As a licensed mortgage agent dedicated to offering Canadians the best financing solutions, I understand that encountering a lender you haven’t heard of can feel unfamiliar — even a little daunting. Let’s discuss the biggest mortgage lender in Quebec who also is a growing force in Ontario— I’m talking about Desjardins, a distinguished financial institution that could be the perfect fit for your mortgage needs.

What Kind of Lender is Desjardins?

Three Powerful Reasons to Choose Desjardins for Your Mortgage

Who is an Ideal Client for Desjardins?

Who is Desjardins?

Desjardins is not just another lender; it is Canada’s largest federation of credit unions, with roots dating back to 1900. They are a financial giant in Quebec and a growing force in Ontario. As a credit union, Desjardins is fundamentally different from traditional banks — it is a cooperative, meaning it is owned by its members, not external shareholders. This unique structure prioritizes member service, stability, and community values over pure profit, resulting in a customer-centric experience.

What this implies is that Desjardins operates with a strong commitment to responsible lending, personalized service, and competitive offerings that truly put the client first.

What Kind of Lender is Desjardins?

Desjardins is a full-service credit union lender operating primarily in Ontario and Quebec. Unlike big banks that sometimes limit lending based on property location, Desjardins is far more geographically flexible, financing properties in virtually any city, town, or rural community within these two provinces. Moreover, Desjardins lends both conventionally and through insured programs (via CMHC and Sagen), including offerings for high-ratio mortgages, purchase-plus-improvements, and even vacant land financing.

As a balance sheet lender, they often hold mortgages themselves rather than securitizing and selling them off. This allows for greater flexibility in underwriting and decision-making — particularly valuable for clients with complex financial profiles.

Three Powerful Reasons to Choose Desjardins for Your Mortgage

When it comes to securing the right mortgage solution, choosing the right lender can make all the difference. Desjardins stands apart by offering a rare combination of flexibility, expertise, and member-focused service that few others in the market can match. Whether you are buying in a major urban centre or a rural community, investing in multi-unit properties, or seeking a lender who truly values your long-term success, Desjardins delivers unique advantages. Here are three compelling reasons why partnering with Desjardins could be the smartest move for your real estate financing needs.

- No Geographic or Sliding Scale Restrictions

- Exceptional Niche Lending Expertise

- Member-Focused Flexibility and Strength

No Geographic or Sliding Scale Restrictions

Desjardins will consider properties anywhere in Ontario, whether in major cities like Toronto or Ottawa, or more remote areas like Thunder Bay, Sault Ste. Marie, or the Muskokas. Unlike some lenders, they do not apply sliding scale limitations based on property value and location — a game-changer for clients buying in smaller communities.

Exceptional Niche Lending Expertise

Desjardins offers unique products that many lenders do not, such as financing for 5- to 8-unit residential properties (plexes), vacant land purchases, and new construction turnkey projects with long rate holds — up to 18 months! They are the only broker-channel lender to finance multi-unit properties of this size exclusively, making them a critical option for investors.

Member-Focused Flexibility and Strength

As a cooperative, Desjardins is deeply invested in the success of its members. They offer competitive insured mortgage products (including purchase plus improvements), customized underwriting for strong clients (even allowing exceptions to standard ratios), and a simple $5 membership fee that opens the door to full credit union services, including banking and lending.

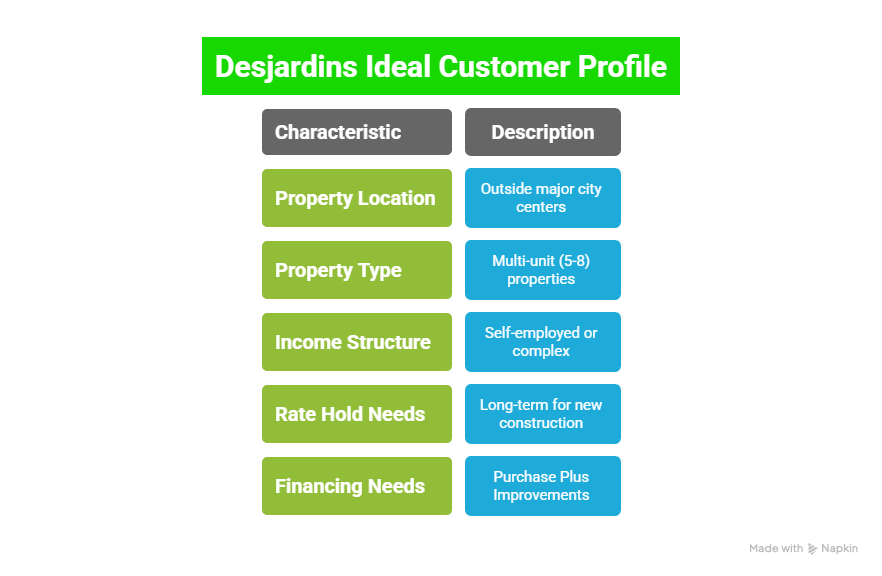

Who is an Ideal Client for Desjardins?

Desjardins is ideal for:

- Homebuyers or investors purchasing outside major city centres who face pushback from banks due to property location.

- Clients purchasing multi-unit (5-8 unit) properties who need specialized financing options.

- Self-employed individuals or clients with complex income structures who may not fit into a traditional lender’s box.

- Clients seeking long-term rate holds for new construction projects.

- Buyers needing Purchase Plus Improvements financing, both insured and conventional.

If you are looking for a lender who values flexibility, common-sense underwriting, and relationship-driven service, Desjardins could be a perfect fit.

What Sets Desjardins Apart?

What makes Desjardins unique is their commitment to both people and places. Their cooperative model allows them to put people first, offering products and solutions tailored to real life rather than strict corporate checklists. Unlike traditional banks, they are not bound by population size, location radius, or one-size-fits-all risk models.

Moreover, their niche focus — especially in vacant land, rural communities, plex properties, and turnkey construction — fills critical gaps that major banks often ignore.

Their current underwriting timelines are a known challenge — turnarounds can be slower than other lenders — but this is largely a reflection of their tremendous growth and dedication to responsible, manual underwriting practices. With internal improvements already underway, service levels are expected to improve.

My Final Thoughts

Choosing a mortgage lender is about more than just rate — it’s about flexibility, fit, and trust. Desjardins offers real solutions for real people, especially those who might be overlooked or underserved by the big banks.

If you are purchasing in Ontario or Quebec, seeking a specialized mortgage solution, or simply want a lender that treats you like a valued member rather than a number, Desjardins deserves strong consideration.

When you partner with me as your mortgage agent, I ensure you have full access to these opportunities, complete support through the process, and strategic guidance every step of the way.

If you’d like to explore whether Desjardins is right for your situation, reach out today — I would be honoured to help you move one step closer to your homeownership or investment goals.