In Canada, saving for a down payment is considered one of the biggest challenges for many aspiring homeowners. According to recent surveys, around 76% of Canadians planning to buy a home in the next five years say saving for a down payment is their primary financial obstacle. Additionally, nearly 60% of Canadians have started saving, which represents a drop from 76% in the previous year, highlighting the growing difficulty due to rising home prices and other economic factors. This challenge is particularly pronounced among first-time buyers, with 67% expressing concerns about their ability to save enough for a down payment.

A down payment, usually 5% to 20% of the home’s price, is key to getting an insured mortgage and buying a home, but you will have to pay mortgage default insurance (see Required Mortgage Default Insurance) which is required by law. A down payment of more than 20% does not require mortgage default insurance, and while mortgage rates for insured and uninsurable mortgages are higher (see: Insured, Insurable, Uninsurable Mortgages Explained) you don’t have to pay the expensive mortgage default insurance premium.

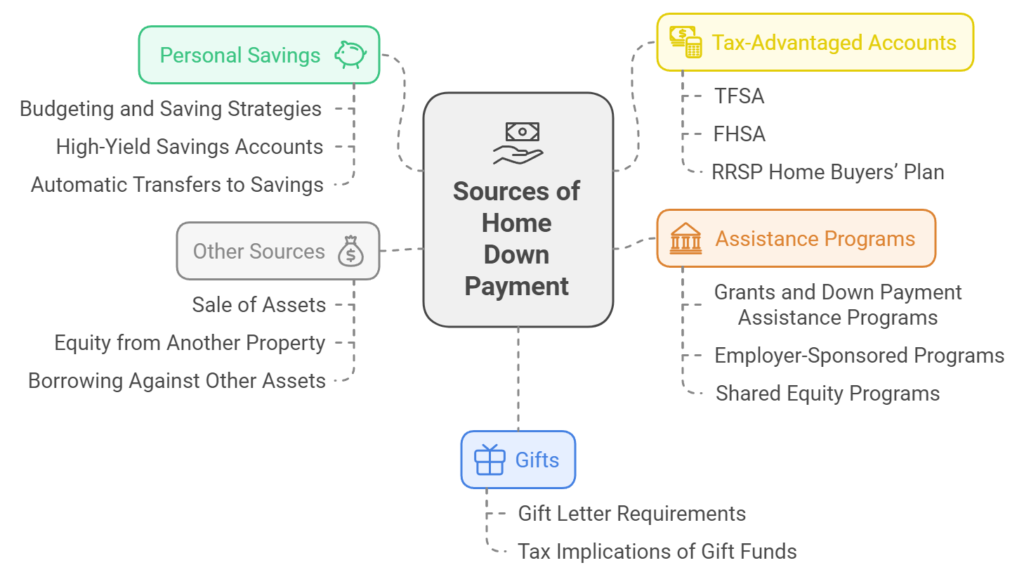

Having enough money for a down payment shows lenders you’re financially stable. It also means you’ll owe less on your mortgage. There are many ways to get the money you need, like saving yourself, getting help from family, or using grants and programs. There are also net worth programs. Lenders need to see proof of where the down payment came from as the government is aggressively stepping up enforcement through anti-money laundering legislation.

Key Takeaways

- Saving for a down payment is a significant challenge for many Canadian homebuyers

- Down payments can range from 5% to 20% depending on the home purchase price

- A larger down payment reduces the overall mortgage amount and demonstrates financial stability to lenders

- Various sources can be used to accumulate down payment funds, including personal savings, gift funds, grants, and assistance programs

- Lenders require documentation and verification of the down payment source during the mortgage application process

TFSA (Tax-Free Savings Account)

FHSA (First Home Savings Account)

Down Payment Assistance Programs

Borrowing Against Other Assets

Personal Savings

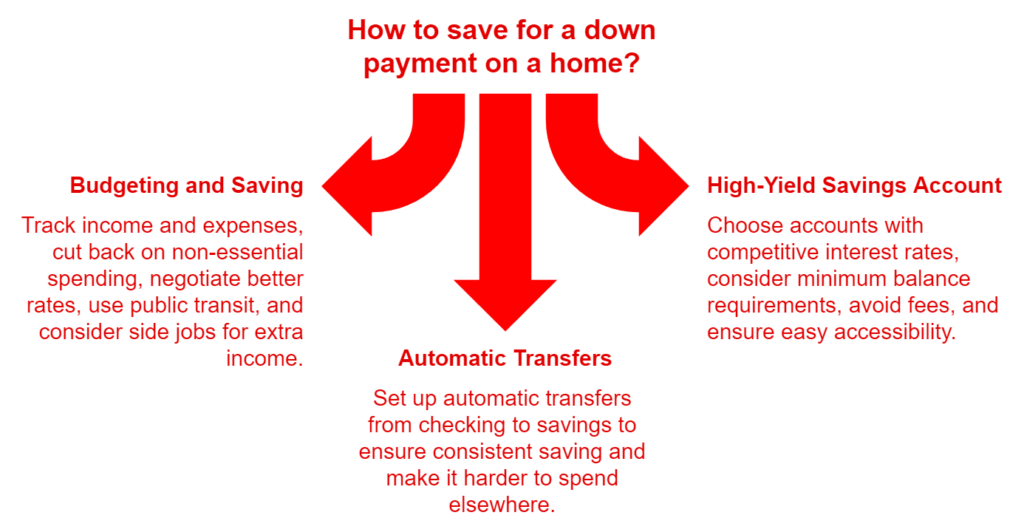

For many Canadians, saving for a down payment is key to owning a home. By setting aside a part of their income and sticking to a budget, they can save up for their dream home.

Budgeting and Saving Strategies

First, making a detailed budget is essential for saving. Tracking income and expenses helps find ways to spend less and save more. Some good strategies include:

- Cutting back on things like dining out or entertainment

- Negotiating better rates for bills like cable or insurance

- Using public transit instead of owning a car, or getting by with one car instead of two

- Getting extra income from side jobs or freelance work

High-Yield Savings Accounts

To grow your savings faster, consider a high-yield savings account. These accounts offer higher interest rates than regular savings accounts. When looking at these accounts, consider:

| Factor | Consideration |

|---|---|

| Interest Rate | Choose accounts with competitive APYs |

| Minimum Balance | Some need a minimum balance for the best rates |

| Fees | Avoid accounts with monthly or low balance fees |

| Accessibility | Make sure it’s easy to transfer money to and from your main bank |

Automatic Transfers to Savings

Setting up automatic transfers from your checking to savings is very effective. It ensures a part of your income goes to savings, making it harder to spend it elsewhere.

“Automatic transfers are a game-changer when it comes to saving for a down payment. By paying yourself first and treating your savings like any other bill, you can make steady progress towards your homeownership goals without having to think about it every month.”

Remember, saving for a down payment is a long-term effort. With careful budgeting, high-yield savings, and automatic transfers, you can build up your savings for your dream home.

