and depends on the LTV ratio of the loan.

- Cost and Calculation: Mortgage insurance premiums range from about 0.6% to 4.5% of the mortgage amount, depending on the size of the down payment. The premium can be paid in a lump sum at the time of purchase or added to the mortgage and included in monthly payments.

Examples of LTV Ratios: High Ratio Mortgage

High-Ratio Mortgage:

Scenario: A borrower purchases a home for $900,000 and makes a down payment of $90,000.

Calculation: The mortgage amount needed is $810,000.

LTV Ratio: $810,000 / $900,000 = 90%

Mortgage Default Insurance Required: Yes, since the LTV is greater than 80%.

Let’s further develop the high-ratio mortgage example for a home appraised at $900,000, where the borrower makes a down payment of $90,000, requiring a mortgage amount of $810,000. We’ll now include the calculation for the cost of mortgage default insurance.

High-Ratio Mortgage Example with Default Insurance Calculation

Home Appraisal Value: $900,000

Down Payment: $90,000

Mortgage Amount: $810,000

LTV Ratio: $810,000 / $900,000 = 90%

Mortgage Default Insurance Calculation

For high-ratio mortgages—those with an LTV ratio over 80%—mortgage default insurance is required. The premium rate depends on the exact LTV ratio. Given our scenario with a 90% LTV ratio, the premium typically might be around 4% of the mortgage amount, as this LTV is within one of the highest brackets commonly covered by mortgage insurers.

Insurance Cost Calculation:

Insurance Premium = Mortgage Amount × Premium Rate

Insurance Premium = $810,000 × 4% (LTV 90.01%) = $32,400

Note: This amount can be paid upfront or rolled into the mortgage.

Provincial Sales Tax (Ontario: 8%, Saskatchewan: 6%, Quebec: 9%): $32,400 x 8% = $2,592

Note: This amount must be paid upfront as part of the closing costs.

Total Cost of Mortgage Insurance Premium: $34,992

Total Cost and Monthly Impact

The total mortgage now includes the principal plus the insurance premium:

Total Mortgage After Adding Insurance Premium:

Total Mortgage = Mortgage Amount + Insurance Premium

Total Mortgage = $810,000 + $32,400 = $842,400

This adjusted total impacts the monthly mortgage payments by increasing them. To see the specific impact, one would need to calculate the monthly payments based on the mortgage term and interest rate.

Discussion

In this scenario, the addition of $34,992 in mortgage default insurance increases the total financing needed and will lead to higher monthly payments. The cost of the insurance premium is typically folded into the total mortgage amount, which the borrower pays off over the life of the mortgage, including interest, but the provincial sales tax portion must be paid up front as part of the closing costs. This addition emphasizes the importance of considering the total cost of purchasing a home, beyond just the list price and mortgage interest.

The existence of mortgage default insurance allows borrowers with less than a 20% down payment access to the housing market, albeit at a higher overall cost due to the insurance premiums. For many, this is a necessary trade-off to enter the housing market sooner.

Low-Ratio Mortgage Example without Default Insurance Calculation

Home Appraisal Value: $900,000

Down Payment: $350,000

Mortgage Amount: $550,000

LTV Ratio: $550,000 / $900,000 = 61%

Mortgage Default Insurance Required: No, as the LTV is less than 80%.

Discussion

In this scenario, no mortgage default insurance is required to be paid as the loan to value of the mortgage is under 80% (61%). By having a larger down payment and avoiding mortgage default insurance, this purchaser saved almost $35,000 compared to a person who had a much higher loan-to-value ratio. It often makes sense for purchasers to obtain additional down payment assistance if it is available to them to avoid paying mortgage default insurance. Such assistance could come from taking out a loan (flex down) if their debt service ratios will allow it, getting help from the bank of ‘Mom and Dad’, or sometimes seeking equity assistance from companies that will provide down payment assistance.

Lastly, in rising real estate markets, paying mortgage default insurance makes economic sense despite its seemingly high cost. As house prices rise, the price of homes can go up faster than people can save for a home. If a million-dollar house goes up in value by 6%, it goes up in value by $60,000, that’s more than people can save in a year. Paying mortgage default insurance allows buyers to get into the market earlier before it runs away from buyers.

Other Mortgage Products, Programs, and Refinancing

Depending on the mortgage holder’s loan to value ratio, certain mortgage products, programs and refinancing may or may not be available.

To be able to do any sort of mortgage refinancing, the loan-to-value ratio must be less than 80%. For example, you cannot do an equity take-out refinancing if the result is to have a mortgage loan that is greater than 80%.

Rental programs require a minimum 20% down payment (LTV of less than 80%). Other rental programs have a maximum loan to value of 70% LTV or less while others have a max LTV of 60% depending on the attributes of the deal and the mortgage. Contact me for more information as it pertain to your particular situation.

LTV Ratios below 65% enable purchasers and mortgage holders to access a wider variety of mortgage programs including those that enable them to skip or suspend mortgage payments or take advantage of interest only mortgages.

In Canada, the maximum loan-to-value (LTV) ratio for reverse mortgages is generally up to 55%. However, the specific amount a borrower can access through a reverse mortgage depends on several factors:

- Age of the Borrowers: The minimum age requirement for a reverse mortgage in Canada is typically 55 years old. The older the borrower, the higher the percentage of the home value they can borrow. This is because the loan does not require monthly payments and is not due until the home is sold, the borrowers move out, or the last borrower dies.

- Appraised Value of the Home: The amount of money a borrower can receive from a reverse mortgage is partially determined by the current market value of the home, as assessed by a professional appraiser.

- Location of the Home: Properties located in urban areas with higher real estate values might qualify for a higher loan amount compared to those in rural areas where home values might be lower.

- Condition of the Property: The state of the property also influences the loan amount. Well-maintained homes might receive a higher valuation, thereby increasing the available loan amount.

- Lender Policies: Different lenders might have slightly varying policies regarding the maximum LTV ratio, based on their risk assessment models.

Example of How LTV Varies by Age:

- A 55-year-old might be able to borrow up to 20-30% of their home’s value.

- An 85-year-old might be eligible to borrow up to 50-55% of their home’s value.

The reason for the age-based scaling is that reverse mortgages do not require repayment until the borrowers are no longer using the home as their primary residence. Therefore, the risk to the lender increases with the amount of time they might have to wait to recoup their loan, which is why they allow older homeowners to borrow a higher percentage.

Reverse mortgages can be a useful financial tool for older homeowners looking to supplement their income during retirement without the need to sell their home. However, because these loans can eventually consume a significant portion of the equity in a home, they are best considered carefully and typically as a last resort after other retirement funding options have been explored.

Conclusion

The Loan to Value ratio is a fundamental concept in Canadian mortgage lending that affects not only the eligibility and terms of the loan but also the necessity and cost of mortgage default insurance. By understanding and effectively managing their LTV ratios, borrowers can potentially secure more favourable mortgage terms and minimize their overall borrowing costs. For lenders, assessing the LTV ratio is crucial for risk management and pricing loans appropriately to reflect the level of risk involved.