Personal Finance

Securing Your Today and Tomorrow

The Surge in Private Mortgages

Surge in Private Mortgages: If you’re a homeowner, buyer, realtor, or financial professional, you’ve probably felt it already. Deals are more complex. Financing conversations are happening earlier. And outcomes that used to be automatic now require real strategy. That’s not a slowdown—it’s a shift.

The 10 Principles of APR

10 Principles of APR: But APR — the Annual Percentage Rate — is where the real truth lives, not in the advertised rate—which is NOT what you pay. APR exists to answer a more important question: what does this mortgage actually cost once everything required is accounted for?

Is Your Mortgage Rate Lying to You?

Is Your Mortgage Lying? The interest rate is only part of the story. The real story—the one that tells you what the mortgage actually costs you—is hidden in a number most people barely glance at: APR.

My World of Shadow Banking

… Inside the Black Box of Mortgage Lending and Real Estate Finance Most Canadians think mortgages are simple. You walk into a bank, talk to someone behind a desk, sign some papers, and that’s that. Clean. Simple. Straightforward. That’s so yesterday! But the truth—one...

Prime Rate Panic-Proofing

Prime Rate Impact Calculator: If you’ve ever watched the news, heard “rates are moving,” and felt your stomach drop a little—yeah, you’re not alone. Most Canadians don’t actually need more opinions about interest rates. They need clarity. That’s exactly what my Prime Rate Impact Calculator is built to do: turn prime-rate chatter into real numbers you can understand, stress-test, and use to make smart decisions

What a Mortgage Agent Does

What a Mortgage Agent Does: My world of real estate finance is like a black box to most people, including financial professionals like bankers, lawyers, accountants, and financial planners. Sure, they might have some high-level exposure and education to the general concepts around real estate finance and mortgages in particular, but how my world works from the inside and what really goes on is a mystery and hidden from public view, especially that part of my world that is shadow banking.

10 Big Benefits of Going Variable

Variable Mortgages. If you’ve ever surfed—or even watched someone surf—you know it’s all about balance. You don’t fight the wave; you ride it. That’s exactly what it feels like to hold a variable-rate mortgage. Sure, the water can get choppy, but if you’ve got good footing, it can take you further, faster, and often cheaper than the safer route.

Canadian Land Transfer Tax Calculator

Land Transfer Tax Calculator: Buying a home in Canada is a thrilling adventure — whether it’s a downtown condo, a family home in the suburbs, or a cabin near the lake. But between deposits, inspections, and closing paperwork, there’s one cost that often catches buyers off guard: the Land Transfer Tax (LTT).

Home Carrying Cost Calculators

… Understanding Carrying Costs: The Unsung Hero of Smart Homebuying When most people think about buying a home, they focus on one number—the price tag. But seasoned buyers, realtors, and mortgage professionals know that the real story lies beneath the surface. The...

