When most people think about the cost of a mortgage, their mind goes straight to the interest rate. That’s natural—but it’s incomplete. There’s another category of costs that often shows up only at the very end of a transaction, when timelines are tight and decisions are already made: mortgage discharge costs.

That’s exactly why I coded up my Mortgage Discharge Cost Calculator.

This tool is designed to help you see—clearly and early—what it actually costs to remove a mortgage from title, based on the type of lender you’re dealing with. Whether you’re refinancing, switching lenders, selling a property, or restructuring debt, knowing these numbers in advance puts you back in control.

Below, I’ll walk you through how to use the calculator properly, and more importantly, how to apply the results in real-world decisions.

What the Mortgage Discharge Cost Calculator Does

The calculator estimates the administrative and legal costs involved in discharging a mortgage in Canada. These are not mortgage penalties (like IRD or three months’ interest). Instead, they’re the often-overlooked fees charged by:

- Your lender

- Your lawyer

- Land registry systems

- Administrative and trust processes

The calculator adjusts automatically based on whether your mortgage is with a:

- Prime lender (bank or monoline)

- Alternative lender (Alt-A / B)

- Private or MIC lender

Each lender category comes with very different discharge realities, and the calculator reflects that.

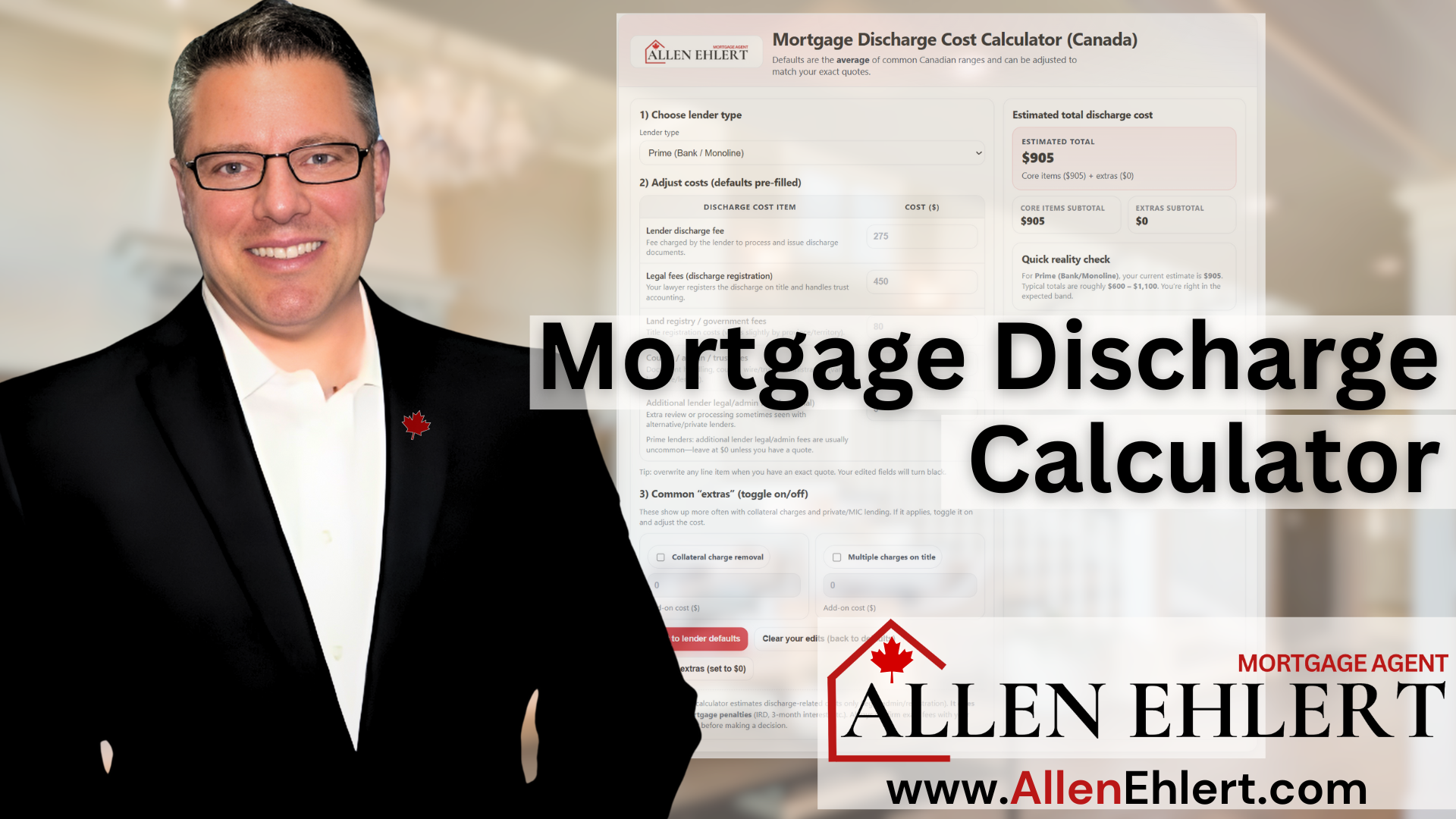

Step 1: Choose Your Lender Type

At the top of the calculator, you’ll select your lender type.

This step matters more than most people realize.

A prime lender discharge is usually straightforward. A private or MIC discharge often isn’t. By choosing the correct lender category, the calculator loads realistic default values based on typical Canadian experience.

Those defaults are averages, not worst-case scenarios—and they’re meant to give you a reasonable starting point, not a scare tactic.

Step 2: Review the Default Cost Items

Once the lender type is selected, you’ll see a breakdown of common discharge cost categories, such as:

- Lender discharge fee

- Legal fees to register the discharge

- Land registry / government fees

- Courier, admin, and trust fees

- Additional lender legal or administrative fees

All default values appear in light grey. That’s intentional.

Light grey tells you:

“This is a typical estimate, not a quote.”

At this stage, you’re getting a planning number, which is exactly what you want early in a decision-making process.

Step 3: Overwrite Any Line Item With Real Quotes

As soon as you type your own number into any field, it turns black.

That visual cue is critical. It tells you:

- What’s still an estimate

- What’s now a confirmed or assumed cost

