… Discover the impact debt consolidation can have on your financial security

High-Interest Debt Is Loud. Home Equity Is Quiet. This Calculator Shows You the Difference.

Debt rarely explodes overnight. For most Canadians, it tightens slowly—one credit card here, a car loan there—until cash flow starts feeling constrained and affordability quietly slips away. Rising interest rates have made that pressure worse, especially for households carrying unsecured debt at double-digit rates.

My Debt Consolidation Calculator is designed to bring clarity to that moment. It’s not just a comparison tool—it’s a planning and education tool. It helps you understand what options exist, when they make sense, and why timing and structure matter just as much as the rate. Used properly, it turns a vague sense of financial stress into concrete, actionable insight.

Topics Covered in This Guide

Why affordability breaks down before people realize it

The real difference between unsecured debt and secured debt

Why debt consolidation is as much strategy as it is math

What the Debt Consolidation Calculator shows you

How to use the calculator step by step

Understanding results: savings vs. extra cost

When timing matters more than the rate

How realtors and clients can use this as a planning tool

Why affordability breaks down before people realize it

Affordability isn’t just about making today’s payments. It’s about resilience—how much room you have when something changes.

Many Canadians are technically “keeping up,” but a growing share of income is being absorbed by interest rather than progress. As unsecured balances rise and rates climb, affordability erodes quietly. You don’t feel it in one big moment—you feel it in smaller decisions: delaying savings, avoiding repairs, hesitating to move, or feeling anxious every time a bill comes in.

This calculator helps surface those pressures early, before they turn into forced decisions.

The real difference between unsecured debt and secured debt

One of the most important lessons this calculator teaches is why interest rates differ so dramatically.

Unsecured debt—credit cards, personal loans, some car loans—carries high interest because there’s no collateral backing it. The lender prices in that risk.

Secured debt—mortgages, HELOCs, and some second mortgages—is backed by property. The risk profile is different, so the pricing is different. That’s why secured debt typically carries much lower interest rates.

The calculator doesn’t assume you should move debt—it simply shows what happens to the cost of interest when you change the structure.

Why debt consolidation is as much strategy as it is math

Debt consolidation isn’t a yes-or-no decision. It’s a timing decision, a structure decision, and sometimes a patience decision.

In some cases, consolidating immediately makes sense. In others, penalties, fees, or short remaining terms mean waiting produces a better outcome. This calculator is designed to help you explore those scenarios safely, without pressure.

It answers not just “What if I consolidate?” but “What if I consolidate now versus later?”

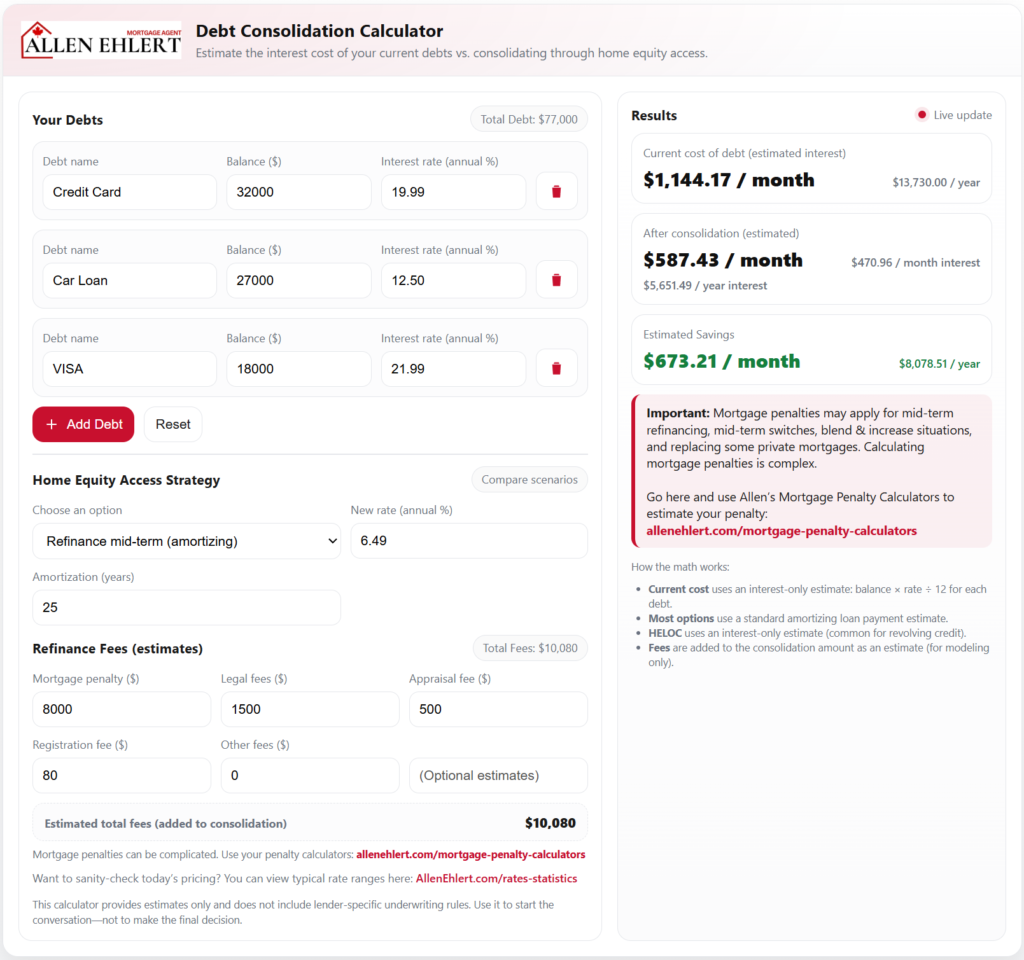

What the Debt Consolidation Calculator shows you

The calculator compares two core realities:

- Your current cost of debt (estimated interest you’re paying now)

- Your estimated cost after consolidation, based on the strategy selected

What makes it powerful is its flexibility. You can:

- Enter multiple debts with different rates

- Compare refinance, switch, renewal, HELOC, second mortgage, and private options

- See how fees and penalties affect the outcome

- Instantly identify Estimated Savings or Estimated Extra Cost

It’s not about selling an option—it’s about illuminating the trade-offs.

How to use the calculator step by step

First, enter each debt you currently carry, including balances and interest rates.

Second, select a consolidation strategy—mid-term refinance, switch at renewal, blend and increase, HELOC, second mortgage, or private options.

Third, input an estimated interest rate and review any applicable fees or penalties. The calculator adjusts automatically based on your selection.

Fourth, review the results panel to see how your interest cost changes and whether the scenario produces savings or additional cost.

Understanding results: savings vs. extra cost

When the calculator shows Estimated Savings, it means—based purely on interest—you’re paying less after consolidation than you are today.

When it shows Estimated Extra Cost, that doesn’t mean the strategy is wrong. It means under current assumptions, the timing or structure isn’t favourable yet.

That distinction matters. Knowing when not to act is just as valuable as knowing when to move.

When timing matters more than the rate

I’ve worked with many homeowners who assumed consolidation only made sense if rates dropped. Often, that’s not true.

One client—let’s call her Sarah—was carrying high-interest debt and wanted to refinance immediately. The calculator showed savings before penalties, but once the mortgage penalty was factored in, the math turned negative.

Instead of forcing a move, we used the calculator to plan for renewal. Same debts. Same house. Different timing. The result flipped from extra cost to meaningful savings.

Structure didn’t change. Timing did.

How realtors and clients can use this as a planning tool

Realtors can use this calculator to:

- Help buyers understand how existing debt affects affordability

- Support sellers considering upsizing or downsizing

- Frame smarter conversations around timing and readiness

Clients can use it to:

- Explore options without pressure

- Understand whether equity access helps or hurts

- Enter mortgage conversations informed instead of overwhelmed

Allen’s Final Thoughts

This calculator isn’t about pushing consolidation—it’s about clarity. Debt decisions are rarely black and white, and the right move today may be the wrong move six months from now.

As a mortgage agent, my role is to help you interpret these results, understand the hidden layers—penalties, fees, lender rules—and choose a path that aligns with your real life, not just a rate sheet. Whether that means acting now, waiting for renewal, or simply planning ahead, the goal is the same: stronger affordability and fewer surprises.

The calculator starts the conversation. I’m here to help you finish it—strategically, calmly, and with confidence.