… Where the Lease Meets the Loan

When it comes to commercial real estate, most people think of two separate worlds — the lease and the loan. One defines how a business occupies a property; the other defines how the property is financed. But here’s the truth that many overlook: these two worlds are deeply intertwined.

Whether you’re a landlord looking to maximize financing potential, a business owner negotiating lease terms, or a realtor structuring a deal, understanding how commercial leases and commercial mortgages interact can make or break your investment strategy.

Allow me to unpack how the lease you sign (or draft) can directly affect your mortgage approval, property valuation, and long-term profitability.

Topics I’ll Cover

The Relationship Between Leases and Commercial Mortgages

Why Lease Structure Affects Financing

Key Lease Terms Lenders Scrutinize

How Tenants Influence Property Value and Mortgage Terms

Common Pitfalls and How to Avoid Them

The Relationship Between Leases and Commercial Mortgages

A commercial mortgage is a loan secured by income-producing real estate — think retail plazas, industrial warehouses, or office buildings. The lender’s confidence in that property’s value and cash flow is largely built on the leases in place.

In essence, the lease is the heartbeat of a commercial property’s financial health. It dictates how much income the property generates, how stable that income is, and how likely it is to continue over time.

A lender doesn’t just look at the borrower — they look at the tenants. A strong tenant with a long, stable lease can boost financing opportunities. Conversely, short-term or unstable tenants can weaken a property’s lending profile.

Why Lease Structure Affects Financing

From a lender’s perspective, the quality of the lease determines the predictability of income. Predictable income equals lower risk — and lower risk can mean better loan terms.

Let’s look at how different lease types impact financing:

Gross Lease:

Since the landlord pays operating expenses, the property’s net income can fluctuate. Lenders might view this as slightly higher risk unless there’s a clear history of stable expense management.

Triple Net (NNN) Lease:

Tenants cover taxes, insurance, and maintenance, leaving the landlord with more predictable net income. Lenders love this structure because it stabilizes cash flow and reduces operating risk.

Modified Gross Lease:

This middle-ground structure can work well, but lenders will want clarity on which expenses belong to the tenant versus the landlord to calculate true net operating income.

In short, leases that transfer more expenses to tenants generally strengthen financing potential because they reduce variability in the landlord’s bottom line.

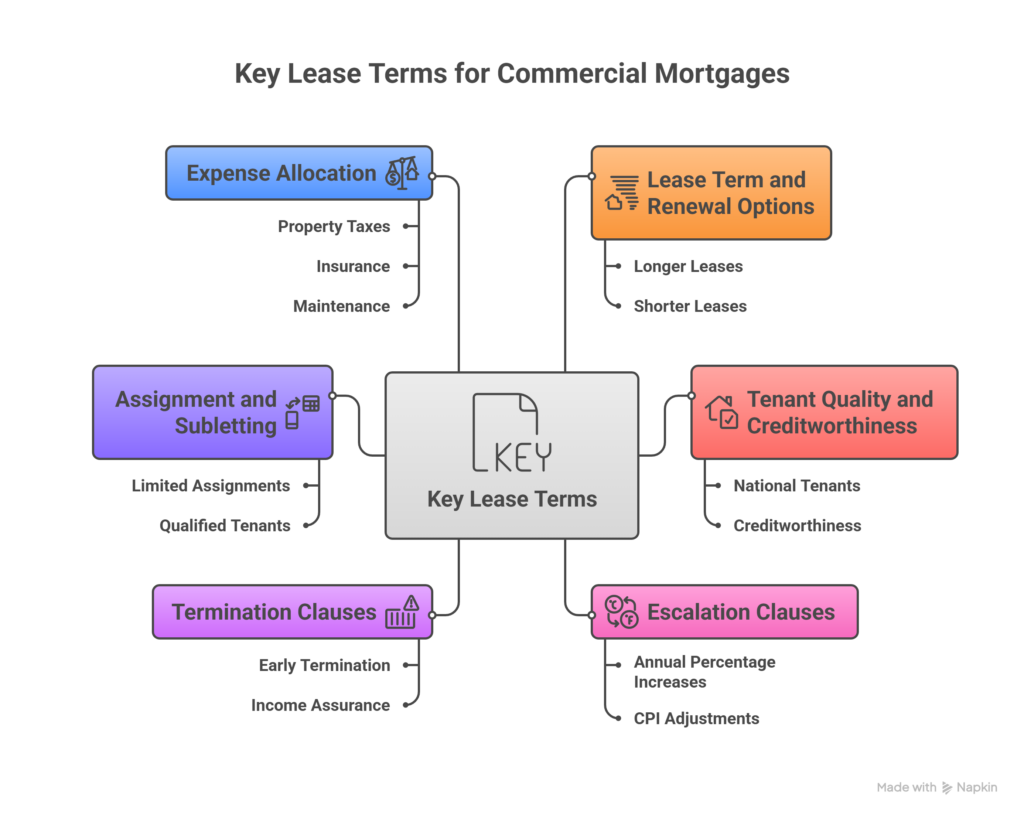

Key Lease Terms Lenders Scrutinize

When reviewing a commercial mortgage application, lenders don’t just glance at the rent roll — they dive deep into the lease agreements. Here are the clauses that raise or lower eyebrows:

1. Lease Term and Renewal Options:

Longer lease terms with reliable tenants create stability. A five- or ten-year lease term signals predictable income. Shorter terms might lead to tighter lending conditions or higher rates.

2. Tenant Quality and Creditworthiness:

National or established tenants (like Shoppers Drug Mart or TD Bank) can significantly improve loan terms. Lenders often consider tenant credit as a proxy for income reliability.

3. Escalation Clauses:

Rent increases built into the lease — such as annual percentage increases or CPI adjustments — help preserve cash flow against inflation, a major plus for lenders.

4. Termination Clauses:

Leases that allow tenants to terminate early introduce risk. Lenders want assurance that income is locked in.

5. Assignment and Subletting:

Lenders prefer leases that limit risky assignments or sublets, as they can introduce less-qualified tenants.

6. Expense Allocation:

Clear definitions of who pays for property taxes, insurance, and maintenance ensure lenders can accurately model net income.

A well-drafted lease can turn a good deal into a great one by showcasing income stability and minimizing ambiguity.

How Tenants Influence Property Value and Mortgage Terms

In commercial real estate, the tenant mix directly influences a property’s value and mortgage eligibility. Lenders view the income stream as the primary collateral, so the reliability of those tenants matters as much as — sometimes more than — the borrower’s financial strength.

Example:

Imagine two similar retail plazas.

- Plaza A is fully leased to national brands like Starbucks, Scotiabank, and Subway, all under long-term triple net leases.

- Plaza B has a mix of short-term local businesses under month-to-month agreements.

Even if both properties earn similar gross rent, Plaza A will appraise higher and secure more favourable mortgage terms because its income is stable, diversified, and low-risk.

For landlords, this means choosing quality tenants and structuring strong leases can directly boost financing power.

For tenants, it’s equally important — a well-structured lease can improve their ability to negotiate leasehold improvement loans or financing tied to their business operations.

Common Pitfalls and How to Avoid Them

Many investors and landlords underestimate how lease details can derail financing. Here are a few traps to avoid:

Vague Lease Terms:

Ambiguous clauses around expenses or renewals can make lenders nervous. Always ensure clarity in responsibilities and timelines.

Overly Short Lease Terms:

If major tenants have less than three years left, refinancing becomes more challenging. Lenders prefer longer commitments.

Unrealistic Market Rent:

If leases are significantly above or below market value, lenders may adjust the property’s income to reflect true market conditions, affecting loan size.

Non-Transferable Leases:

Clauses that restrict assignment or create uncertainty during property sale can reduce a property’s marketability — and thus its financing options.

Ignoring Estoppel Certificates:

Before finalizing financing, lenders often require tenants to sign estoppel certificates confirming lease details. Missing or inaccurate certificates can delay closing.

Allen’s Final Thoughts

The intersection of commercial leases and commercial mortgages is where strategy meets execution. The lease creates the cash flow; the mortgage transforms that cash flow into leverage and long-term equity growth.

If you’re a landlord, your leases are your financial backbone. Structure them not just for occupancy, but for financing strength — long terms, stable tenants, and clearly defined expense responsibilities can all enhance property value and borrowing power.

If you’re a tenant, understand how your lease terms affect financing potential — both for your landlord and for your own business. The stronger your lease, the more likely you’ll attract favourable financing for leasehold improvements or expansion.

And if you’re a realtor, knowing how lease structures influence lending can set you apart. You’ll guide clients toward properties with stronger financial fundamentals — and deals that close faster and cleaner.

As a mortgage agent, I work right at this intersection. I help property owners, investors, and business tenants align their lease terms with lending requirements to ensure financing is smooth, strategic, and stress-free. Whether you’re negotiating a lease, refinancing a plaza, or evaluating a commercial purchase, I can help you understand how the fine print on paper translates into real-world lending power.

Because in commercial real estate, the best deals aren’t just about location or price — they’re about how well the lease and the loan work together.