TFSA (Tax-Free Savings Account)

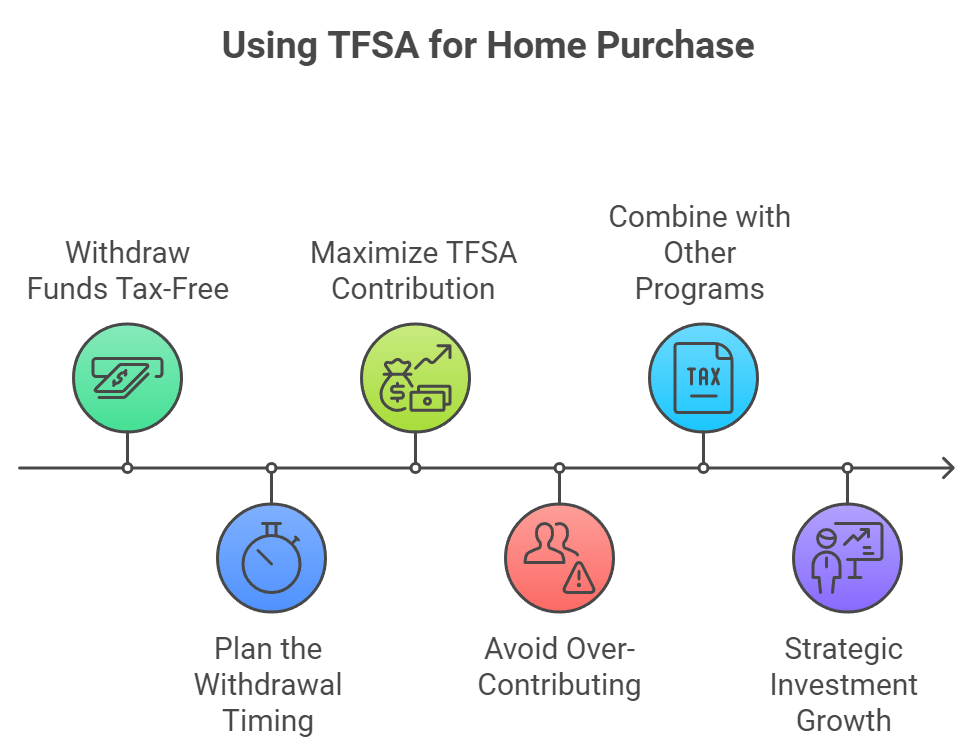

Using your Tax-Free Savings Account (TFSA) to help with a down payment on a house can be an effective strategy, given the tax-free growth of investments within the account. Here’s how you can use a TFSA to fund a down payment on a house:

1. Withdraw Funds Tax-Free

- Key Advantage: The most significant benefit of a TFSA is that you can withdraw money tax-free at any time. Unlike an RRSP withdrawal, which may incur taxes (unless you’re using the Home Buyers’ Plan), TFSA withdrawals are not taxed, making it a flexible option for home purchases.

- Process: To use the TFSA for a down payment:

- Log into your TFSA account (either through your bank or investment platform).

- Request to withdraw the amount you need for the down payment.

- You do not need to provide any reason for the withdrawal, and there are no penalties or taxes associated with it.

2. Plan the Withdrawal Timing

- Re-Contribution Room: Any amount you withdraw from your TFSA will re-add to your contribution room in the next calendar year. For example, if you withdraw $50,000 for a down payment in 2024, you will get $50,000 in new contribution room starting in 2025. This is useful if you plan to rebuild your TFSA in the future.

- Investment Liquidation: If your TFSA is invested in stocks, bonds, or mutual funds, you may need to sell those investments before withdrawing the funds. Plan your withdrawal in advance to avoid selling investments at an inopportune time (e.g., during a market downturn).

3. Maximizing Your TFSA Contribution Before Withdrawal

- Maximize Growth: Before you withdraw from your TFSA, ensure you are maximizing your contributions. As of 2024, the total lifetime contribution limit for the TFSA is $88,000 (if you’ve been eligible to contribute since the TFSA was introduced in 2009). If you haven’t maximized your TFSA, consider contributing any available cash to grow your savings tax-free before withdrawing.

- Optimizing Returns: If you’re a few years away from purchasing a home, consider investing your TFSA funds in low-risk investments such as GICs, high-interest savings accounts, or bonds to ensure the funds are there when you need them for the down payment.

4. Avoid Over-Contributing

- Be mindful of your TFSA contribution room. If you over-contribute, the Canada Revenue Agency (CRA) imposes a 1% penalty per month on the excess amount. Check your available TFSA contribution room before adding any new funds.

5. Combining TFSA with Other Programs

You can combine your TFSA withdrawal with other programs to maximize the funds available for your home purchase:

- Home Buyers’ Plan (HBP): You can use the HBP to withdraw up to $35,000 from your RRSP (per individual) for a down payment. While the RRSP withdrawal is tax-free under the HBP, you will need to repay the amount into your RRSP over 15 years. By using both the TFSA and HBP, you could increase the total amount available for your down payment.

- First Home Savings Account (FHSA): The FHSA, introduced in 2023, allows Canadians to contribute up to $8,000 per year (up to a maximum of $40,000) for a tax-deductible contribution similar to an RRSP, with tax-free withdrawals like a TFSA. If you have both an FHSA and TFSA, you can use both for your down payment.

6. Strategic Investment Growth

- Long-Term Growth for a Larger Down Payment: If you’re not in a rush to purchase a home and have a few years to save, consider investing your TFSA funds in a diversified portfolio with a mix of equities and fixed income. This can help grow your down payment faster due to the tax-free capital gains and interest earnings in the TFSA.

Example:

Let’s say you have $50,000 in your TFSA that has been invested in a mix of mutual funds and bonds for several years. You decide to use this for your down payment.

- You log into your TFSA account and liquidate the investments, converting them to cash.

- You withdraw the $50,000 from your TFSA without any taxes or penalties.

- In the next calendar year, your TFSA contribution room increases by $50,000, allowing you to re-contribute the funds at a later date.

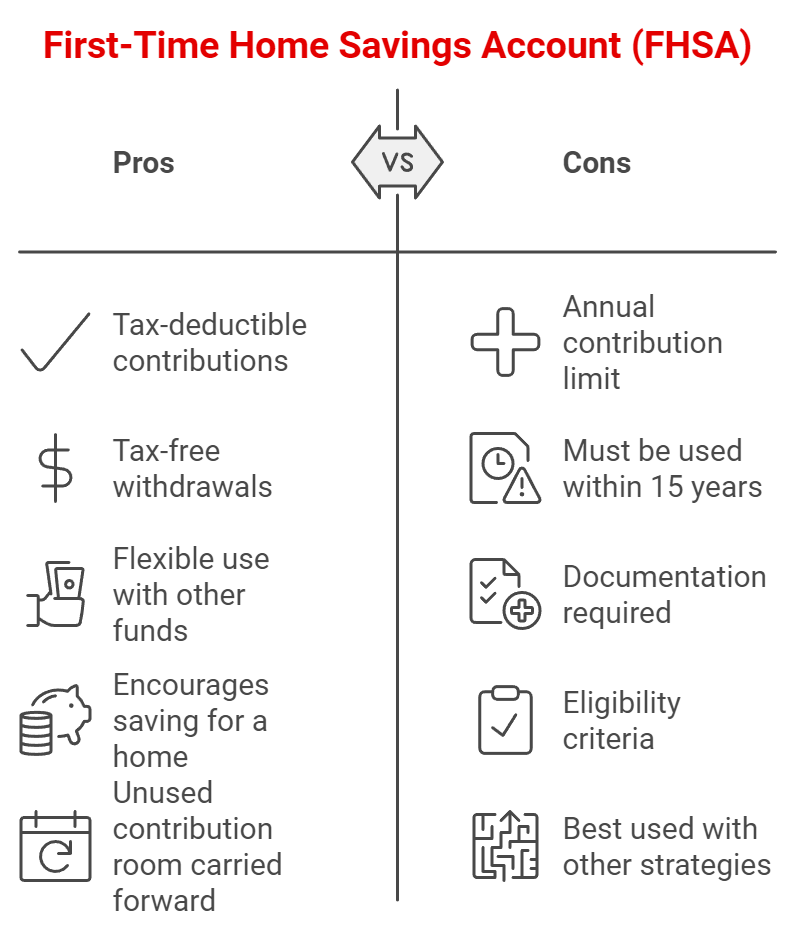

FHSA (First Home Savings Account)

The First-Time Home Savings Account (FHSA) enables first-time home buyers to save for the down payment for their first home. The FHSA is a relatively new savings account designed specifically to help Canadians save for their first home, combining features of both a Registered Retirement Savings Plan (RRSP) and a Tax-Free Savings Account (TFSA).

