Divorce is rarely clean, but when it comes to the house, things get extra complicated.

I get this call a lot:

“Hey Allen, I’m keeping the house, and I’m buying my ex out… What happens to the mortgage? Can I even afford it? Are there penalties?”

Let’s break it down step by step—with plain language, real talk, and expert insight—so you know what to expect if you’re the one staying put and buying your former partner out.

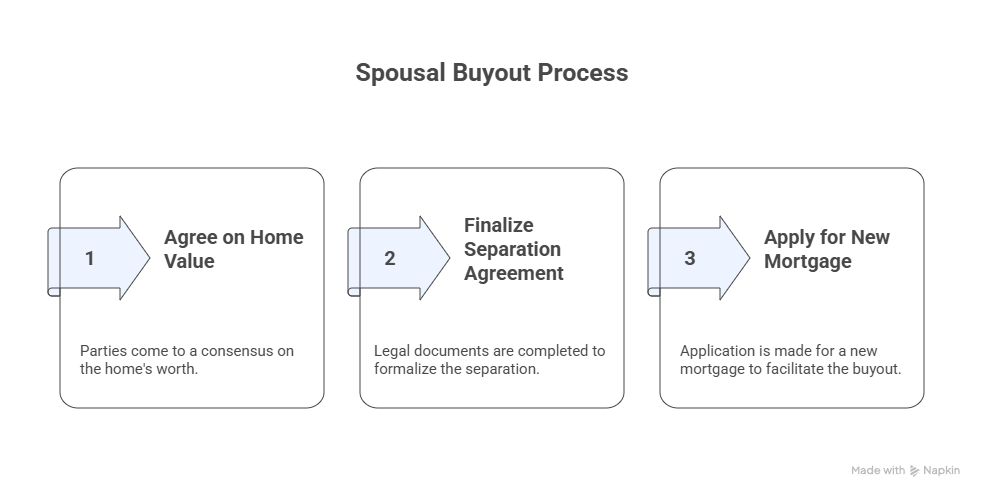

Step One: Agree on the Home’s Value

Step Two: Finalize the Separation Agreement

Step Three: Apply for the New Mortgage (a.k.a. The Buyout)

3 Common Ways to Buy Out Your Ex

What if You Can’t Qualify to Keep the Home?

Step One: Agree on the Home’s Value

Before anything else, both parties need to agree on what the property is worth today. That means getting a professional appraisal—no guessing based on your neighbour’s listing price or what your cousin said it was worth.

A proper appraisal protects both sides. It gives you the hard number you’ll base the buyout on. And if you’re using a lender’s Spousal Buyout Program, that appraisal is mandatory.

Step Two: Finalize the Separation Agreement

Lenders won’t move forward without a legally binding Separation Agreement.

This document needs to clearly state:

- Who’s keeping the home

- What the buyout amount is

- How any other joint debts or assets are being handled

No agreement = no mortgage. Period.

Step Three: Apply for the New Mortgage (a.k.a. The Buyout)

This is where I come in.

To keep the house and buy your ex out, you’ll need to refinance the mortgage in your name only. That means passing the usual lending requirements:

- Sufficient income

- Good credit

- Acceptable debt ratios

- Stability in employment

BUT! There’s good news: if you’re using the Spousal Buyout Program, you may be able to refinance up to 95% of the home’s value, even if you wouldn’t normally qualify for that high a loan-to-value ratio in a standard refinance.

That extra wiggle room helps cover:

- The existing mortgage payout

- The lump-sum equity owed to your ex

- Possibly even legal fees (depending on the lender)

Pro tip: Not every lender offers the Spousal Buyout Program and not every Spousal Buyout Program is the same; contact me for details… I’m here to help!

What About Penalties?

If your existing mortgage is being broken early (say, before the term is up), you’ll likely face a prepayment penalty. How much?

It depends on:

- Whether you’re in a fixed or variable mortgage

- How much time is left in the term

- What your lender’s specific formula is

For fixed-rate mortgages, the penalty is usually the greater of 3 months’ interest or something called the Interest Rate Differential (IRD)—which can be thousands.

Mortgage assumption: If the spouse staying in the home qualifies on their own, some lenders may allow them to assume the mortgage without triggering a penalty. This is rare and must be explicitly allowed in the mortgage terms.

If you’re going through a divorce, it’s worth calling the lender before committing to a buyout to get an accurate penalty quote. I help clients do this all the time, and sometimes we can fold the penalty into the new mortgage to avoid paying it out of pocket.

3 Common Ways to Buy Out Your Ex

Let’s walk through your main options for buying out your spouse or partner:

- Traditional Refinance (Up to 80% Loan-to-Value)

- Spousal Buyout Program (Up to 95% Loan-to-Value)

- Co-Signer or Guarantor Refinance

Traditional Refinance (Up to 80% Loan-to-Value)

This works if:

- You have enough equity in the home

- The buyout amount is modest

- You’re not using the extra funds for anything beyond mortgage payout + equity transfer

Straightforward and relatively easy—but limited to borrowing up to 80% of the home’s current value. If that’s not enough, you’ll need option #2.

Spousal Buyout Program (Up to 95% Loan-to-Value)

Designed specifically for divorce or separation scenarios.

Conditions:

- You must have a finalized separation agreement

- Appraisal is required

- Funds must go directly toward the buyout—not personal spending

The benefit? You can access more equity without needing a second mortgage or private loan. This program is a lifesaver for people with equity in the home but not a ton of cash in the bank.

Co-Signer or Guarantor Refinance

If your income alone isn’t strong enough to carry the mortgage, you may consider bringing in a co-signer—like a parent, sibling, or trusted friend—to strengthen your application.

This doesn’t change ownership (unless you want it to), but it does help satisfy lenders on the income side.

Be warned: your co-signer is on the hook if payments are missed. So this option requires a high level of trust—and clear communication.

What if You Can’t Qualify to Keep the Home?

Hard truth: sometimes, the numbers just don’t work.

You can’t refinance, and you can’t get a co-signer. In that case, the best option is usually to sell the property, pay off the mortgage, split the proceeds, and start fresh.

It’s not ideal, but it may be the cleanest financial path forward. Remember: owning a home you can’t afford is worse than walking away with a clean slate.

My Final Word: Get Advice Before You Sign Anything

In divorce, emotions often move faster than logic. But when it comes to the mortgage—slow it down, get proper advice, and run the numbers before making big decisions.

As a mortgage agent, I’m here to:

- Help you qualify for a buyout

- Connect you with appraisers and lawyers

- Strategize around penalties and timing

- Make sure you’re not overcommitting out of guilt or fear

This isn’t just about keeping a roof over your head. It’s about keeping your future intact.

Let’s Talk First—Before You Make it Legal

Buying your ex out is a major financial move. Let’s make sure you do it right. I’m here to help you plan the process, avoid costly mistakes, and land on your feet.

Call or email me for a confidential conversation.