Renting can offer advantages over buying, such as flexibility, lower upfront costs, and freedom from maintenance responsibilities. However, for most people, renting is not a lifestyle choice; it is an economic necessity. Most people would buy something if they could. Approximately 41% of all Canadians are renters, according to the Financial Consumer Agency of Canada.

Choosing between renting and buying a home is a significant decision that depends on individual circumstances, financial goals, and lifestyle preferences. While renting can be the right choice for some, for others, in our economic environment, renting is a financial death trap that leaves renters in a perilous financial state.

Limited Control and Personalization

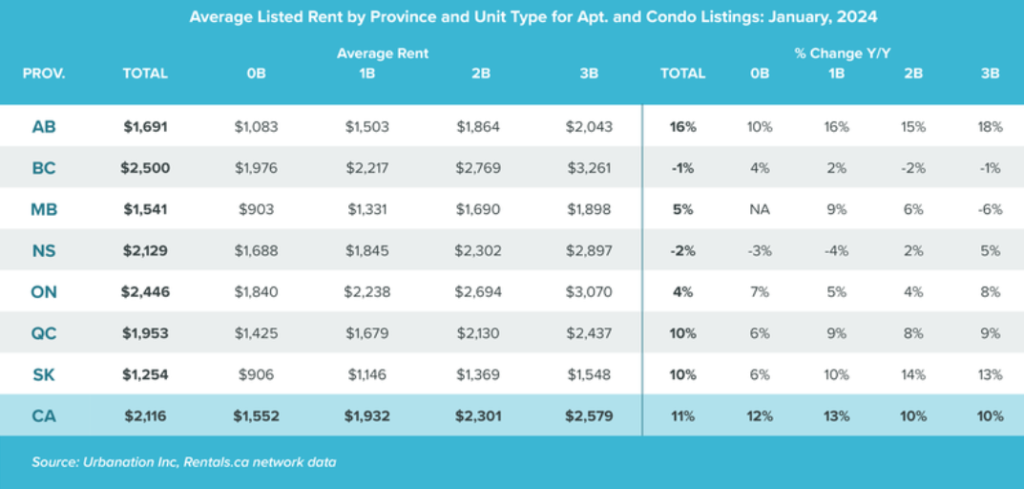

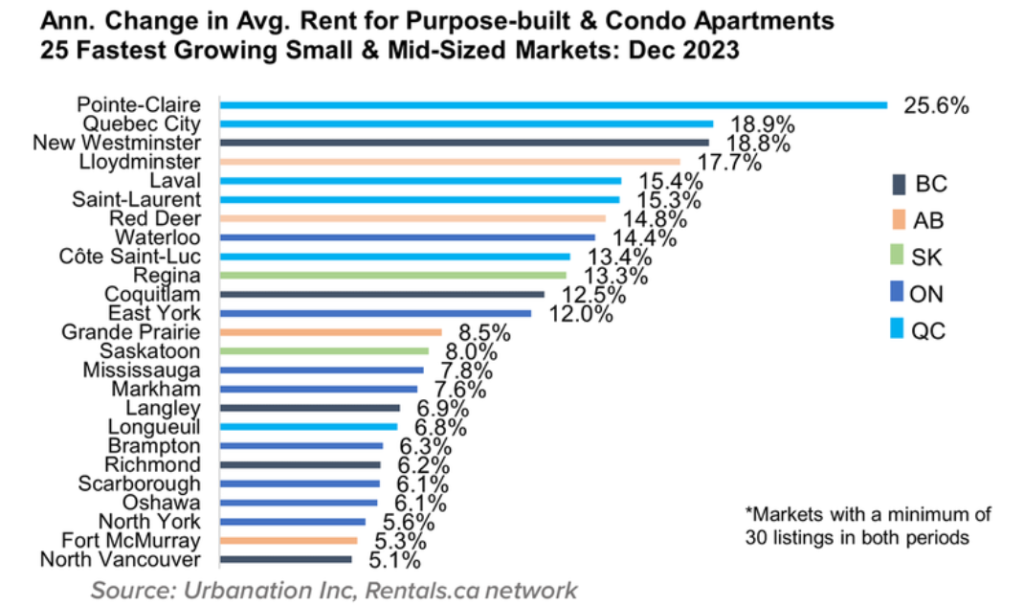

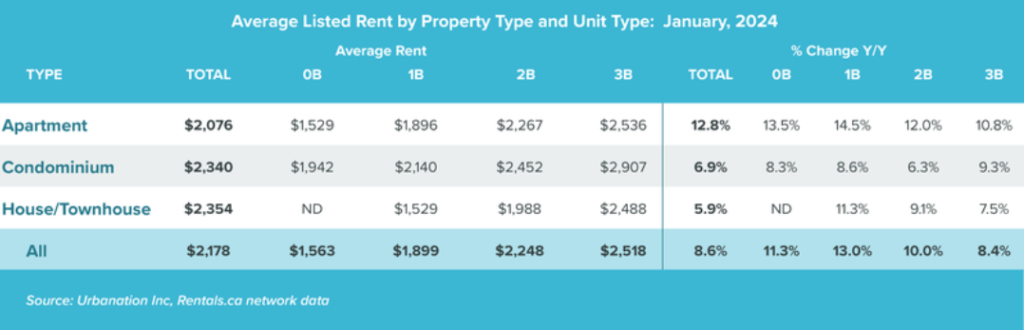

Presently, rent prices are outpacing the rate of inflation and, more importantly, the income of Canadians, and this trend will continue. Year over year, the average increase in rent across Canada was 8.6%, with much higher increases in more urban centres, and that follows a national average of a 12.1% increase the previous year. For example, Mississauga, Ontario, saw a rent increase of 10.5%, Scarborough, Ontario, saw a rent increase of 17%, and Brampton, Ontario, 18%, while Halifax saw a decline in rent of 7.4%.

Asking Rents in Canada Declined 3% in 2024

The decline in rents last year followed growth of 8.6% in 2023 and 12.1% in 2022, representing the first time that rents experienced an annual decrease since the COVID-19 pandemic in 2020 when rents fell 5.4%. Overall, rents increased by a total of 16.8% over the past five years, which equates to an average of 3.15% per year.

See: Annual Rental Report

The future looks bleak for renters. 2023 saw Canada build 7% fewer homes during a housing crisis, despite Canada’s population growing the fastest of almost any country in the world. In Toronto, where new rentals come from the condominium market, condo projects have come to a halt as investors cannot reconcile the high cost of purchase with the rent units can reasonably charge. Further, in Ontario, any unit built after 2018 is not subject to rent control, so any new units will not be ‘affordable’.

If you don’t own, you must make the necessary sacrifices, put together a budget you can commit to, and make the decision that you will get out of the rent trap or else face a perilous future where homelessness is a distinct possibility as rent increases continue to outpace incomes.

No Equity Building

Unlike homeownership, where mortgage payments contribute to building equity in the property, rent payments do not build any equity. This means that renters do not benefit from the potential appreciation in property value over time.

Your personal residence is the only real estate in Canada that appreciates tax-free. Unlike a stock, which you have to pay capital gains tax on if you sell it for more than you paid for it, you can sell your home for more than you paid and pay no capital gains. Other investments, like GICs, mutual funds, ETFs, etc., and even your bank account, all come with tax consequences. Considering how heavily taxed Canadians are, it makes complete sense that Canadians would hold most of their wealth in their homes. Real estate is the principal way Canadians build wealth.