Tax-Free Contributions

Contributions to an FHSA are tax-deductible, similar to an RRSP. This means you can reduce your taxable income by the amount you contribute, up to the annual and lifetime contribution limits.

Withdrawals from an FHSA for the purpose of buying a qualifying first home are tax-free, similar to a TFSA. This makes it an excellent tool for saving for a down payment.

Contribution Limits

As of the current rules, individuals can contribute up to $8,000 per year, with a lifetime maximum contribution limit of $40,000. Unused contribution room can be carried forward to future years, but annual contributions cannot exceed $8,000.

Using FHSA Funds for a Down Payment:

To use the FHSA funds for a down payment, you must meet the eligibility criteria for first-time homebuyers, which generally means you (and your spouse or common-law partner) must not have owned a home that you lived in as your principal residence at any time during the current calendar year or in the preceding four calendar years.

When you are ready to buy your first home, you can withdraw the funds from the FHSA tax-free. The withdrawal process is straightforward, but you must ensure the funds are used to purchase a qualifying home within 15 years of opening the account, or the FHSA must be closed.

You can combine FHSA funds with other sources of down payment, such as savings, RRSP withdrawals under the Home Buyers’ Plan (HBP), or gifted funds. This flexibility allows you to maximize your down payment.

Documentation

You’ll need to provide bank statements or other documentation showing the funds have been withdrawn from the FHSA and deposited into your account for the purpose of the down payment.

You may also need to provide documentation from the FHSA provider confirming the withdrawal was made for the purchase of a qualifying home.

Advantages & Considerations

The tax advantages of the FHSA make it a highly efficient way to save for a down payment, potentially allowing you to save more quickly than with other savings methods.

The FHSA offers the flexibility of tax-free withdrawals when buying your first home, which can be a significant financial boost.

While the FHSA provides significant tax benefits, the contribution limits mean it’s most effective when used in combination with other savings strategies if you need a larger down payment.

The FHSA must be used within 15 years of opening, so it’s best suited for those who are planning to buy their first home within that period.

In summary, the First Home Savings Account (FHSA) is an excellent source of down payment for first-time homebuyers in Canada, offering both tax-deductible contributions and tax-free withdrawals, making it a highly advantageous savings tool for those planning to enter the housing market.

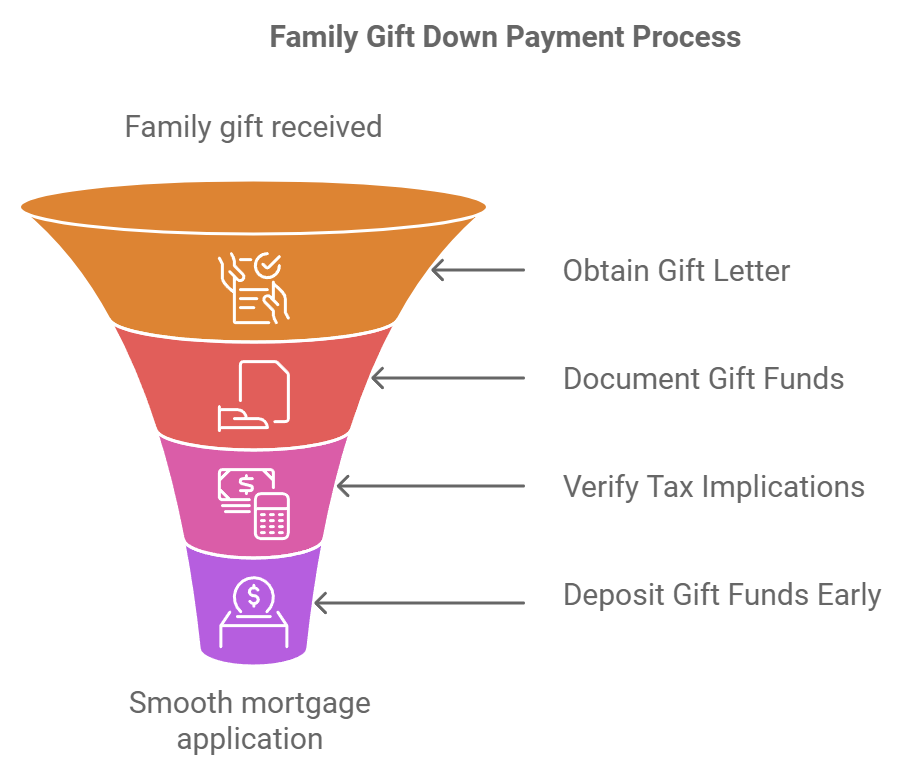

Gift Funds from Family

Many Canadians get help from family for their down payment. Parents, grandparents, and siblings can give money to help buy a home. But, there are rules to follow when using family gifts for a mortgage.

Gift Letter Requirements

Lenders need a signed gift letter for down payment funds. This letter must have:

- The amount of the gift funds being provided

- The relationship between the donor and the recipient

- A statement confirming that the funds are a true gift and not a loan

- The donor’s signature and contact information

The gift letter proves the funds are a gift, not a loan. It’s crucial to have this letter ready and signed to avoid mortgage application problems.

Tax Implications of Gift Funds

In Canada, the person getting the gift doesn’t have to pay taxes on it. This is true as long as the gift is not a loan.

But, the person giving the gift might face tax rules if they give too much. It’s wise for both sides to talk to a tax expert to understand any tax issues.

To make the mortgage process easier, gift funds should be documented and deposited early. This lets the lender check the funds’ source and makes sure the gift is not used to inflate the down payment.

Knowing the rules for using family gifts can help Canadians achieve their dream of owning a home. It makes the mortgage application process smoother and more confident.

