… Allen Ehlert’s Secret Weapon for Stress-Free and Reduced Risk Moves

If you’ve ever bought and sold homes at the same time, you know it can feel like trying to juggle with oven mitts on. Point-to-point moves are fraught with danger, and they never come off without a hitch. So you get smart and decide you need bridge financing. Or maybe you’ve got your sale closing a week (or sometimes even a month) after your purchase, and the question hits: How the heck am I going to cover owning two properties at once if I even can?

This is exactly where Allen Ehlert’s Ultimate Canadian Bridge Financing Calculator steps in. Think of it as your flashlight in a dark basement—it takes the guesswork out of carrying two homes at the same time and lays out the numbers in plain English.

Before I dive into how to use it, here’s what I’ll be sharing:

Understanding Bridge Financing

How to Use the Bridge Financing Calculator

Real-World Examples for Realtors and Clients

A Story That Brings It All Home

Understanding Bridge Financing

Bridge financing is a short-term loan that lets you “bridge” the gap between buying your new home and receiving the sale proceeds from your old one. In practice, this means you can close on your dream home without waiting around nervously for your buyer’s funds to land in your account.

But here’s the rub: carrying two homes isn’t free. You’ll pay interest on the bridge loan (usually calculated daily), and you’ll want to know exactly what that cost looks like before you dive in. That’s where the calculator shines.

You also need to know that not all lenders provide bridge financing, so if you think you’ll need it (and yeah, you need it… I would never sell one home and move to another without it), it’s important to arrange bridge financing at the same time I’m negotiating your new mortgage so that I may even be able to get you a bit of a deal.

Lastly, if you are paying cash for your new home, you can’t get bridge financing. Bridge financing is a bit of a perk I can negotiate with some lenders to protect your purchase/sale and support a smooth move.

How to Use the Bridge Financing Calculator

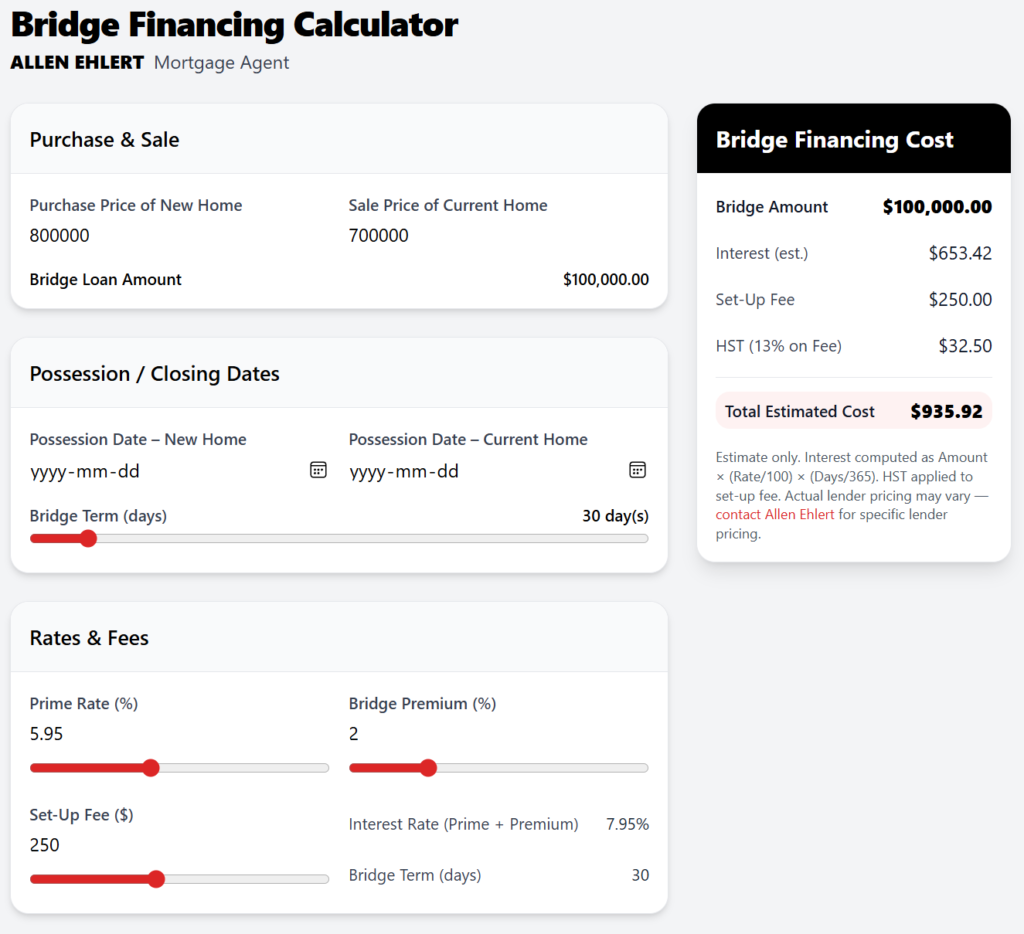

Using the calculator is straightforward—no math degree required. Here’s how you do it:

- Enter the purchase price of your new home.

- Input the sale price of your current home.

- Add in your existing mortgage balance.

- Choose the interest rate (typically your lender will tell you).

- Select the number of days you’ll need bridge financing.

Hit calculate, and—boom—the numbers appear. You’ll see the cost of carrying both homes at once, laid out clearly, so you can plan ahead instead of sweating in silence.

Real-World Examples for Realtors and Clients

For my clients, this tool is a sanity-saver. Imagine you’re upgrading from a condo to a detached home. Your new place closes on June 1st, but your buyer can’t close on your condo until June 15th. That’s a two-week gap. With the calculator, you can punch in your numbers and instantly know approximately what that 14-day bridge loan will cost you. No surprises.

For realtors, it’s a relationship-builder. Instead of leaving your clients in the dark, you can walk them through the calculator and show them the real cost of carrying two homes. That transparency builds trust—and trust turns into referrals.

A Story That Brings It All Home

Let’s picture Sarah and Mike. They found their dream home in Windsor—big backyard, space for the kids, the whole deal. The problem? Their new house closes in three weeks, but their townhouse sale doesn’t close until five weeks from now. That’s a two-week overlap.

Sarah was panicked, thinking they’d have to somehow come up with the full purchase price upfront. But once they used Allen’s calculator, they saw it wasn’t nearly as scary as they thought. The cost of carrying both homes for 14 days was manageable, and it gave them the confidence to move forward without second-guessing.

And guess what, when they pulled up to their new home with a moving van full of their life’s possessions, they discovered the sellers were not yet out of the house. Despite the home being officially theirs at 6 pm, the sellers’ movers hadn’t shown up. Fortunately, because Sarah and Mike still had possession of their townhouse because they had bridge financing, they were able to work out a solution with the sellers that took the stress off and put a little bit of money in their pocket. They used that money to get the carpets cleaned and give their new home a fresh paint job. They even replaced the toilets!

Bridge financing took what could potentially have turned into a disaster that broke the deal into a smooth and less stressful experience.

Allen’s Final Thoughts

Buying and selling at the same time doesn’t have to feel like a circus act. With the Ultimate Canadian Bridge Financing Calculator, you can see the exact cost of carrying two homes before you even sign on the dotted line. Whether you’re a homebuyer or a realtor, this tool empowers you to plan, budget, and breathe easy.

At the end of the day, calculators don’t just crunch numbers—they give you peace of mind. And that’s priceless.

How I Can Support You

As your mortgage agent, I’m not just here to hand you a calculator link and wish you luck. I’m here to walk you through every step—whether that’s running bridge financing scenarios, negotiating the best rates with lenders, or explaining how this fits into your bigger financial picture.

I can:

- Break down your bridge financing options in plain language.

- Coordinate with your realtor so everyone’s on the same page.

- Help you structure the timing of your purchase and sale to minimize costs.

- Make sure you’re not just covered, but confident.

So, next time you’re worried about carrying two homes, don’t sweat it—reach out. Together, we’ll make sure the numbers work in your favour and your move feels like an upgrade, not an ordeal.