… The Quiet Superpower Most Homeowners Ignore

Let’s start with a reality check.

Most Canadians are living in an affordability pressure cooker. Housing costs are high. Groceries are expensive. Insurance, utilities, childcare—everything feels heavier than it did even a few years ago. At the same time, income hasn’t kept pace, and job security feels shakier than it used to.

In an environment like this, financial resilience matters more than optimization.

That’s why—despite all the cautions, caveats, and horror stories—you still need to seriously consider a HELOC before you ever think you’ll need one. Used properly, a HELOC isn’t about spending. It’s about survivability, optionality, and control.

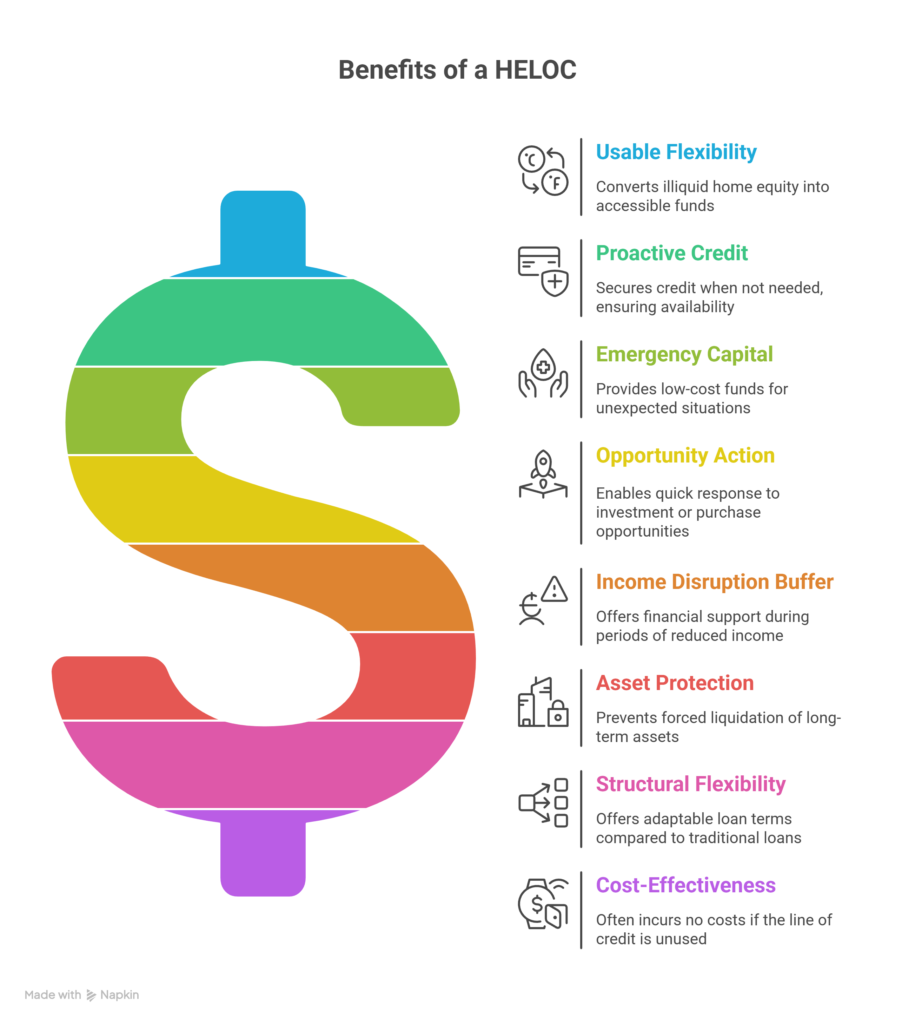

Before we go deeper, here are the eight reasons a HELOC—set up early and used responsibly—can make profound financial sense:

- A HELOC turns illiquid home equity into usable flexibility

- The best time to get credit is when you don’t need it

- It is the lowest-cost emergency capital most households can access

- It allows you to act quickly when opportunity appears

- It provides breathing room during income disruption

- It reduces the need to liquidate long-term assets at the wrong time

- It offers structural flexibility most loans don’t

- It often costs nothing if you never use it

Let’s unpack why these matter—especially right now.

A HELOC Turns Illiquid Wealth into Usable Flexibility

For most homeowners, the bulk of their net worth sits inside their home. That’s great on paper—but useless in real life unless it can be accessed.

A HELOC converts a portion of that equity into on-demand liquidity without forcing you to sell, refinance, or disturb long-term plans. You’re not borrowing—you’re pre-positioning.

That distinction matters.