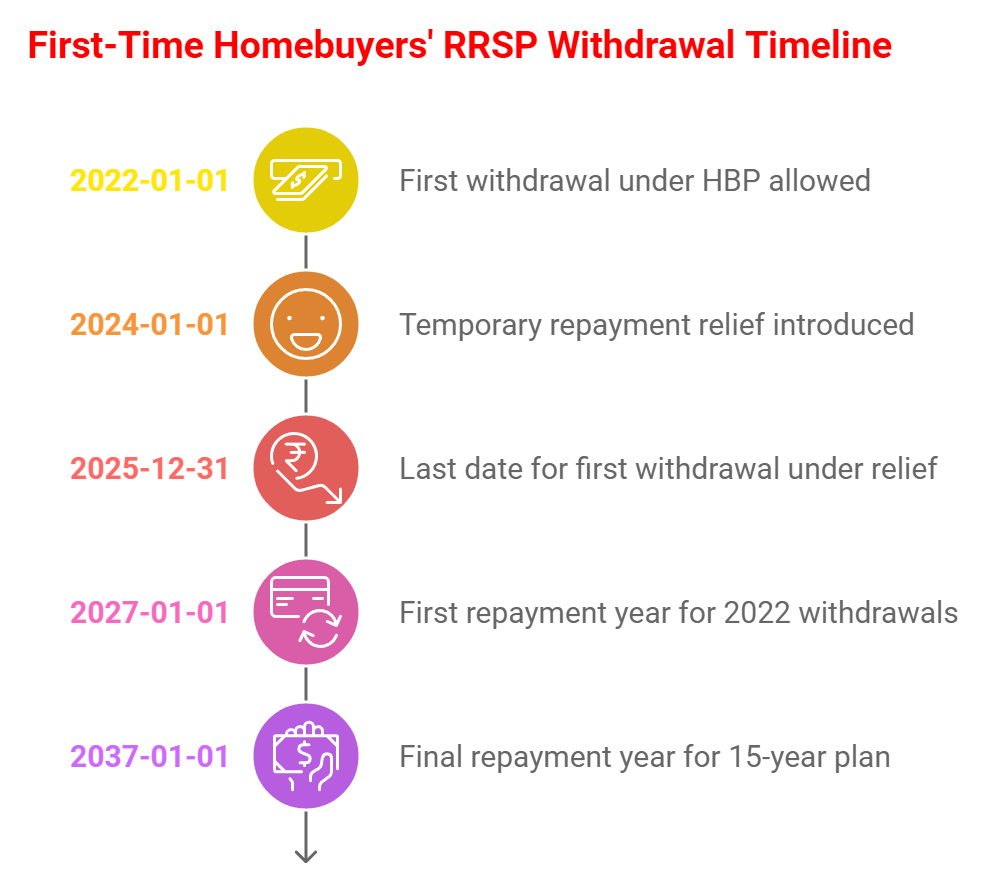

RRSP Home Buyers’ Plan

Canadian first-time homebuyers can get a big help from their retirement accounts. The Home Buyers’ Plan lets them take up to $60,000 from their RRSP for a down payment. This way, they can use their retirement savings without worrying about taxes right away.

RRSP Home Buyers’ Plan

The RRSP Home Buyers’ Plan is a great option for Canadians buying their first home. To use it, you must be a first-time buyer, have a home purchase agreement, and plan to live in the home as your main residence within a year.

With the HBP, you can take out up to $60,000 from your RRSP for a down payment. If you’re buying with a partner, you can both take out $60,000. This can make it easier to afford a home.

Tax Implications and Repayment

The Home Buyers’ Plan has a big plus: the money you take out isn’t taxed as income. But, you must pay it back to your RRSP within 15 years. You start making payments the year after you take out the money.

A temporary repayment relief was introduced in 2024 to defer the start of the 15-year repayment period by an additional three years for participants making a first withdrawal between January 1, 2022, and December 31, 2025. Accordingly, the 15-year repayment period would start the fifth year following the year in which a first withdrawal was made. For example, if you made your first withdrawal in 2022, your first year of repayment will be 2027.

It’s important to know how the HBP works and what taxes you might face. If you don’t pay back the money, it will be taxed as income. So, make sure to plan your repayments and include them in your budget to afford a home.

Exploring retirement account withdrawals, like the RRSP Home Buyers’ Plan, can help first-time homebuyers in Canada. It can give them extra money for their down payment and help them achieve their dream of owning a home.

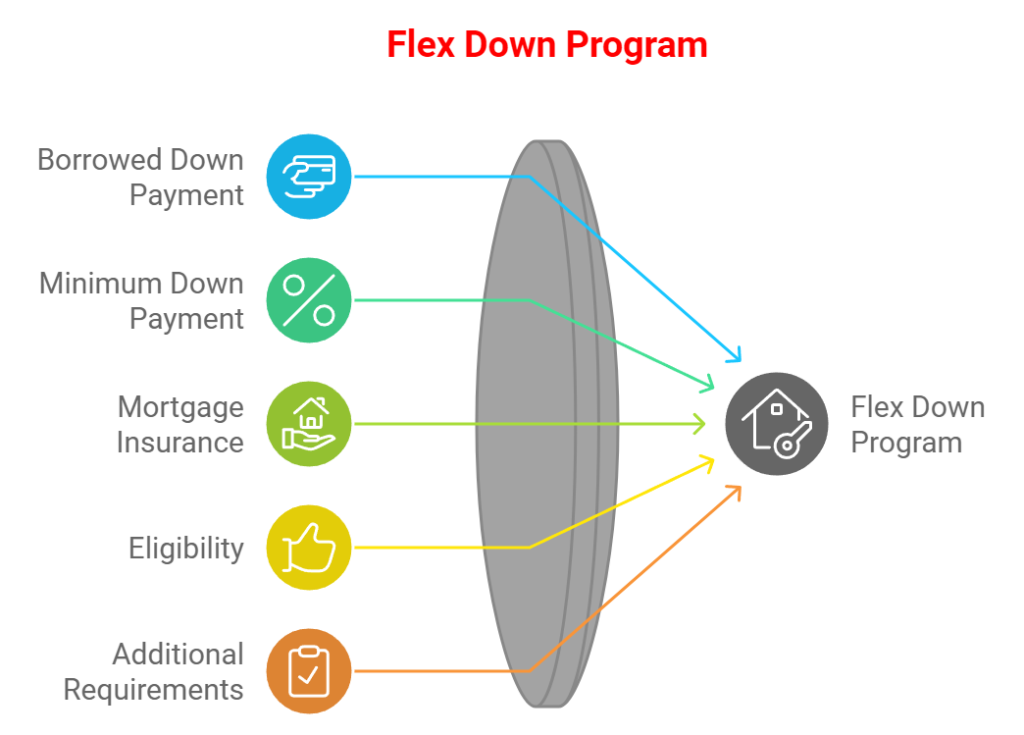

Flex Down Mortgage Program

The Flex Down mortgage program in Canada is a type of high-ratio mortgage that allows homebuyers to use borrowed funds for their down payment. This program is designed to help individuals who have strong credit and can afford monthly mortgage payments but do not have enough savings for the required down payment.

Key Features of Flex Down:

- Borrowed Down Payment: The down payment can be borrowed from various sources, including personal loans, lines of credit, or even credit cards, as long as the borrower qualifies to carry the additional debt alongside the mortgage.

- Minimum Down Payment: The program allows you to borrow the minimum 5% down payment required for homes priced up to $500,000. For homes between $500,000 and $999,999, a down payment of 5% is required on the first $500,000 and 10% on the portion exceeding $500,000.

- Mortgage Insurance: Since this is a high-ratio mortgage (less than 20% down), the borrower must also pay for mortgage default insurance provided by organizations like CMHC, Sagen, or Canada Guaranty.

- Eligibility: Borrowers typically need a strong credit history and stable income to qualify for the Flex Down program, as lenders need to ensure that the borrower can handle both the mortgage payments and the repayment of the borrowed down payment.

- Additional Requirements: Some lenders may require a minimum credit score (often around 680 or higher) and proof that the borrower can afford the additional debt obligations.

Considerations:

Since the down payment is borrowed, the overall debt load increases, and lenders will factor this into your debt service ratios (Gross Debt Service (GDS) and Total Debt Service (TDS)) when assessing your mortgage application.