Further, if you pay rent, you are paying someone else’s mortgage. Why not buy something, like a house, that you can rent part of and get your tenant to pay your mortgage? With a plan and working with a mortgage agent, you can discover possibilities you never knew existed.

Lack of Long-Term Security

Renting typically involves short-term lease agreements, which can lead to a lack of long-term housing security. Renters may face uncertainties like lease non-renewals, rent increases, or the need to relocate due to the property owner’s decisions.

In Ontario, Canada, the Residential Tenancies Act (RTA) governs the relationship between landlords and tenants, including the reasons a landlord can legally give to terminate a tenancy. It’s important for both landlords and tenants to understand these reasons to ensure compliance with the law. Generally, a landlord can terminate a lease for:

Landlord’s Own Use: A landlord can end a tenancy if they, a family member, or a caregiver plan to move into the unit. The landlord must provide proper notice and compensation to the tenant.

Sale of the Property: If the landlord sells the property and the buyer wants to use the property themselves, the landlord can give notice to end the tenancy, subject to specific conditions.

Renovations or Repairs: If the landlord plans to do major renovations or repairs that require a building permit and the property to be vacant, they can issue a notice to end the tenancy. Compensation or an option to move back in at a similar rent may be required.

Conversion, Demolition, or Repurposing: If the landlord plans to convert the rental property to non-residential use, demolish it, or use it for another purpose, they can terminate the tenancy, subject to certain conditions.

The unit you rent is not your home, it belongs to someone else; you are just ‘borrowing it’.

Limited Control and Personalization

Renters often have limited ability to modify or personalize their living space, as making significant changes usually requires the landlord’s permission. This can be a drawback for those who wish to create a home that reflects their personal style and needs.

What this means for your mental well-being is a constant reminder that where you are is not your home. You don’t belong here.

Rising Rental Costs

Renters are subject to fluctuations in the rental market, which can lead to periodic rent increases. In areas with high demand for rental properties, this can result in a significant financial burden over time.

In Ontario, Canada, the annual rent increase limit is set by the provincial government and is based on the Ontario Consumer Price Index (CPI). This limit applies to most residential rental properties that are covered under the Residential Tenancies Act (RTA). However, there are some exceptions, such as rental units first occupied for residential purposes after a specific date (e.g., November 15, 2018), which may not be subject to rent control.

