The Open Banking Revolution: How Mortgages Are About to Get a Whole Lot Easier

If you’ve ever felt like getting a mortgage meant running an obstacle course—chasing down pay stubs, digging through old bank statements, sending documents back and forth—you’re not alone. The process can feel outdated, clunky, and stressful. But here’s the good news: change is on the horizon. It’s called Open Banking, and it’s going to flip the script on how we verify income, assets, and financial history.

Before I dive in, here’s a quick roadmap of what we’ll cover:

Who’s Building Open Banking in Canada

How It Will Transform Mortgage and Lending

Real-Life Examples: Before and After Open Banking

What This Means for Realtors and Clients

What Open Banking Is

At its core, Open Banking is a new way of securely sharing your financial data between banks, lenders, and trusted third-party providers. Getting your documents together to support a mortgage application today is brutal. Instead of emailing PDFs, scanning documents, or worrying about fraud, you’ll be able to grant a lender permission to directly access specific financial information—safely, quickly, and in real time.

Think of it like giving a house key to a trusted contractor, but instead of letting them wander through every room, you only unlock the one room they need to fix. You’re always in control, and the access is limited and secure.

Who’s Building Open Banking in Canada

In Canada, the federal government is steering this ship. They’ve brought together banks, fintech companies, regulators, and consumer advocates to design a secure, standardized framework. While Open Banking has already gained traction in places like the UK and Australia, Canada has been taking its time to make sure privacy, security, and consumer choice are baked into the system.

The first phase, known as Consumer-Directed Finance, is already underway. The goal is to create a trusted system where Canadians can share their financial data easily—without giving out logins and passwords like we sometimes do today with third-party apps.

How It Works in Practice

Here’s what happens when Open Banking is fully implemented:

- You apply for a mortgage.

- Instead of uploading your NOAs, bank statements, and pay stubs, you simply give consent for your lender to access the necessary data directly from your bank.

- The lender gets instant confirmation of your income deposits, account balances, and even recurring expenses—all without you lifting a finger.

It’s safe, it’s encrypted, and you stay in control. You can revoke access at any time, and only the exact data you approve gets shared.

How It Will Transform Mortgage and Lending

Right now, underwriting a mortgage can take days or even weeks. Documents need to be collected, reviewed, and verified manually. If you’re self-employed or have multiple income streams, the process is even more complicated.

With Open Banking, here’s how things will change:

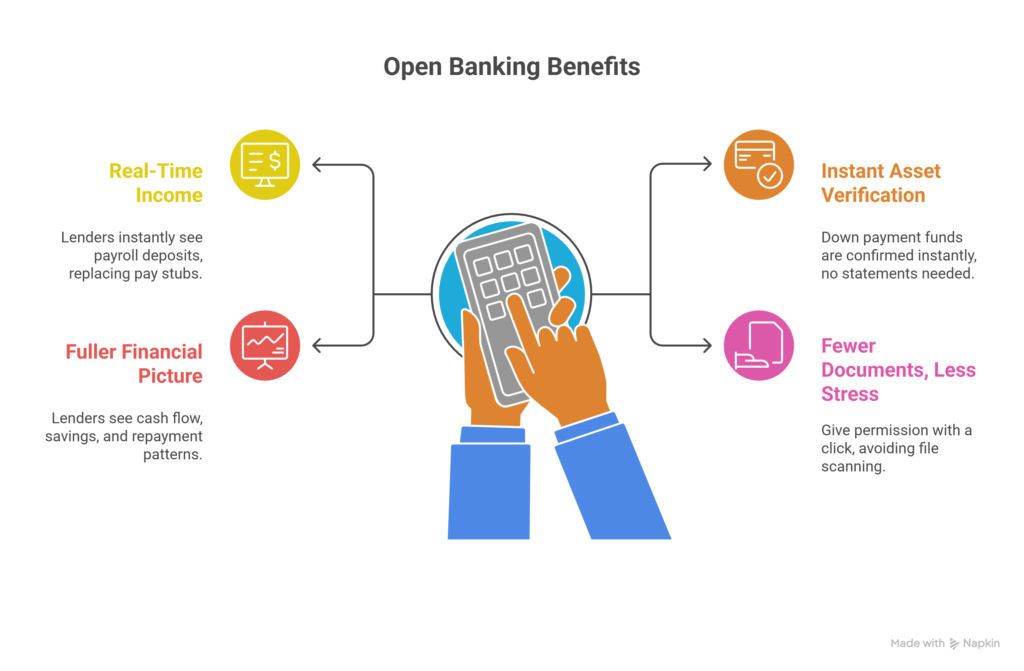

- Real-Time Income Verification: Instead of submitting months of pay stubs, lenders see your payroll deposits instantly.

- Instant Asset Verification: Forget digging up six months of bank statements. Your down payment funds can be confirmed on the spot.

- A Fuller Financial Picture: Lenders won’t just rely on your credit report. They’ll also see your real cash flow, savings habits, and repayment patterns—making approvals faster and often fairer.

- Fewer Documents, Less Stress: Instead of scanning and emailing dozens of files, you’ll just give permission with a click.

Real-Life Examples: Before and After Open Banking

Let’s put this into a story.

Meet Sarah, a self-employed graphic designer.

Today, Sarah wants to buy her first condo. She spends hours pulling together tax returns, NOAs, invoices, and bank statements. Her lender has to piece everything together to prove her income, and the process drags out for weeks. It’s frustrating, and she worries she might lose the condo to another buyer while waiting.

Now, fast forward to the world of Open Banking.

Sarah applies for a mortgage and simply checks a box to share her banking data. Her lender sees her regular client deposits over the last 12 months, her consistent savings contributions, and her healthy balance. Within hours, her income and assets are verified—no stacks of paperwork, no stress, and no delays. Sarah gets her approval before the weekend, and she moves forward with confidence.

What This Means for Realtors and Clients

If you’re a realtor, Open Banking means your clients can move faster. Quick mortgage approvals translate into stronger offers in competitive markets. No more waiting for paperwork to catch up while a hot listing slips away.

If you’re a client, it means less stress, fewer late-night hunts for bank statements, and the comfort of knowing your financial information is verified instantly and securely. You’ll spend less time on paperwork and more time focusing on finding the home you love.

Allen’s Final Thoughts

Open Banking is more than just a buzzword—it’s the future of mortgages in Canada. By simplifying verification, reducing paperwork, and speeding up approvals, it’s going to make the homebuying journey smoother for everyone involved.

As your mortgage agent, I’m here to guide you through this transition. Whether you’re a realtor helping clients write winning offers, or a family preparing for your first home, I’ll help you take advantage of these new tools as they roll out. My role is to connect you with lenders who are embracing this technology and to make sure you’re always one step ahead.

At the end of the day, my job is to cut through the noise, save you time, and help you get into the right home with the right mortgage. And with Open Banking on the horizon, that job just got a whole lot easier.