Liquidity doesn’t make you reckless. Lack of liquidity makes people desperate.

The Best Time to Get Credit Is When You Don’t Need It

This is one of the most important financial truths there is.

When life is calm:

- Income is stable

- Credit is strong

- Property values are intact

- Lenders are generous

When life gets messy:

- Credit tightens

- Approvals slow

- Options disappear

A HELOC is insurance you qualify for in good times and rely on in bad ones. Waiting until you’re under pressure is often waiting too long.

HELOCs Are the Lowest-Cost Emergency Capital Most Households Can Access

When emergencies hit, speed and cost matter. Here’s how a HELOC stacks up against other common options:

| Source of Emergency Funds | Typical Cost | Speed | Long-Term Damage |

| Credit cards | Very high | Immediate | High |

| Personal loans | Medium–high | Moderate | Medium |

| Payday / short-term loans | Extreme | Immediate | Severe |

| RRSP withdrawal | Hidden (tax + lost growth) | Moderate | Permanent |

| Selling investments | Opportunity cost | Slow | Market-timing risk |

| HELOC | Low | Immediate | Low if repaid |

In an affordability crisis, having emergency capital is not a luxury—it’s a necessity. The absence of cheap liquidity is what forces bad decisions: selling assets at the bottom, taking predatory credit, or missing payments that damage credit for years.

It Lets You Act When Opportunity Appears

Opportunity doesn’t wait for mortgage approvals.

A HELOC can allow you to:

- Act quickly on discounted real estate

- Bridge short-term gaps until permanent financing is optimal

- Fund renovations that immediately improve cash flow

- Add secondary suites or income features

- Handle time-sensitive business or family opportunities

For disciplined borrowers, it’s not about leverage—it’s about timing control.

It Buys Time During Income Disruption

Job loss. Illness. Contract gaps. Business slowdowns.

Even a six-month income interruption can derail an otherwise solid household. A HELOC can provide:

- Temporary cash flow support

- The ability to stay current on obligations

- Time to make good decisions instead of panicked ones

That breathing room preserves credit, reduces stress, and protects long-term plans.

It Reduces the Need to Liquidate Long-Term Assets at the Worst Time

Pulling money from RRSPs or selling investments during downturns can permanently damage wealth.

A HELOC allows you to:

- Bridge short-term needs

- Leave long-term assets intact

- Repay when conditions normalize

Used this way, a HELOC protects—not undermines—long-term financial health.

HELOCs Are Structurally More Flexible Than Most Loans

Unlike most credit products, HELOCs:

- Have no prepayment penalties

- Allow interest-only payments if needed

- Can be paid down and reused

- Often allow portions to be locked into fixed rates

That flexibility is invaluable when life doesn’t follow a straight line.

They Often Cost Nothing If You Never Use Them

This is the part people miss.

If structured correctly:

- No balance = no interest

- No interest = no carrying cost

A HELOC can sit quietly in the background for years, unused, doing nothing except existing as a safety net.

That’s not debt.

That’s preparedness.

A Story I See Done Right

A professional couple set up a HELOC early—no urgency, no drama. Years later, one income disappeared temporarily. Instead of selling investments or missing payments, they used the line deliberately, covered expenses, and repaid it once income returned.

No panic. No permanent damage. No stress spiral.

That’s a HELOC doing its job.

What This Looks Like in Practice

For realtors

- Encourage clients to think about liquidity, not just purchase price

- Flag the value of HELOCs before life changes

- Help clients see preparedness as part of good planning

For clients

- Treat a HELOC as a safety net, not spending money

- Set rules for use before you ever draw from it

- View access as insurance—not income

How I Help You Use This Tool Properly

My role isn’t to push HELOCs. It’s to design them properly—or stop them altogether.

I help clients:

- Decide whether flexibility or constraint suits them best

- Compare HELOC structures across lenders

- Model rate increases and downside scenarios

- Set conservative limits and clear exit strategies

- Avoid products that look cheap but behave expensively

Sometimes the right advice is “yes.”

Sometimes it’s “not yet.”

Sometimes it’s “not at all.”

All three protect you.

Allen’s Final Thoughts

A HELOC isn’t about borrowing more money. It’s about giving yourself options in a world that’s getting less forgiving.

In an affordability crisis, resilience beats optimization every time. The households that struggle the least aren’t the ones with the highest returns—they’re the ones with access to low-cost emergency capital when life throws a punch.

A HELOC, set up early and used responsibly, can be that quiet backstop.

If you’re going to consider one, do it deliberately, conservatively, and with independent advice—not because you’re desperate, but because you’re prepared.

That’s how powerful tools stay helpful—and never become traps.