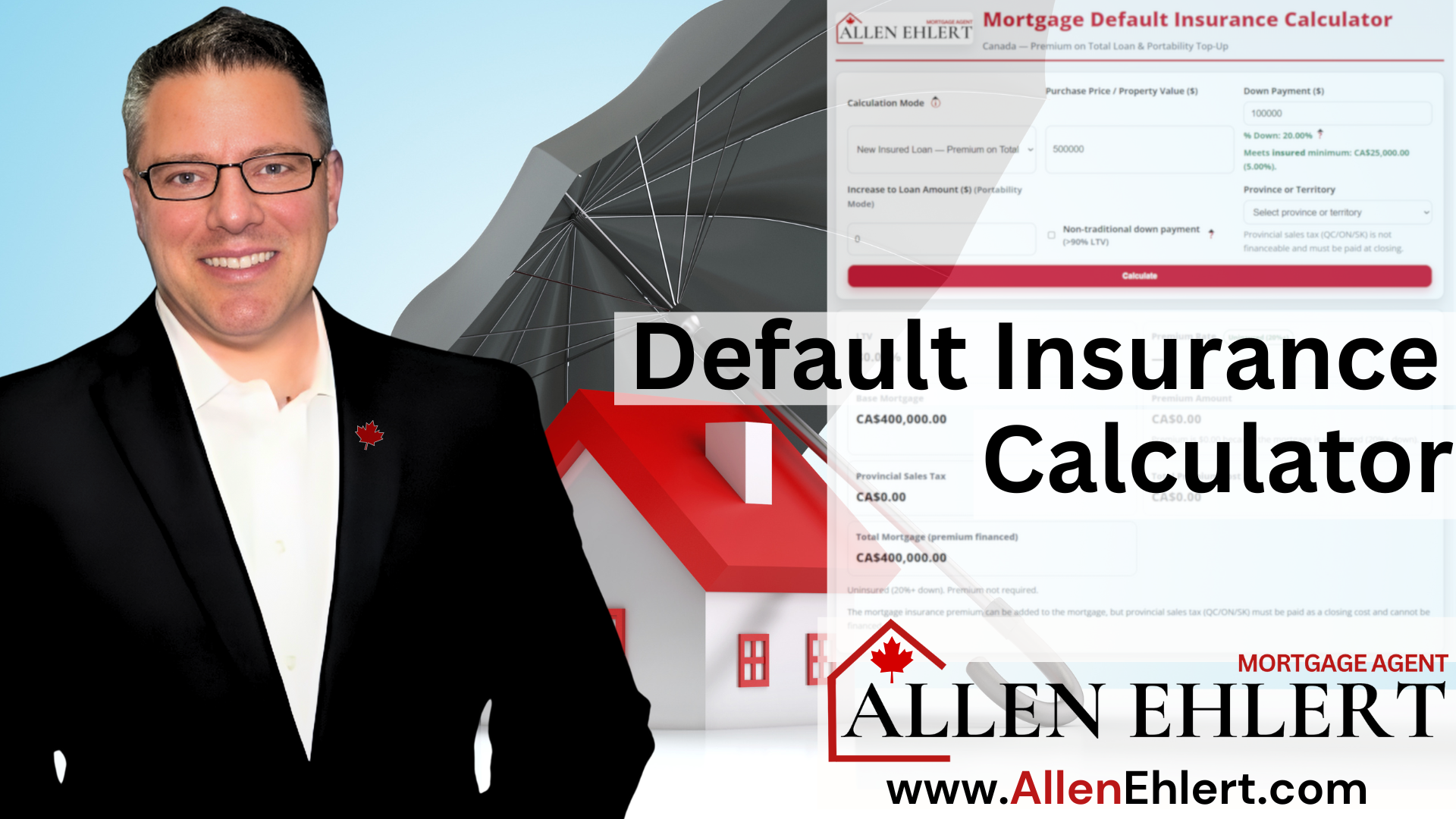

Mortgage Default Insurance Calculator

Mortgage Default Insurance Calculator: Buying a home in Canada can feel like stepping into a maze of numbers, acronyms, and fine print — but it doesn’t have to. Whether you’re a first-time buyer or a seasoned investor, understanding how default insurance works is key to knowing your real costs and options.

Canadian Closing Costs Calculator

Canadian Closing Costs Calculator: Buying a home is one of those life-changing moments that’s equal parts thrilling and nerve-wracking. Between scrolling listings, making offers, and imagining your first morning coffee in the new kitchen, it’s easy to overlook one key detail — closing costs. These aren’t the fun, HGTV-type parts of buying a home, but they’re essential.

How to Use My Mortgage Discharge Cost Calculator

Mortgage Discharge Calculator: This tool is designed to help you see—clearly and early—what it actually costs to remove a mortgage from title, based on the type of lender you’re dealing with. Whether you’re refinancing, switching lenders, selling a property, or restructuring debt, knowing these numbers in advance puts you back in control.

Non Resident Tax Rebates (NRST, NRPDTT, BC PNP, etc.)

Foreign Buyer Tax Rebates (NRST, NRPDTT, BC PNP): When you first arrive in Canada, buying a home feels like crossing the finish line of a marathon—only to realize there’s another race waiting at the starting line: understanding the taxes, rebates, and programs that affect newcomers. One of the biggest hurdles foreign buyers face in Ontario is the Non-Resident Speculation Tax (NRST)—a hefty 25% charge on residential property purchases by non-residents.

Why My Pre-Approval Is Better

Pre Approval: When you’re getting ready to buy a home, that pre-approval letter feels like a badge of honour — proof that you’re serious, qualified, and ready to make your move. But here’s what most buyers (and most realtors) don’t realize: not all pre-approvals are created equal.

Why You Need a Mortgage Agent

Mortgage Agent. Buying a home isn’t just a purchase—it’s a leap into the next chapter of your life. And with rates swinging, rules tightening, and mortgage options multiplying faster than smartphone models, you deserve someone who’s dedicated to you and no one else. That’s where a mortgage agent steps in—your advocate, your strategist, your buffer against costly mistakes.

Stop Scrolling Realtor.ca

Get a Mortgage Agent first: Most people start their homebuying adventure exactly backwards. They hop onto Realtor.ca, fall in love with a gorgeous kitchen, picture their dog in the backyard, and then—usually with a little dread—they think, “Okay… how do we actually pay for this and what can we afford?”

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate