…APR: The Number That Exposes the Real Cost of Your Mortgage

If you’ve ever shopped for a mortgage, you’ve probably been hit with a shiny interest rate that sounds great—almost too great. And here’s the uncomfortable truth: sometimes it is. The interest rate is only part of the story. The real story—the one that tells you what the mortgage actually costs you—is hidden in a number most people barely glance at: APR.

But there is a wider problem, Ontario’s regulator found more than half of the mortgage files looked at had some form of APR disclosure issue—either too low, too high, or poorly explained. Other regulators across the country identify similar issues. This means that Canadians are regularly not being told what the true cost of their mortgage.

APR exists because borrowers deserve clarity. And yet, time and again, regulators across Canada have found that clarity is missing, incomplete, or misunderstood. Let’s fix that.

Topics I’ll Uncover in this Article:

What APR is (and what it isn’t)

Why Canadian mortgage compounding matters

What APR must include to be compliant

Why regulators stepped in across Canada

How APR gets misused or misunderstood in the real world

A Story That Plays Out Every Day

How realtors and clients can use APR properly

Where a Professional Mortgage Agent Changes the Outcome

What APR Is (and What It Isn’t)

APR stands for Annual Percentage Rate, and in plain English, it’s the total annual cost of borrowing, expressed as a percentage.

Here’s the key distinction most people miss:

- The interest rate tells you how interest is calculated.

- APR tells you what the mortgage truly costs once mandatory fees are included.

APR is not a marketing number. It’s a disclosure number. It exists so you can compare apples to apples—even when one mortgage hides fees behind a “low” rate and another doesn’t.

And no, APR is not optional. In Ontario and most other provinces, it is legally required to be disclosed before you commit to a mortgage.

Why Canadian Mortgage Compounding Quietly Changes the Math

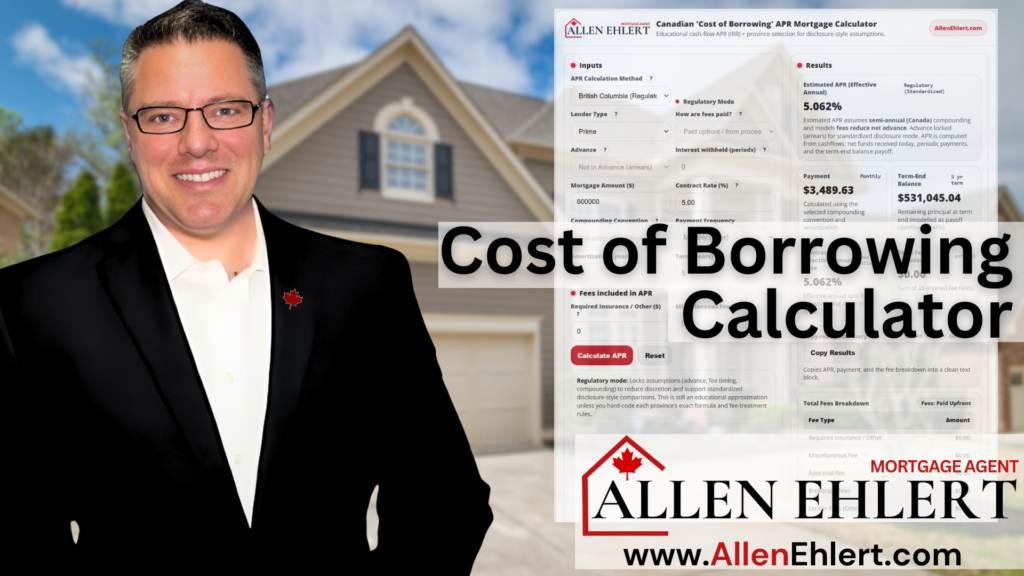

In Canada, mortgage rates are quoted as nominal rates compounded semi-annually, not monthly. That alone means a “5.00%” mortgage is already costing you more than 5.00% on an effective annual basis.

Before fees even enter the picture:

- A 5.00% Canadian mortgage actually costs about 5.06% annually once compounding is considered.

APR captures this reality. The posted rate does not.

What APR Must Include to Be Legitimate

A compliant APR disclosure generally includes:

- The interest rate (with proper compounding)

- Lender fees

- Brokerage fees paid by the borrower

- Certain administrative or underwriting fees

- Some insurance-related charges when required to obtain the mortgage

APR does not represent total homeownership cost. It doesn’t include property taxes, utilities, or optional services. It focuses strictly on the cost of credit.

When fees are real, APR must reflect them. When they’re left out, the disclosure is wrong—full stop.

Why Regulators Across Canada Stepped In

Ontario’s regulator found a pattern that should make everyone uncomfortable:

- APRs were frequently understated

- Mandatory fees were often excluded

- Some APRs were shown as estimates without being labelled as such

- In many cases, borrowers could not reasonably understand the true cost of their mortgage

Inaccurate APR Disclosure Is Common

FSRA’s preliminary examinations revealed significant problems in how mortgage annual percentage rates (APR) are being calculated and disclosed to borrowers:

- 36% of reviewed files had an understated APR because required fees were not included.

- 37% of files included estimates of APR that were not clearly labelled as estimates.

- 21% of files showed an overstated APR due to extra charges being incorrectly included.

In other words, more than half of the mortgage files FSRA looked at had some form of APR disclosure issue—either too low, too high, or poorly explained

What’s important is this: Ontario is not unique.

Other provinces—British Columbia, Alberta, Manitoba, Nova Scotia, and others—have similar cost-of-borrowing rules. The difference is that Ontario’s regulator has been more public and more aggressive in calling out non-compliance.

The takeaway? APR errors are not fringe mistakes. They are systemic.

How APR Gets Misused in the Real World

Here’s where things go sideways:

- A low rate is advertised loudly

- Fees are disclosed quietly—or separately

- APR is buried in fine print or shown late

- Borrowers focus on payment and assume all else is equal

This isn’t always malicious. Often, it’s a mix of habit, misunderstanding, and incentives that reward speed over clarity.

But the impact is real. Borrowers make decisions based on incomplete information.

A Story That Plays Out Every Day

A couple I’ll call Mark and Sarah were renewing their mortgage. Their bank offered them a rate that beat every competitor by 0.20%. It felt like a no-brainer.

Then we looked at the details.

The bank mortgage had:

- A higher APR

- Embedded administrative fees

- A restrictive penalty formula

- No flexibility to restructure later

The competing option had a slightly higher rate—but a lower APR and far better long-term flexibility.

Mark’s words stuck with me:

“We almost took the cheaper-looking mortgage without realizing it actually cost more.”

That’s exactly why APR exists.

How Realtors and Clients Can Put This Into Practice

For realtors:

- Ask for the APR, not just the rate

- Encourage clients to compare APR side by side

- Flag deals where the APR jumps noticeably above the rate

For clients:

- Don’t assume the lowest rate is the cheapest mortgage

- Ask what fees are included in the APR

- Treat APR differences as a signal to ask better questions

This is how you move from rate shopping to mortgage decision-making.

Where a Professional Mortgage Agent Changes the Outcome

A good mortgage agent doesn’t just hand you numbers. They translate them.

Here’s what I do differently:

- I explain why the APR is what it is

- I show you how fees, penalties, and structure affect long-term cost

- I flag compliance issues before they become financial surprises

- I help you compare mortgages based on reality, not marketing

APR isn’t about fear. It’s about informed consent.

Allen’s Final Thoughts

APR is the truth teller of the mortgage world. It’s the number that strips away clever advertising and shows you what you’re actually paying.

If APR isn’t clearly disclosed, clearly explained, and clearly understood, the mortgage conversation is incomplete—no matter how good the rate looks.

My role isn’t to sell you a mortgage. It’s to help you understand the one you’re choosing—fully, clearly, and confidently.

If you want help:

- Interpreting APR properly

- Comparing mortgages beyond the rate

- Avoiding costly surprises at renewal or payout

- Or simply making sure you’re seeing the whole picture

That’s exactly what I’m here for.