Depending on how the down payment is borrowed (e.g., credit cards or personal loans), interest rates on the borrowed funds could be high, adding to the overall cost of purchasing a home.

The Flex Down program can be a good option for buyers who are financially stable but don’t have liquid savings for a down payment, though it comes with the responsibility of managing additional debt.

For more information, it’s important to speak with a mortgage professional to assess whether the Flex Down option is suitable for your financial situation.

Sale of Assets

Looking to raise funds for a down payment? Selling existing assets is a good option. You can sell investments, vehicles, or personal property to get the money you need. This includes stocks, bonds, cars, boats, or collectables.

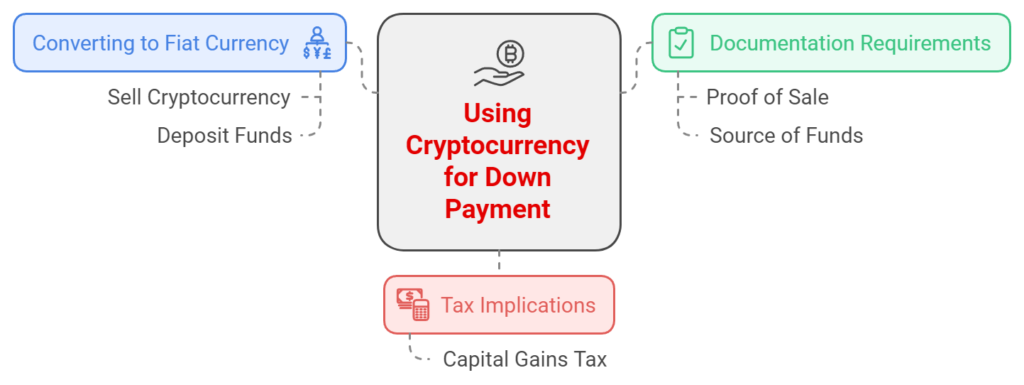

Bitcoin and other digital currencies

Digital currencies as a direct source of down payment for a mortgage are generally not accepted by most traditional lenders. However, there are ways to utilize digital currency indirectly as a down payment source by first converting it into fiat currency (e.g., Canadian dollars). Here’s how it works:

Direct Use of Digital Currency:

- Not Directly Accepted: Most lenders in Canada do not accept Bitcoin or other cryptocurrencies directly as a down payment. This is primarily due to the volatility of digital currencies, the difficulty in tracing the origin of funds, and regulatory concerns.

Indirect Use of Digital Currency:

- Converting to Fiat Currency:

- Sell the Cryptocurrency: To use cryptocurrency for a down payment, you must first sell the digital assets through a cryptocurrency exchange or other legal means and convert them into Canadian dollars.

- Deposit the Funds: Once converted, you must deposit the proceeds into a traditional bank account. Lenders typically require these funds to be in your account for a certain period (often 30 to 90 days) to be considered a legitimate source of down payment.

- Documentation Requirements:

- Proof of Sale: You must provide documentation of the sale of the cryptocurrency, including the transaction history from the exchange, proof of the funds being deposited into your bank account, and any relevant tax documentation.

- Source of Funds: Lenders will need to verify the source of funds, ensuring that the money used for the down payment is legitimate and not associated with illegal activities. This may include tracing the origin of the cryptocurrency and ensuring it complies with anti-money laundering (AML) regulations.

- Tax Implications:

- Capital Gains Tax: Selling cryptocurrency may trigger capital gains tax, which needs to be considered when determining the net amount available for the down payment. Ensure you have accounted for any tax liabilities when planning to use cryptocurrency proceeds.

Considerations:

- Volatility: The value of cryptocurrencies can be highly volatile, which poses a risk when planning to use them for a down payment. The value could decrease significantly between the time of planning and actual conversion.

- Regulatory Scrutiny: Lenders may subject transactions involving cryptocurrency to higher scrutiny due to concerns about money laundering and the traceability of funds.

While Bitcoin or other digital currencies cannot be directly used as a down payment for a mortgage in Canada, they can be utilized indirectly by converting them into Canadian dollars and ensuring that the converted funds are well-documented and meet the lender’s requirements. Before proceeding, it’s essential to consult with both a financial advisor and Allen Ehlert to understand the specific requirements and implications.

Grants and Down Payment Assistance Programs

For many, saving for a down payment is tough, especially for first-time buyers. Luckily, there are government grants and down payment help programs. These can make buying a home easier by covering some costs upfront.

Provincial and Municipal Grants

Provinces and cities also have their own help. For example, British Columbia’s Home Buyers’ Plan lets first-time buyers use RRSPs for down payments. Ontario’s First-Time Homebuyer Incentive gives a land transfer tax rebate to help with costs.

“Down payment assistance programs can be a game-changer for first-time buyers struggling to save for a home. By leveraging these grants and incentives, many Canadians are able to achieve their homeownership goals sooner than they thought possible.” – Sarah Thompson, Financial Advisor

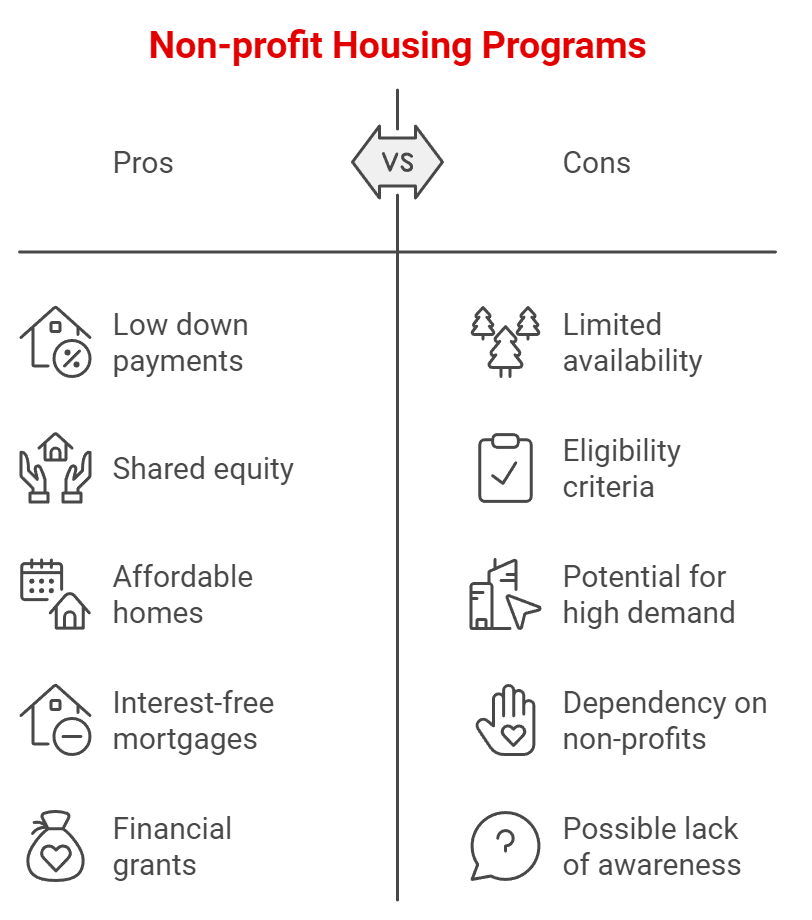

Non-Profit Organizations

Non-profits across Canada also offer down payment help and affordable homes. They work with local governments and developers to solve housing affordability. For example, Attainable Homes in Calgary helps moderate-income earners with low down payments. Options for Homes in Toronto has a shared equity program to lower homeownership costs.

| Organization | Location | Program Details |

|---|---|---|

| Attainable Homes | Calgary, AB | Helps moderate-income earners purchase homes with a minimal down payment |

| Options for Homes | Toronto, ON | Provides a shared equity program that reduces the cost of homeownership |

| Habitat for Humanity | Various locations across Canada | Offers affordable homeownership opportunities through sweat equity and interest-free mortgages |

First-time home buyers can greatly reduce financial barriers with these programs. By using grants, down payment help, and non-profit initiatives, buying a home becomes more achievable. With smart budgeting and saving, owning a home can become a reality for many Canadians.