If your lawyer tells you their discharge fee will be $550, type it in.

If your lender confirms a $395 discharge fee, overwrite the default.

This allows the calculator to evolve from a planning tool into a decision tool.

Step 4: Toggle Common “Extras” (When They Apply)

Some discharge costs only appear in certain situations, especially with alternative and private lending.

The calculator lets you toggle items like:

- Collateral charge removal

- Multiple charges on title

If the toggle is off, the cost is excluded entirely.

If it’s on, a default estimate appears (again in grey), which you can override.

This is particularly useful for:

- Collateral mortgages

- Private loans with layered registrations

- Complex refinances or exits

Step 5: Review the Total and Subtotals

On the right-hand side, the calculator shows:

- Total estimated discharge cost

- Core items subtotal

- Extras subtotal

This breakdown helps you quickly see:

- How much is “unavoidable”

- How much is driven by structure and lender choice

It also helps professionals explain costs clearly to clients without hand-waving or vague language.

Step 6: Use the Reality Check (This Is Where Insight Lives)

At the bottom, you’ll see a Quick Reality Check.

This compares your current estimate against typical Canadian ranges for that lender type. It doesn’t judge—it simply answers the question:

“Is this number broadly consistent with what usually happens?”

If you’re inside the range, you’re likely planning realistically.

If you’re outside it, that’s not wrong—but it’s a signal to pause and ask why.

Sometimes that “why” uncovers:

- A structure that’s no longer serving you

- Fees that weren’t disclosed clearly upfront

- Or a refinance that isn’t as beneficial as it first appeared

When You Should Use Allen Ehlert’s Mortgage Discharge Cost Calculator

This tool is most valuable before you commit to anything.

Use it when you’re:

- Comparing a refinance vs. staying put

- Considering a lender switch at renewal

- Selling a property with a non-standard mortgage

- Working through a separation or estate situation

- Evaluating private or short-term financing exits

- Paying off your mortgage

It’s especially powerful for realtors, financial planners, and borrowers who want to avoid last-minute surprises.

Allen’s Final Thoughts

Mortgage discharge costs are rarely the headline—but they’re often the footnote that changes the math.

This calculator isn’t about fear or complexity. It’s about clarity. When you understand the full cost of getting out of a mortgage, you make better decisions about getting into one—or changing it.

Use the calculator early. Use it honestly. And if the numbers raise questions, that’s not a problem—that’s an opportunity to structure things better before the clock starts ticking.