Ever feel like your mortgage lender waits until the last possible minute to send you that renewal offer? You’re not imagining it. There’s actually a legal minimum for how much notice they need to give you, but that doesn’t always mean you’ll have a lot of time to weigh your options. If you’re coming up on your mortgage renewal and wondering what your rights are, you’re in the right place. Let’s break it down so you can be better prepared when that renewal envelope (or email) lands in your lap.

Let’s go over:

What’s a Mortgage Renewal Offer?

When Do Lenders Have to Send It (Legally)?

What Are They Required to Include?

What If You Haven’t Received It?

When Should You Start Shopping for a Better Mortgage?

What’s a Mortgage Renewal Offer?

When your mortgage term is nearing its end—usually every 5 years in Canada—your lender will send you a renewal offer. This is their way of saying, “Hey, your term is ending, here’s what we’re offering for the next round.” It typically includes a new rate, new term options, your new monthly payment, and how long you have to respond.

The renewal offer is your lender’s default pitch to keep you around. But just because it’s the easiest option doesn’t mean it’s the best one. More often than not, it’s not even close to their best rate.

When Do Lenders Have to Send It (Legally)?

Under Canadian law, federally regulated lenders (like the Big 6 banks and trust companies) are required to send you a renewal statement at least 21 days before the end of your mortgage term. This rule comes from the Financial Consumer Agency of Canada (FCAC).

By law (see FCAC Guideline: Mortgage Repayment and Renewal Disclosure) “If a mortgage is eligible for renewal, the federally regulated financial institution must provide the borrower with a renewal statement at least 21 days before the end of the existing term.”— Financial Consumer Agency of Canada (FCAC).

So, legally speaking, they have to give you 3 weeks’ notice. That’s it.

Now, if you ask me, that feels more like a courtesy heads-up than a real opportunity to explore your options. Some lenders might send it out 30 or even 60 days early, but many wait right up until the 21-day mark.

What Are They Required to Include?

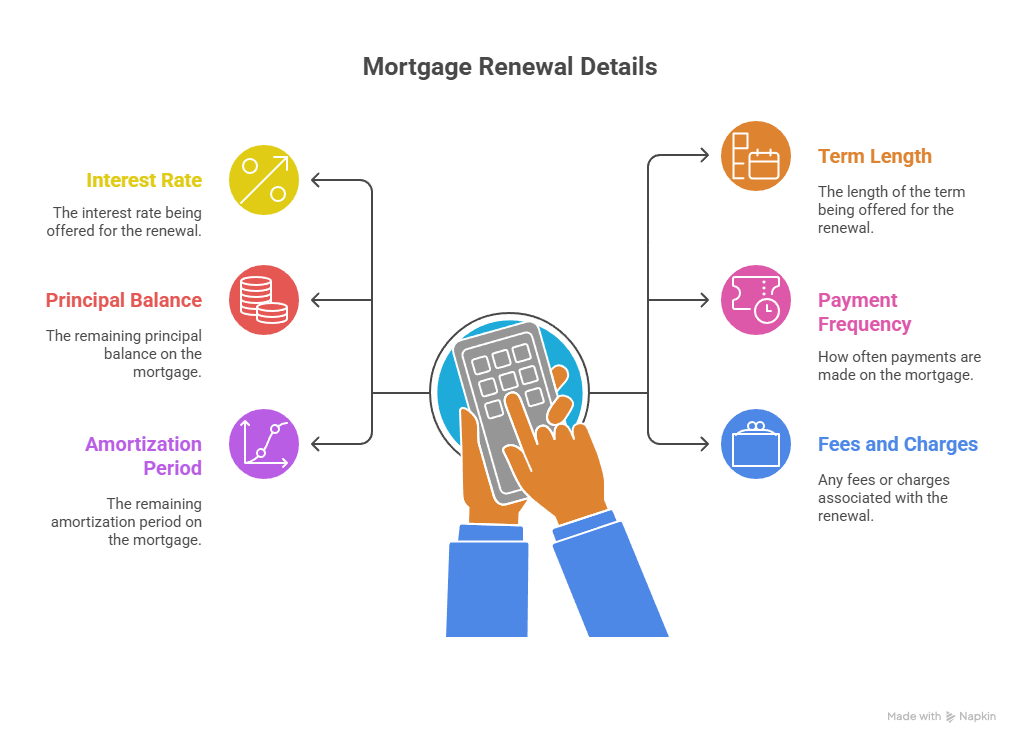

Your lender can’t just slap a number on a sheet of paper and call it a day. By law, the renewal offer must clearly state:

- The interest rate

- The term length being offered (e.g., 1 year, 3 years, 5 years)

- The remaining principal balance

- The payment frequency

- The amortization period remaining

- Any fees or charges associated with the renewal

It must be provided in writing, either by mail or electronically (depending on how you’ve opted to receive official documents).

What If You Haven’t Received It?

If you’re within 30 days of your renewal date and haven’t heard a peep from your lender, it’s time to pick up the phone. Mistakes happen. Letters get lost, emails go to spam, systems glitch. But don’t assume silence means everything’s fine.

Also—and this is key—just because your lender hasn’t contacted you yet doesn’t mean you can’t start shopping around. In fact, the smartest time to start looking at your renewal options is 120 days before your mortgage term ends. That gives you time to lock in a great rate, switch lenders if necessary, make changes that adjust to the current or anticipated realities of your life, and make a calm, informed decision instead of scrambling last minute.

When Should You Start Shopping for a Better Mortgage?

A good rule of thumb: start reviewing options at least 120 days before renewal. That’s when most lenders will hold rates, and you can really start exploring alternatives. This gives you time to:

- Compare options

- Requalify if needed

- Coordinate appraisals or docs

- Strategically negotiate with current lender

By starting at least 120 days before renewal, time is on your side.

General rule of thumb is:

30+ days before maturity? You have lots of options and leverage

15-20 days? Still doable, but it’s all hands on deck, and you better be able to deliver those docs fast!

Less than 10 days? Risky. It’s now on rush basis and many lenders will simply not accept the file. You may be forced to default into your current lender’s higher renewal rate… OUCH!

Allen’s Final Thoughts

Here’s the bottom line: your lender is legally required to send your renewal offer 21 days before your term ends, but that doesn’t mean they’ll give you a great deal—or much time to act. That 3-week window is often just enough time to panic and sign whatever’s in front of you.

But you’re not stuck. You have options. And the earlier you explore them, the better the outcome. Don’t wait for your lender to do you any favours. Take control of your renewal.

How I Can Help

As your mortgage agent, I’m not just here to react to whatever your bank sends you. I’m here to help you:

- Start the renewal process early (120 days out!)

- Review your lender’s offer and compare it to what’s available elsewhere

- Negotiate a better rate or term that actually fits your life

- Switch lenders smoothly if the numbers make sense

- Re-amortize or access equity if your financial goals have changed

Let’s make sure your next mortgage works for you, not just your lender. Reach out as soon as you’re 4 months from renewal and we’ll put a plan together—on your terms.