… The Disappearing Dollar: Why Your Paycheque Buys Less of What Really Matters

Let’s talk about something that’s been quietly eating away at Canadians’ financial future — purchasing power. Sure, your income might rise over time, and the news might say inflation’s “under control.” But if you’ve ever wondered why your parents could buy a house on one income while you’re grinding just to save a down payment, the answer isn’t as simple as the Consumer Price Index (CPI).

CPI tells us how much more it costs to buy bread, gas, and Netflix subscriptions — but it doesn’t tell us how much more it costs to buy assets: homes, land, businesses, or investments that create real wealth. That’s where the true story of money’s decline hides.

Topics Covered

The Real Story: Asset Inflation vs. Income Growth

How Realtors and Clients Can Use This Knowledge

The Mirage of CPI

You hear it all the time — “Inflation is 2% this year.” Sounds manageable, right? But CPI measures consumer goods, not capital goods. It’s like checking your temperature when what you really need is a full-body scan.

Think of CPI as the “shopping cart index.” It tracks the cost of groceries, fuel, and clothes. But if you’re trying to build wealth, those aren’t the things you’re investing in. You’re trying to buy assets — homes, rental properties, or stocks — and that’s where prices have sprinted ahead of wages.

So, while the cost of milk might rise by 3%, the cost of a detached home might climb by 15%. The CPI says inflation is stable, but your down payment goal keeps running away from you.

The Real Story: Asset Inflation vs. Income Growth

Here’s where the rubber meets the road. Over the past few decades, wage growth in Canada has limped along at about 2–3% annually. Meanwhile, real estate in many markets — Toronto, Vancouver, even smaller Ontario towns — has doubled or tripled in price.

That’s not inflation you can measure in a grocery aisle. That’s a full-blown asset inflation.

What’s happened is that central banks, low interest rates, and easy credit have made borrowing cheaper. That sounds great until you realize it also pushes asset prices higher, faster than most people’s pay can keep up. So while you’re earning a bit more each year, the very assets that could secure your financial future are slipping further away.

The Details in the Data

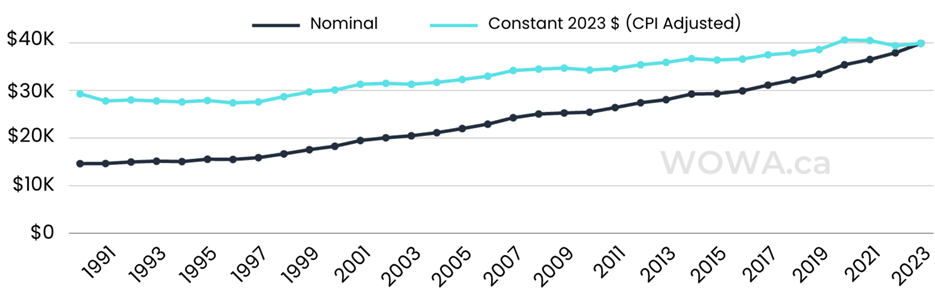

The following shows that after taxes, in 2023 the median Canadian income was about $40,000.

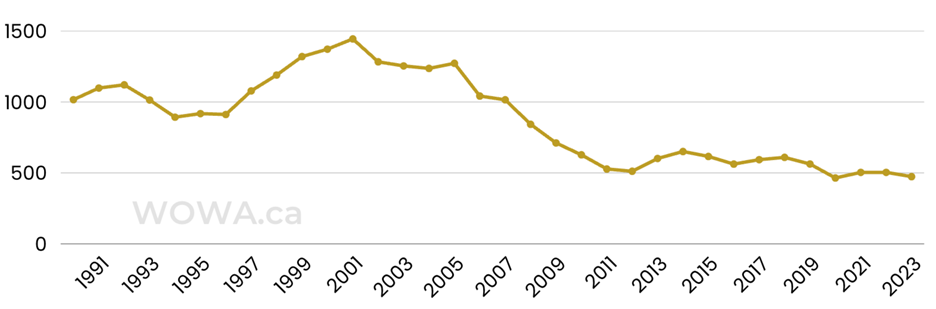

However, when Canadians’ income is compared to grams of gold (imagine you are paid in grams of gold instead of Canadian dollars), the median annual income after taxes is dropping:

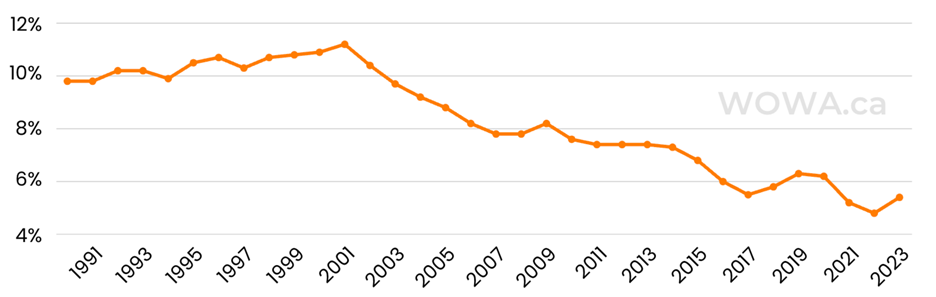

But people don’t live in bars of gold; they live in homes. The following chart shows how Canadians’ median after-tax income as a percentage of the median home continues to fall:

Historically, the median home price in Canada has been 2.4 to 3 times the median income. That means, given that the median Canadian income is around $70,000, the median home in Canada should go for around $210,000. Presently, it’s about $700,000 nationally. However, in the GTA, it is about $1,060,000. For the greater Vancouver area, it’s $1,150,000, but when you are just talking detached homes, the benchmark is about $1,950,000.

Unless someone gives you a pile of money, good luck!

A Tale of Two Generations

Let’s put this into a story.

Meet Tom and Lily — two generations apart, both starting out in Ontario.

In 1985, Tom bought his first home in Whitby for $90,000. His household income was around $40,000 a year. His mortgage payment took up less than 25% of his take-home pay. He even managed a few trips to Florida without breaking the bank.

Fast-forward to 2025. Lily, Tom’s granddaughter, is earning $80,000 as a young professional — double what her granddad made. But the average home in the same neighbourhood is now $950,000, boringly average for Whitby. Even with her solid job, Lily would need nearly $200,000 just for a 20% down payment.

She can afford Uber Eats, vacations, and streaming subscriptions — the consumer goods CPI measures — but she can’t buy into the asset class that builds lasting wealth. Her parents can’t understand why she is wasting money on ‘luxuries’ and not buying a home. They don’t understand that for Lily, luxuries are relatively cheap, but staples, like food, a vehicle, or a home, are beyond what many Canadians can afford.

It’s a different world.

That’s the real depreciation of money — not what happens in your grocery cart, but what happens in your wealth-building capacity.

How Realtors and Clients Can Use This Knowledge

This isn’t just an academic debate. It’s a call to action.

For realtors, understanding this dynamic helps you position real estate as more than just a purchase — it’s a hedge against long-term currency erosion. Instead of saying, “You’re buying a home,” you can say, “You’re locking in your future purchasing power.” That’s a message that resonates, especially with younger buyers who feel the game is rigged.

For clients, this means thinking differently about timing and leverage. Waiting for prices to drop often means losing more purchasing power as inflation compounds and rates fluctuate. Even small steps — like buying a condo before a detached, or using equity from family support — can help you enter the asset market sooner.

In other words, the sooner you own an appreciating asset, the sooner you step off the treadmill of inflation and start benefiting from it.

Allen’s Final Thoughts

Here’s the uncomfortable truth: your money’s value isn’t just about what it buys today — it’s about what it can buy tomorrow. And if tomorrow’s assets are sprinting ahead while your income jogs behind, then you’re losing ground every year.

As a mortgage agent, my role isn’t just to get you a mortgage. It’s to help you understand the bigger financial picture — how leverage, timing, and strategy can protect your future purchasing power.

Whether you’re a first-time buyer, a realtor guiding your clients, or an investor planning your next move, I’m here to help you turn financial theory into financial freedom. Together, we can make sure your money works as hard for you as you do for it.

Because at the end of the day, owning assets isn’t just about having a roof over your head — it’s about reclaiming your power in a system where cash loses and ownership wins.