Qualifying for a mortgage in Canada hinges on many factors, but none are as critical as income. Lenders scrutinize earnings to gauge an applicant’s financial stability and capacity to service debt. While salaried employment remains the gold standard, the modern workforce is evolving, and so are lenders’ criteria for acceptable income sources. From self-employment earnings to government benefits, a wide spectrum of income streams can support a mortgage application. Understanding the nuances of each source can significantly impact a borrower’s ability to secure financing.

Self-Employment and Business Income

Government Assistance and Benefits

Alternative and Non-Traditional Income Sources

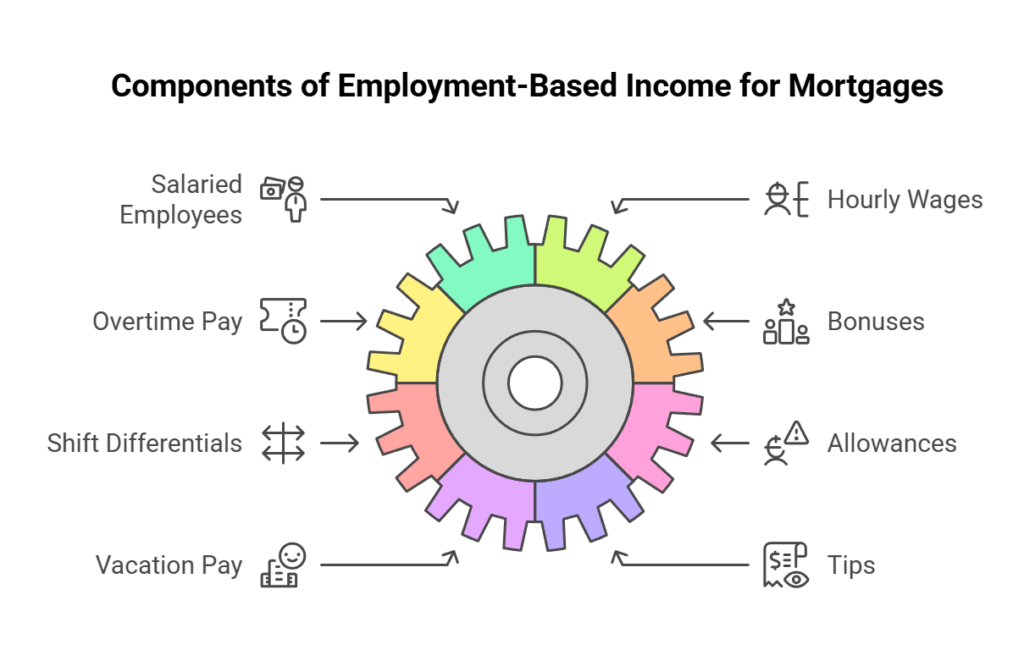

Employment-Based Income

Salaried Employees

Salaried income represents one of the most straightforward ways to qualify for a mortgage. Lenders favour the predictability of a fixed annual salary, often requiring recent pay stubs, an employment letter, and tax documents such as T4s. Borrowers with a stable, long-term position are typically perceived as low risk.

Hourly Wages

For those paid by the hour, consistency is key. If an applicant works full-time with regular hours, lenders will assess their earnings based on a recent pay stub. However, for fluctuating schedules, a two-year average—derived from tax returns—becomes the standard method of assessment.

Overtime Pay

Extra hours worked beyond a standard workweek can bolster mortgage qualification, provided they are consistent. Lenders often require a two-year history of overtime earnings, demonstrated through pay stubs and tax records, to ensure reliability.

Bonuses and Performance-Based Compensation

While bonuses can enhance an applicant’s financial profile, they introduce an element of unpredictability. Lenders typically average bonus earnings over two years, ensuring that windfall payments do not artificially inflate an applicant’s income.

Shift Differentials and Premiums

Extra income from night shifts, weekends, or holidays.

May be considered if documented on pay stubs and confirmed by the employer.

Allowances

Some lenders allow 100% of the car allowance, while others use 50%.

Must be taxable and consistent.

Vacation Pay

If paid out regularly (instead of accrued), lenders may consider it.

Tips and Gratuities

Accepted only if claimed on taxes (e.g., restaurant or hospitality workers).

Must provide T4s or NOAs showing declared income.

RRSP/RRIF or Pension Income (if still employed)

If drawing from an employer pension or RRSP/RRIF, lenders may include it as secondary income.

Second Job Income (or gig)

Considered if consistent for at least 2 years; must provide T4s, NOAs, and employer verification

Maternity/Parental Leave

Most lenders accept a full pre-leave salary if returning to work.

Letter from employer confirming return date and salary required.

Disability Income (Employer-Provided)

Long-term disability benefits may be counted if consistent and permanent.

A confirmation letter from the employer or insurance provider is needed.

Union Pay/Per Diem Pay

Both Union Pay and Per Diem Pay are forms of compensation that differ from standard salaried or hourly wages. They are common in industries such as construction, healthcare, and skilled trades.

Union pay refers to wages and benefits negotiated through a labour union on behalf of workers. Employees who are part of a union receive standardized pay rates, benefits, and protections outlined in a collective bargaining agreement (CBA).

Per diem pay refers to a daily allowance paid to employees who work on a temporary or short-term basis. This can either be:

- A set daily wage for work performed (common in contract work).

- A daily stipend to cover expenses like lodging, food, and travel (common in business travel).

Lenders assess union pay and per diem pay differently when considering mortgage applications. Union pay is generally accepted by all lenders since it is stable and based on a contract. Borrowers typically provide pay stubs, T4s, and employment verification to confirm income. Per Diem Pay is less reliable because it can be irregular or temporary. Some lenders accept it if there is a consistent history of earnings over 2 years, backed by T4s, paystubs, and NOAs.

Self-Employment and Business Income

Sole Proprietors

Entrepreneurs who operate as sole proprietors must prove business viability. Lenders assess income based on tax returns (T1 Generals) and Notices of Assessment (NOAs), usually requiring a two-year average to account for income fluctuations.

Incorporated Business Owners

Owners of incorporated businesses face additional scrutiny. Instead of traditional salaries, they may draw dividends, which lenders accept if consistently documented. Some lenders also consider retained earnings, offering flexibility in mortgage qualification.

Contract Workers and Freelancers

For those without a traditional employer, the key is demonstrating sustained earnings. A two-year income history, evidenced by tax returns, client contracts, and bank statements, strengthens an application. Some lenders may require additional proof of continued work engagements.

Commission-Based Income

Sales Professionals

Real estate agents, financial advisors, and other commission-based professionals often experience income variability. Lenders average commission earnings over two years to determine a stable qualifying income.

Real Estate Agents and Mortgage Brokers

Since earnings in these fields are directly tied to market conditions, lenders require extensive documentation, including detailed tax returns, NOAs, and business statements, to assess income reliability.

Investment and Rental Income

Dividends and Interest Income

Passive income from dividends and interest is considered, but lenders often require a documented history of consistent earnings. Tax returns and investment statements provide the necessary verification.

Rental Income

Lenders include rental income from investment properties but typically apply a percentage (e.g., 50%–80%) of the gross rent to account for expenses. A lease agreement and tax filings support the application.

Government Assistance and Benefits

Canada Pension Plan (CPP) and Old Age Security (OAS)

Retirees can use pension income for mortgage qualification. Lenders require pension statements and bank records to verify ongoing payments.

Disability Benefits

Long-term disability payments, whether from the government or private insurers, may be considered, provided they are permanent and well-documented.

Employment Insurance (EI) Benefits

Since EI is temporary, most lenders do not accept it unless tied to maternity or parental leave with a guaranteed return-to-work agreement.

Child Benefits (CCB, DTC)

Most prime and alternative lenders accept CCB as income, typically for children under 12 or 15. Government-issued benefit statements and direct deposit records support its inclusion.

If your child is eligible for the disability tax credit, you may be eligible for the child disability benefit. You could get up to $3,322 for each child who is eligible for the disability tax credit.

Alternative and Non-Traditional Income Sources

Alimony and Child Support

Court-ordered support payments may count towards income, provided they are consistent and verifiable via legal agreements and bank statements.

Foreign Income

Some lenders accept income earned outside Canada, though stringent documentation—such as international tax returns and employment verification—is required.

Combining Multiple Income Sources

Borrowers with diverse income streams can enhance mortgage affordability through income layering. Combining salary, investments, rental earnings, and benefits can optimize mortgage qualification.

Documentation Requirements

Lenders require tax documents, pay stubs, NOAs, and bank statements to verify income. Incomplete or inconsistent documentation can derail an application, making thorough preparation essential.

Key Documentation Required

For all employment income sources, lenders may request:

- Pay stubs (Employees) (typically last 30-60 days)

- T4s (1 year for salaried/hours guaranteed employees, otherwise 2 years)

- NOAs (optional for salaried/hours guaranteed employees, otherwise 2 years)

- Employment letter (confirming job title, start date, and salary/compensation)

- Bank statements (if using deposits to verify income consistency or Self Employed Stated Income Program)

While the following may be personal sources of funds, they typically cannot be used to qualify for a mortgage:

Unacceptable Income Sources

- Unreported cash income (e.g., undeclared tips)

- One-time bonuses or sporadic commissions

- EI benefits (unless it’s parental leave and you have a return-to-work date)

- One-time settlement payments (e.g., lawsuit settlements)

Conclusion

The mortgage qualification process in Canada extends beyond traditional employment income. From self-employment earnings to government benefits and passive income, numerous sources can contribute to affordability. Understanding lender preferences and documentation requirements can make the difference between mortgage approval and denial.