Canadians seem to pay more for a lot of things. Canadians pay an outrageous amount for taxes and are often cited as paying some of the highest prices in the world for cell phone plans, among other things.

So how does the cost of refinancing your mortgage in Canada compare to refinancing your mortgage in the United States?

In Canada, refinancing your mortgage typically requires breaking your existing mortgage. When you refinance, you are replacing your current mortgage with a new one, which usually involves paying off the existing loan and setting up a new mortgage agreement. This process generally triggers the need to break the existing mortgage contract.

What Happens When You Break Your Mortgage

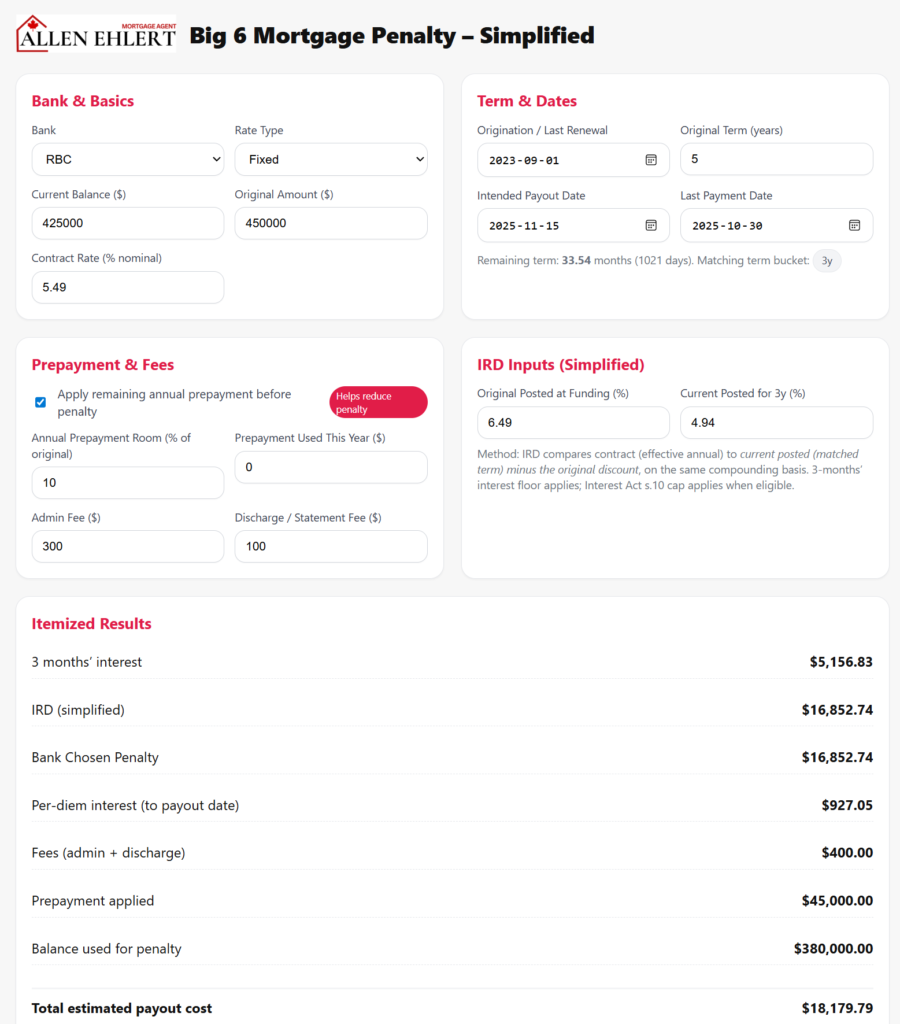

When you break your mortgage to refinance, you may be subject to penalties, such as an interest rate differential (IRD) penalty if you have a fixed-rate mortgage, or a three-month interest penalty if you have a variable-rate mortgage. The specific penalty depends on the type of mortgage and the terms of your agreement.

Refinancing allows you to negotiate new terms, such as a lower interest rate, a different amortization period, or access to home equity. However, the benefits of refinancing need to be weighed against the cost of the penalties and any associated fees.

NOTE: Break Mortgage Alternative. Some lenders offer a “blend and extend” option, where you can combine your existing mortgage rate with the current market rate and extend the term of your mortgage without fully breaking it. This option can sometimes reduce or eliminate penalties, but the blended rate might not be as low as the best available rate if you were to break the mortgage.

The Big Difference

In the United States, unlike Canada, there are no penalties for breaking a mortgage that was obtained after the financial crisis of 2008. Because Americans have 30-year mortgages, there are some still around from before 2008, but penalties on these mortgages are usually subprime loans and are structured as a percentage of the remaining loan balance or a set number of months worth of interest.

In 2010, in the USA, the Dodd-Frank Wall Street Reform and Consumer Protection Act placed significant restrictions on prepayment penalties. For example, prepayment penalties are generally only allowed within the first three years of the loan and are capped at certain levels. Many standard mortgages do not include these penalties at all.

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 implemented significant changes to the U.S. financial regulatory environment in response to the 2008 financial crisis. One of the key areas it addressed was mortgage lending practices, including the use of prepayment penalties. The Act removed or limited prepayment penalties for several reasons:

- Predatory Lending Practices

- Improved Transparency

- Economic Recovery

- Avoiding Foreclosures

- Standardization of Mortgage Practices

Predatory Lending Practices

Before the Dodd-Frank Act, prepayment penalties in the United States were often used in a way that trapped borrowers in high-interest loans, especially in subprime mortgages. Borrowers who wanted to refinance to a lower interest rate or sell their homes faced hefty penalties, making it difficult for them to escape unfavorable terms. By limiting or eliminating these penalties, the Act aimed to protect consumers from such predatory practices.

In Canada today, it can be argued that IRD penalties, especially as applied to fixed mortgages in Canada, trap Canadians in their mortgage and prevent Canadians from refinancing their homes without the payment of exorbitant fees. Banks have posted rates that are far above the actual mortgage rates they lend money out. Then, when Canadians attempt to refinance their mortgages at lower rates, banks trap Canadians in higher-rate mortgages by making them pay obscenely high IRD penalties based on those arguable false high posted rates. For example, our broker shared a scenario where it cost $100,000 for a client to break their mortgage. Being charged by the bank IRD penalties of tens of thousands of dollars to break a mortgage in Canada is typical. In the United States, such a practise is considered predatory lending. Remember, 60% of Canadians will need to refinance their mortgage sometime during their mortgage term.

Improved Transparency

The Acts in the United States sought to create a more transparent and fair lending environment. Prepayment penalties were often buried in the fine print, making it hard for borrowers to understand the full cost of their loans. By restricting these penalties, the Act made the terms of mortgages clearer and more straightforward.

In Canada, prepayment penalties are buried in the fine print and are very difficult for mortgage borrowers to understand. Often difficult calculations need to be done to determine what exactly the penalty is for a particular borrower for a particular mortgage. When clients call their mortgage agent to ask “what the penalty is to break their mortgage”, the mortgage agent must refer the client back to the lender because there is no transparency.

Not only should amortization tables be provided to Canadian mortgage borrowers, but penalty tables should also be provided so Canadians can see up front what it costs to break their mortgage with a specific lender on a specific mortgage product. Without transparency, Canadians’ ability to compare mortgage products is impaired.

Economic Recovery

The ability to refinance without facing significant penalties was seen as a way to help the economy recover. When borrowers can refinance to lower rates, they have more disposable income, which can boost consumer spending and contribute to overall economic growth.

Canadians are suffering through an affordability crisis. The cost of everything has gone up, and salaries have not kept up with the cost of everything. Canadian mortgage holders are attempting to reduce their monthly mortgage payments by increasing the amortization of their mortgages (longer amortization means lower monthly payments at the cost of a longer time you will have a mortgage). If Canadians could refinance without facing significant penalties, as in the United States, Canadians would have more disposable income, which would increase consumer spending and contribute to overall economic growth.

Read Also:

12 Reasons for Breaking Your Mortgage

Mortgage Refinance to Pay Debt

Avoiding Foreclosures

By removing barriers to refinancing in the United States, the Dodd-Frank Act helped homeowners who might otherwise have defaulted on their loans due to high payments. Refinancing to lower rates reduced monthly payments, helping more homeowners stay in their homes and avoid foreclosure.

With the jump in interest rates following the pandemic, many Canadians are facing a ‘renewal shock’ as the 1.8% mortgage rate they were paying jumps to over 5%. Many Canadians just can’t pay this and are looking at the possibility of selling their home or even possibly facing a power of sale (we generally don’t foreclose in Canada). Helping Canadians with mortgage payments as a result of a sharp increase in mortgage rates by enabling them to refinance would go a long way toward protecting Canadians from losing their homes.

Standardization of Mortgage Practices

In the United States, the Dodd-Frank Act aimed to standardize mortgage practices across the industry to prevent the kind of financial instability that led to the 2008 crisis. By removing or capping prepayment penalties, the Act reduced the variability in loan terms that could lead to financial misunderstandings or abuses.

As mentioned previously, when a client asks a mortgage agent “What is the penalty for breaking my mortgage?” the mortgage agent must generally refer the client back to the bank as only the lender knows how much the penalty is. (In truth, many Canadians don’t even know there is a penalty for breaking their mortgage. They thought they could refinance without realizing that they were listening or reading American websites or media and not knowing things are very different in Canada).

While generally, IRD penalties apply to fixed-rate mortgages, and 3-month interest rate penalty applies to variable-rate mortgages, the details of any particular mortgage product are when things are ‘unknown’. It is so complicated, there are specialty industry mortgage courses offered to mortgage agents to help them grasp the deep complexities and variations of mortgage penalty practises. If mortgage penalties were transparent and standardized across the industry, Canadians would have a clear understanding of their mortgage penalties, be better able to compare products, and be able to make better decisions for themselves and their families.

Conclusion

Canadians pay more for a lot of things, but when it comes to mortgage penalties, the difference between the penalties faced by Canadians and the lack of mortgage penalties faced by Americans is profound. By not being able to refinance your mortgage in Canada without paying exorbitant penalties for breaking your mortgage, Canadians face the same challenges today that Americans faced in 2008, before the mortgage-based financial crisis almost caused the collapse of the global economic system.