Employer-Sponsored Programs

Some Canadian employers help with down payments as part of their benefits. They know how important owning a home is for their workers. This support can help employees save for a down payment.

While these programs exist, they are not commonly offered by employers and are more likely to be found in industries or organizations that prioritize employee retention and benefits, such as large tech companies or public sector jobs.

Employer Contributions

Employers help in different ways, like grants or loans. These can be used for a down payment. Here are some common ways:

- Grants: Employers give one-time grants to help with down payments.

- Forgivable loans: Some employers offer loans that are forgiven over time, turning into grants.

- Matched savings plans: Employers match what employees save for a down payment, speeding up savings.

Employer-Assisted Housing Initiatives

Employers do more than just give money. They also offer housing help. This includes:

- Partnerships with local housing organizations: Employers work with non-profits to offer extra resources like workshops.

- Financial education resources: Companies teach employees about buying a home, budgeting, and credit.

- Homebuyer counseling services: Some employers give access to professional advice on buying a home.

The table below compares the benefits of employer contributions and housing initiatives:

| Employer Contributions | Employer-Assisted Housing Initiatives |

|---|---|

| Direct financial assistance for down payments | Educational resources and support for homebuying process |

| Helps employees accumulate funds faster | Provides access to professional advice and guidance |

| Can be in the form of grants, forgivable loans, or matched savings | Offers partnerships with housing organizations and counselling services |

To see if your employer offers down payment help, talk to HR. These programs can make buying a home easier for employees.

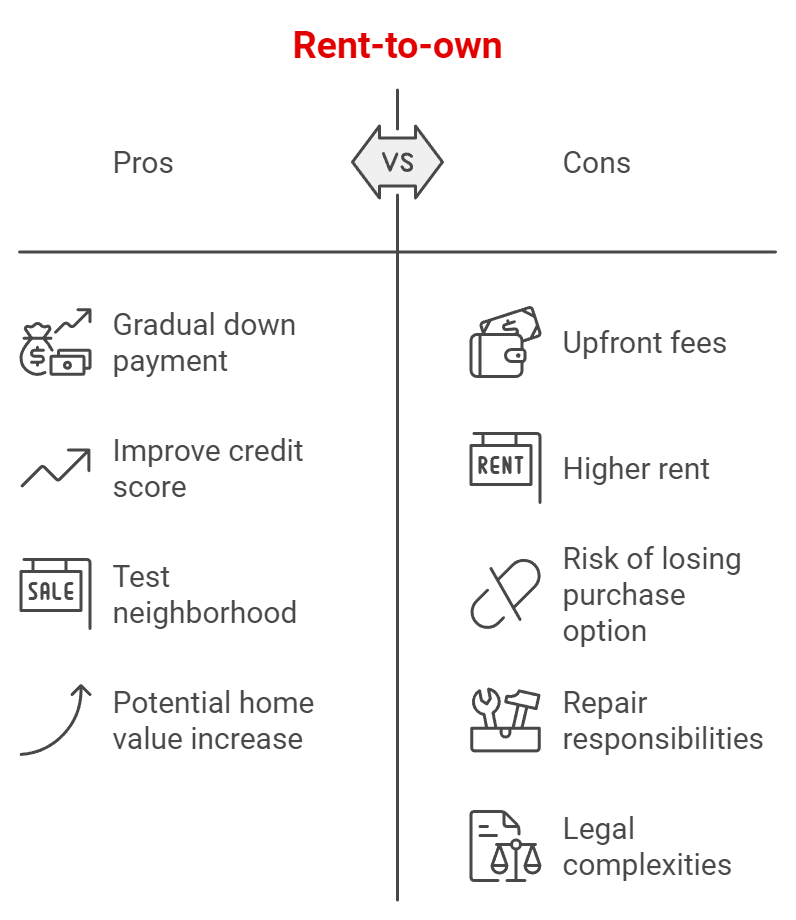

Rent-to-Own Agreements

For those who can’t afford a down payment right away, rent-to-own agreements are a good option. These agreements let renters put a part of their rent towards a down payment. This way, they can work towards owning a home.

How Rent-to-Own Works

With a rent-to-own deal, you sign a lease for one to three years. You have the chance to buy the home at a set price later. A part of your rent goes towards the down payment, building your equity.

These deals usually have two parts:

- A lease that outlines the rental terms

- An option to buy, giving you the right to purchase the home later

Advantages and Disadvantages

Rent-to-own is great for saving for a down payment or improving your credit score. It lets you test a neighborhood before buying. Plus, you might benefit from the home’s value going up during the lease.

But, there are downsides:

- Upfront fees that you can’t get back

- Rent might be higher than usual

- There’s a chance you could lose your option to buy

- You might have to handle repairs and maintenance

It’s important to read the contract carefully and talk to a lawyer before signing a rent-to-own agreement. This way, you know you’re protected.

Rent-to-own can be a good way to own a home for some. But, it’s key to think about the pros and cons and understand the agreement well before you decide.

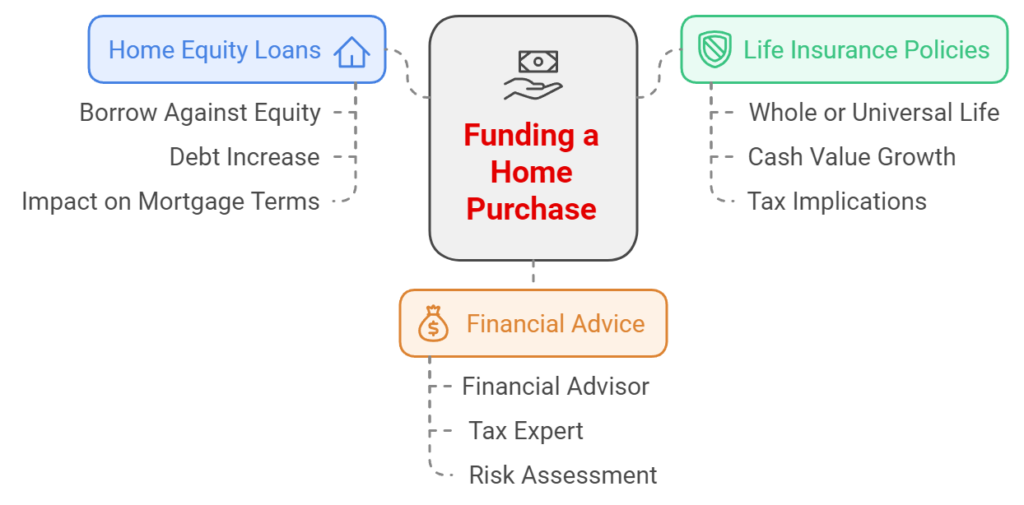

Borrowing Against Other Assets

Some people use savings, gifts, or down payment help to buy a home. Others look at borrowing against what they own. This can help get the money needed for a new home. But, it’s important to think it over and talk to financial experts first.

