…The Mortgage Matchmaker: Finding the Right Fit for Your Payments and Your Future

Let’s face it—mortgages aren’t exactly cocktail-party conversation. But if you’re like most homeowners, you’ve probably asked yourself more than once: “Am I really getting the best deal on my mortgage?” That’s the kind of question that can keep you up at night—or at least make you wince every time a payment comes out of your account.

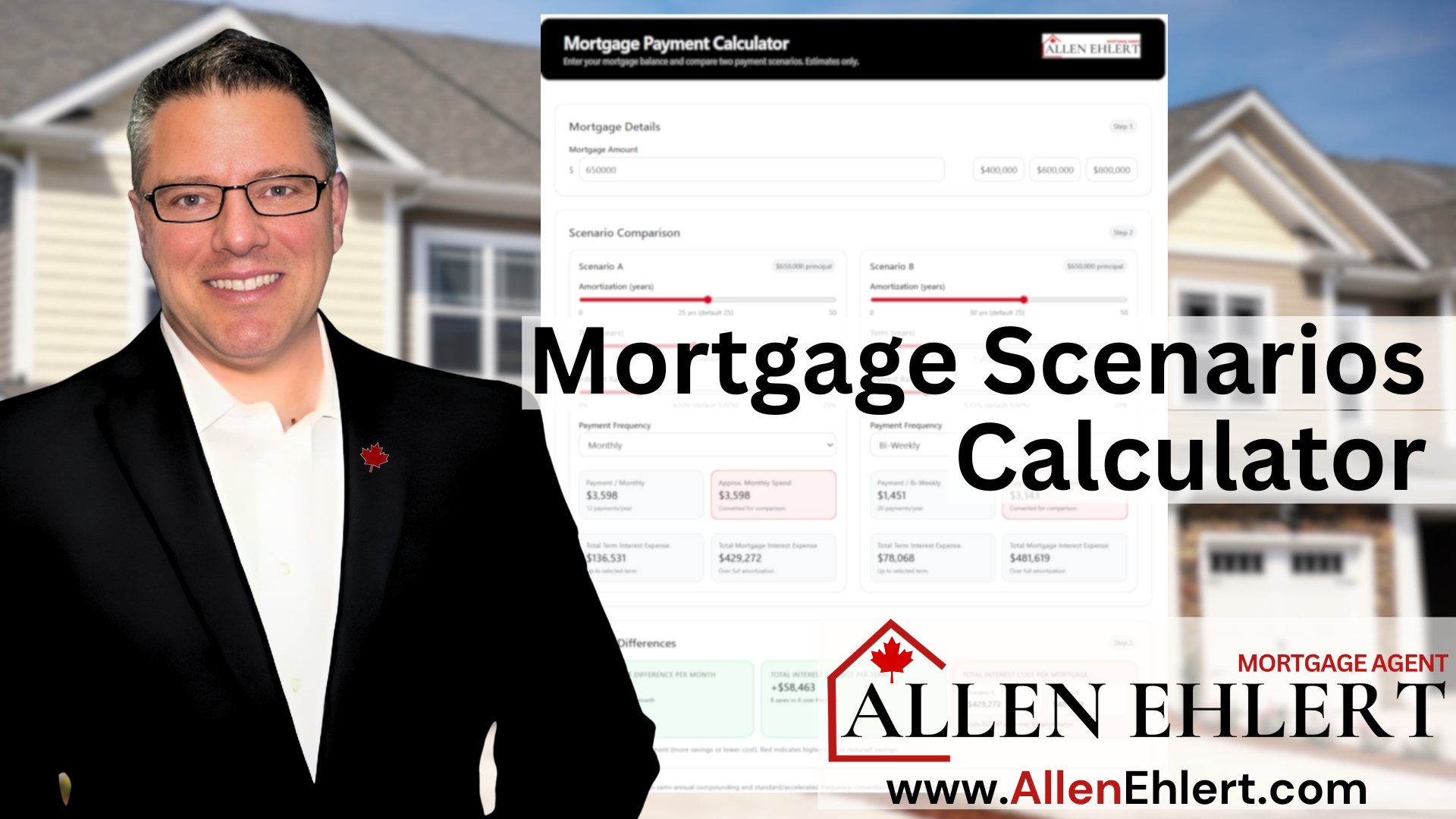

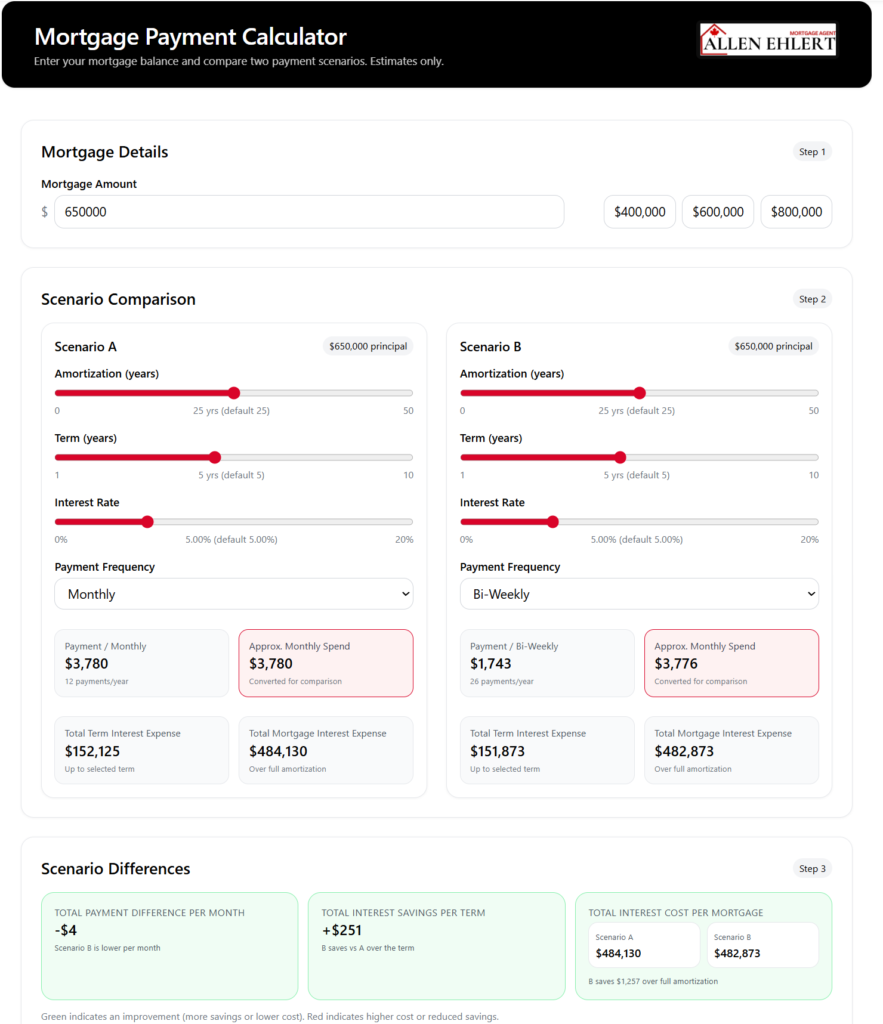

That’s why I built the Mortgage Payment Scenarios Calculator. It’s not just about crunching numbers—it’s about putting you in the driver’s seat. You can run scenarios, compare your current mortgage to a new one, or even pit different lenders against each other. The best part? It shows you not only how your monthly payments stack up, but also how much interest you’ll save (or pay) over the term and the entire life of your mortgage.

Here’s what we’ll cover today:

Why Comparing Mortgages Matters

How the Calculator Works (And What It Shows You)

A Realtor’s Secret Weapon at Renewal or Refinance

A Story: Tom and Maria’s Mortgage Makeover

Putting the Numbers Into Practice

Why Comparing Mortgages Matters

Here’s the deal: not all mortgages are created equal. Two lenders might offer the same rate on paper, but when you factor in term length, amortization, prepayment privileges, and renewal options, the difference in what you pay—or save—can be massive.

Most people stick with their bank out of habit, never realizing they could shave years off their mortgage or save thousands in interest. Comparing isn’t just smart—it’s money in your pocket.

How the Calculator Works (And What It Shows You)

This isn’t your average “plug in your mortgage amount and rate” tool. My calculator lets you:

- Run Scenarios: Change rates, terms, amortizations, or payment frequencies to see how your payments shift.

- Compare Current vs. New Mortgage: Find out if breaking your existing mortgage and switching saves you money—even after penalties.

- Stack Lenders Side by Side: At renewal or refinance, compare different lender offerings to see who’s really giving you the better deal.

- See Interest Savings Clearly: Break down the difference in total interest over the next term and the entire life of your mortgage.

It’s like having a financial crystal ball—you see not just what happens today, but how today’s choice ripples into tomorrow.

A Realtor’s Secret Weapon at Renewal or Refinance

For realtors, this tool is gold when working with clients who are upsizing, downsizing, or investing. You can use it to show them how freeing up equity or changing their mortgage structure impacts cash flow.

Imagine sitting with a couple who want to buy a second property. Instead of guessing, you run the numbers and demonstrate how refinancing their current mortgage at a sharper rate saves interest and unlocks funds for a down payment. That kind of clarity turns “maybe someday” into “let’s do it now.”

A Story: Tom and Maria’s Mortgage Makeover

Tom and Maria had a $500,000 mortgage with their bank at 5.5%. Their renewal letter arrived with a “preferred offer” at 5.2%. They figured it was decent—until they tried my calculator.

They entered their numbers and compared the bank’s offer to another lender’s 4.9% with better prepayment options. The results were eye-opening:

- Monthly payment difference: about $150 lower with the new lender

- Term interest savings: almost $9,000

- Lifetime interest savings: over $40,000

Armed with that data, Tom and Maria switched lenders. They now pay less each month and know they saved enough money to cover their kids’ future university tuition.

Putting the Numbers Into Practice

Here’s how you can use the calculator in real life:

- Homeowners at Renewal: Compare your bank’s “take it or leave it” offer against other lenders.

- First-time Buyers: Test different down payment and amortization scenarios before committing.

- Realtors: Use it in consultations to show buyers how financing choices impact affordability.

- Investors: Run multiple scenarios to see how changing terms affects long-term profitability.

- Families Considering Refinance: See how restructuring debt into a mortgage impacts monthly payments and overall interest.

It’s like test-driving a car—you wouldn’t buy it without knowing how it handles. Why would you lock into a mortgage without knowing the full picture?

Allen’s Final Thoughts

Mortgages aren’t just about rates—they’re about strategy. My Mortgage Payment Scenario Calculator pulls back the curtain and shows you exactly how different choices affect your payments, your interest costs, and your financial future.

As your mortgage agent, I go one step further. I’ll help you interpret those results, negotiate with lenders, and design a mortgage strategy that fits your life—not the other way around. Whether you’re renewing, refinancing, or buying for the first time, I’ll help you cut through the noise and focus on what really matters: saving money, building equity, and keeping your financial plan on track.

Because at the end of the day, it’s not about just getting a mortgage—it’s about getting the right mortgage for you.