For 2023, the rent increase guideline in Ontario was set at 2.5%. This means that landlords could increase the rent by up to 2.5% over the previous year’s rent without needing approval from the Landlord and Tenant Board. The guideline is typically announced annually and applies to rent increases that occur within that calendar year.

It’s important to note the following regarding rent increases under rent control in Ontario:

- Notice Period: Landlords must provide tenants with a written notice of a rent increase at least 90 days before it takes effect.

- Frequency of Increases: Rent can only be increased once every 12 months for a tenant.

- Exemptions: Some rental units are exempt from rent control, including those first occupied for residential purposes after a certain date. For these units, landlords can set the rent at market rates.

- Above-Guideline Increases: In certain circumstances, landlords can apply to the Landlord and Tenant Board for an above-guideline increase. This is usually allowed for specific reasons, such as extraordinary increases in property taxes or significant capital expenditures on the rental property.

- Rent Reduction: In some cases, tenants may be entitled to a rent reduction, for example, if municipal property taxes decrease by more than 2.49%.

Tenants and landlords should familiarize themselves with the specific rules and guidelines related to rent increases in Ontario to ensure compliance with the RTA. The annual rent increase guideline is subject to change each year, so it’s important to stay informed about the current limits and regulations.

Landlords are under a lot of pressure to find ways to increase rent when the revenue generated from rent no longer covers the cost of the unit, usually the result of sharp increases in interest rates.

Further, across many municipalities and cities across Canada, property taxes have increased far beyond the 2.5% rent increase cap. The law allows landlords to immediately pass on these increases to their tenants by increasing the rent.

When tenants lose their rentals due to displacement by landlords, they discover that finding another unit to rent at the same price is nearly impossible, and they have to rent something else at a much higher rent.

No Tax Benefits

Homeowners may benefit from tax deductions related to mortgage interest and property taxes, depending on local tax laws. Renters do not receive these tax benefits, which can be a financial disadvantage. For example, in Canada, many homeowners use a financial strategy called the Smith Manoeuvre to deduct mortgage interest from their taxes.

The Smith Maneuver is a financial strategy used by homeowners in Canada to convert the non-deductible interest of a residential mortgage into tax-deductible interest. This strategy involves using the equity in your home to invest in income-producing assets, with the goal of building wealth and reducing tax liability over time.

Here’s how the Smith Manoeuvre works:

- Obtain a Re-Advanceable Mortgage: The first step is to secure a re-advanceable mortgage, which combines a traditional mortgage with a home equity line of credit (HELOC). As you pay down the principal on your mortgage, the credit limit on your HELOC increases.

- Make Regular Mortgage Payments: Continue making regular payments on your mortgage. Each payment reduces the principal amount of the mortgage and increases the available credit in the HELOC.

- Borrow from HELOC to Invest: After each mortgage payment, borrow the amount by which your HELOC limit has increased and use this money to invest in income-producing assets, such as stocks, bonds, mutual funds, or rental properties.

- Generate Tax-Deductible Interest: The interest on the money borrowed from the HELOC for investment purposes is typically tax-deductible in Canada, as it is used to generate income. This can create a tax benefit by reducing your taxable income.

- Use Investment Income and Tax Refunds: Use the income generated from your investments, along with any tax refunds resulting from the interest deduction, to make additional payments on your mortgage principal. This accelerates the mortgage paydown and increases the available credit in your HELOC.

- Repeat the Process: Continue this cycle – paying down the mortgage, borrowing from the HELOC to invest, and using investment income and tax savings to pay down the mortgage faster. Over time, this can lead to a fully paid-off mortgage and a substantial investment portfolio.

- Long-Term Wealth Building: The ultimate goal of the Smith Maneuver is to build your investment portfolio while paying off your mortgage, potentially leading to increased net worth and financial security.

It’s important to note that the Smith Maneuver involves certain risks and complexities. The strategy relies on the assumption that the long-term return on investments will exceed the cost of borrowing. Market volatility, interest rate changes, and tax considerations must be carefully evaluated. Additionally, not all investments are suitable for this strategy, and the tax deductibility of interest can depend on various factors and individual circumstances.

Investment Opportunity Cost

Money spent on rent is an expense with no return on investment. In contrast, owning a home can be viewed as an investment, with the potential for the property to appreciate in value over time.

With every mortgage payment, you build wealth. That’s wealth you can use for any purpose you wish. If an unexpected life expense occurs, you can contact your mortgage agent and turn your home’s equity into cash. You can take equity out of your house to invest in a new business, or to purchase another property you can rent out.

Canada not only has a housing crisis, it has a pension crisis. Statistics Canada reports only 37% of Canadians, frequently public sector employees, have an employer-sponsored pension. Canadians are relying on the wealth they have built up in their homes, which they can access using a reverse mortgage, to give them the retirement they deserve.

When you rent, any investment opportunity or life relief is lost.

Choosing between renting and buying a home is a significant decision that depends on individual circumstances, financial goals, and lifestyle preferences. While renting can be the right choice for some, for others, in our economic environment, renting is a financial death trap that leaves renters in a perilous financial state.