Home Equity Loans

Homeowners with a lot of equity in their current home might use a home equity loan. This lets them borrow against what they’ve built up. It’s a way to get money without selling other things or using all their savings. Yet, it adds to their debt and might affect their new mortgage terms.

Life Insurance Policies

Life insurance policies, like whole or universal life, can also be used for down payments. These policies grow a cash value that can be borrowed. But, it’s key to know how it will change the policy’s value and death benefit. Also, there could be taxes to think about.

It’s wise to talk to a financial advisor or tax expert before borrowing against assets for a down payment. They can look at your finances, explain the risks and benefits, and make sure it fits your long-term plans.

Net Worth Program

A Net Worth Program in Canada is a mortgage product designed for high-net-worth individuals who may not have a regular or high income but possess significant assets. This program allows them to qualify for a mortgage based on their overall net worth rather than relying solely on their income to meet traditional mortgage lending criteria.

Key characteristics of the Net Worth Program include:

- Asset-Based Qualification: Lenders focus on the borrower’s total assets, such as investments, savings, real estate, and other liquid assets, to determine eligibility. This is particularly helpful for self-employed individuals, retirees, or others with irregular income streams but substantial financial holdings.

- Eligibility: Borrowers may need to show a minimum net worth (e.g., $1 million in assets) to be considered for this program. Lenders typically evaluate liquid assets that can easily be converted to cash.

- Documentation: Instead of emphasizing income, applicants must provide detailed documentation of their assets, including bank statements, investment portfolios, and other proof of ownership.

- LTV (Loan-to-Value) Ratios: Loan-to-value ratios may be more flexible in this program. Lenders may allow higher LTVs for borrowers with a strong asset base.

- Interest Rates: Interest rates in Net Worth Programs may be slightly higher than traditional mortgage rates, depending on the lender’s risk assessment.

- Target Audience: This program is aimed at individuals like investors, business owners, retirees, or those with high-value real estate holdings who may not fit the traditional income-driven lending model but have the financial capacity to support a mortgage.

It’s a solution that accommodates borrowers who, while lacking regular income, demonstrate financial strength through their accumulated wealth. Different lenders may have unique policies and criteria for these programs.

Also Read: Gifts Ineligible for Net Worth Programs

Bank of Mom and Dad

Many homebuyers, particularly first-time buyers, seek help from their parents or family members to fund their down payments. This trend has increased in recent years due to the rising cost of real estate in major cities like Toronto and Vancouver. Here’s an overview of the statistics and trends related to parental help with down payments:

How Many Canadians Receive Parental Help for a Down Payment?

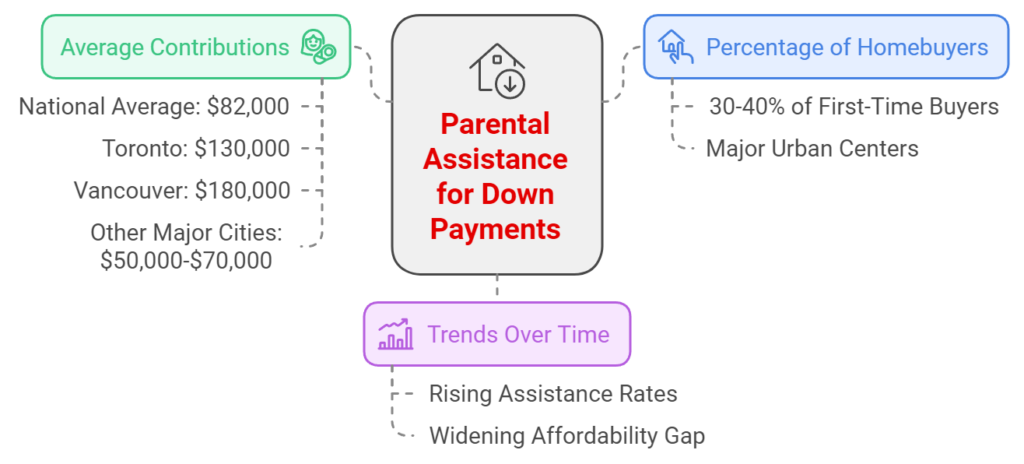

- According to a report by CIBC (2022), around 30-40% of first-time homebuyers receive assistance from their parents for their down payment.

- This trend is particularly common in major urban centers, where housing prices are high, and saving for a down payment can be more challenging for younger buyers.

- The rate of parental assistance has been rising steadily over the past decade, as the affordability gap for first-time buyers continues to widen.

How Much Are Parents Contributing?

- In 2022, the average amount parents contributed to a down payment was approximately $82,000.

- Toronto: Parents contributed an average of $130,000.

- Vancouver: The average contribution was about $180,000.

- Other Major Cities: In cities like Calgary and Ottawa, parental contributions tended to be lower, averaging around $50,000 to $70,000.

- These amounts represent a significant portion of the typical down payment, especially in high-priced markets where down payments of 20% can easily reach six figures.

Who is Receiving the Most Help?

The vast majority of parental assistance is directed at first-time buyers who face the greatest challenges in saving for a down payment, particularly in expensive markets.

The level of parental assistance tends to be higher among families with higher net worth, where parents are more likely to have significant savings or home equity to tap into. Wealthier parents are often in a better position to provide larger down payments, further contributing to the housing affordability divide.

Reasons for the Trend

As real estate prices have surged over the past decade, saving for a traditional 20% down payment has become more difficult for younger buyers, particularly those living in expensive urban markets. This has led to more reliance on family support.

Many parents see helping with a down payment as part of early inheritance planning, especially since the value of their own homes has increased dramatically in recent years.

In the low-interest-rate environment of the past decade, many parents leveraged home equity loans or lines of credit to provide their children with down payment assistance.

With housing prices outpacing wage growth, younger Canadians are struggling to save for down payments, making parental assistance more necessary.

How Do Parents Provide the Help?

- Gifts: Most of the parental assistance comes in the form of gifts. These gifts are typically non-repayable and are often documented with a gift letter, especially if the borrower is applying for a mortgage.

- Loans: In some cases, parents provide a loan to their children to help with the down payment. However, lenders usually consider this a liability for the borrower, which can affect mortgage qualification.

- Co-Signing: In addition to providing funds, some parents choose to co-sign on the mortgage, especially when their children are unable to meet traditional income or credit requirements.

Impact on the Housing Market

Parental assistance is contributing to increased competition in the housing market, especially for first-time buyers. With more financial backing, first-time buyers are able to place larger down payments and compete for higher-priced homes.

Parental help, while beneficial for those who receive it, has created inequities in the housing market. Buyers without access to family wealth often struggle to enter the market, which further drives the affordability gap. Real estate today is a function of wealth, not income.

Future Trends

The trend of parents helping with down payments is expected to continue in the coming years, especially as housing prices remain high, and as more parents seek to pass wealth to their children during their lifetime. However, as interest rates rise, leveraging home equity for down payments may become more costly for parents, potentially moderating the level of assistance they can provide.

Summary of Key Figures:

- Percentage of first-time homebuyers receiving help: 30-40%.

- Average parental contribution (Canada-wide): $82,000.

- Toronto parental contribution: $130,000.

- Vancouver parental contribution: $180,000.

Shared Equity Program

Due to the difficulty of building up a large enough down payment to purchase a house, many purchasers have sought the assistance of an equity partner. An equity partner is an organization that provides money to help purchase a home for a percentage of the home ownership. For example, if buyers wanted to purchase a $800,00 house, 20% down would be required, or $160,000. An equity partner could provide $80,000 for a 10% stake in the value of the house in a type of tenants in common ownership situation.

Equity provided by programs like Ourboro can be used as a source of down payment for a mortgage in Canada. Ourboro is an example of a shared equity program, where a third party provides a portion of the down payment in exchange for a stake in the property’s future value. This type of program can help buyers who may not have sufficient savings for a down payment but can otherwise afford the monthly mortgage payments.

How Shared Equity Programs Work:

- Ourboro’s Model: In the Ourboro program, the company partners with homebuyers by contributing to their down payment. In return, Ourboro receives a share of the equity in the property, proportional to the amount they contribute. When the property is sold, Ourboro receives its share of the appreciation (or depreciation) in the home’s value.

- Down Payment Contribution: The amount contributed by Ourboro can be combined with the homebuyer’s personal savings to meet the required down payment amount, which is typically 5% or more of the home’s purchase price for a mortgage in Canada.

Considerations for Using Shared Equity Programs:

- Lender Acceptance: Not all lenders accept down payments from shared equity programs like Ourboro. It’s essential to work with a lender familiar with and willing to accept this type of arrangement.

- Ownership and Equity Sharing: When using a shared equity program, you are sharing ownership of the property’s equity with the third party. This means you will share the appreciation (and possibly depreciation) in the home’s value when you sell the property.

- Legal and Financial Implications: It’s important to fully understand the terms of the agreement, including how the equity is shared and what happens in the event of a sale or refinancing. Legal advice is recommended to ensure you are clear on all obligations and potential future scenarios.

- Documentation Requirements: Lenders will typically require documentation from the shared equity provider detailing the terms of the contribution. This includes the amount being provided, the conditions of the equity share, and how it affects your overall financial standing.

Benefits:

- Increased Purchasing Power: By supplementing your down payment with funds from a shared equity program, you may be able to afford a more expensive home than you could with your savings alone.

- Access to Homeownership: These programs can make homeownership accessible to individuals who have steady income but lack the required down payment.

Drawbacks:

- Equity Sharing: You are giving up a portion of your future equity in the home, which could be significant if the property appreciates in value.

- Complexity: The arrangements can be more complex than traditional down payments, requiring careful consideration of the long-term financial implications.

Equity provided by Ourboro or similar shared equity programs can be a viable source of down payment for a mortgage in Canada, provided the lender accepts it and you fully understand the terms of the equity-sharing arrangement. It’s advisable to consult with a mortgage broker and a real estate lawyer to navigate this option effectively.

Equity (Down Payment) from Another Property

In Canada, tapping into home equity to purchase another property is a relatively common strategy, particularly in real estate investing. This approach is often used by homeowners who have seen their property values rise significantly over time, enabling them to leverage that equity for various purposes, including buying an investment property or a second home.

Read More: John and Mary Canuck: Example Refinance Strategy

Here are some key points on how this practice is used:

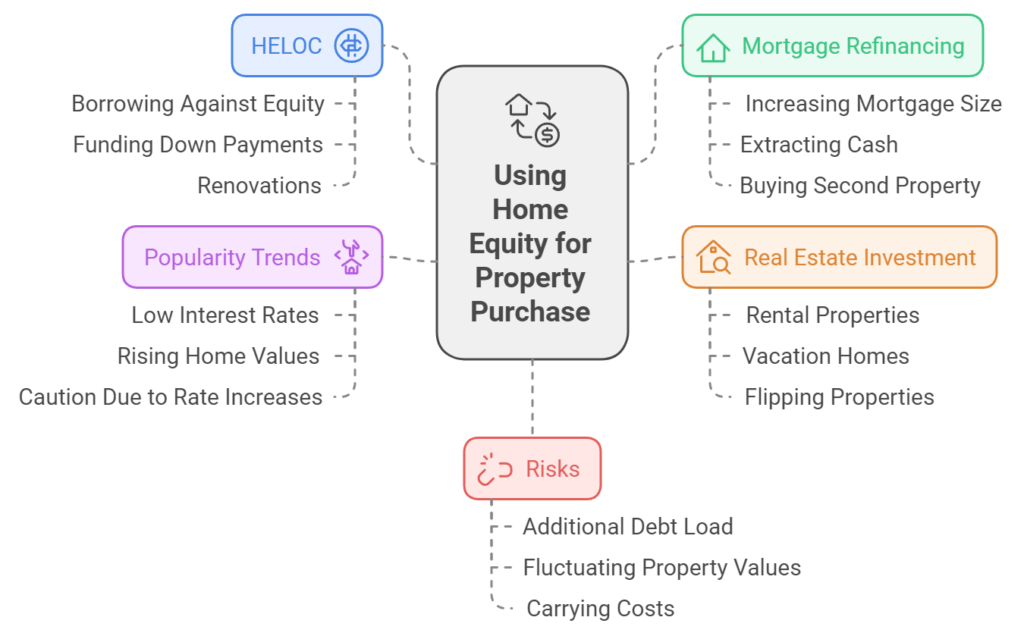

Home Equity Line of Credit (HELOC): A HELOC allows homeowners to borrow against the equity in their homes. It is a popular option for those looking to fund a down payment or renovations on a new property. As of 2023, HELOCs remain one of the most flexible options for tapping into equity, and a significant number of Canadian homeowners use this for investment property purchases.

Mortgage Refinancing: Some homeowners refinance their existing mortgage to access the built-up equity. This involves increasing the size of their mortgage, using the additional funds to purchase a second property. With the recent increases in property prices in many Canadian markets, refinancing has become a practical option for homeowners to extract cash from their homes.

Real Estate Investment: Many Canadians use equity from their primary residence to invest in real estate, whether in rental properties, vacation homes, or even flipping properties. Real estate is seen as a stable long-term investment in Canada, particularly in hot markets like Toronto, Vancouver, and other major cities.

Rising Popularity in Recent Years: The trend has grown in popularity due to low interest rates over the last decade and rising home values, though the increase in interest rates in 2022 and 2023 has made some homeowners more cautious. However, for those with significant equity, it’s still considered a viable option to expand their property portfolios.

Risks: While taking out equity can be a good investment strategy, it comes with risks, especially in a market with rising interest rates. Borrowers need to consider the additional debt load, fluctuating property values, and the carrying costs of owning multiple properties.

In summary, using home equity to purchase another property is quite popular in Canada, particularly among real estate investors and those in larger markets. It is seen as a way to build wealth through property ownership, but it requires careful financial planning to manage risks associated with market fluctuations and debt.

FAQ

What is a down payment, and why is it important when purchasing a home?

A down payment is a big upfront cash payment when buying a home. It’s usually 5% to 20% of the home’s price in Canada. It shows you’re financially stable and helps lower your mortgage amount. It’s a key step in buying a home.

What are some common sources of down payment funds?

Many people use personal savings, gifts from family, or government grants for down payments. You can also withdraw from your RRSP, sell assets, or use crowdfunding. Rent-to-own agreements and borrowing against other assets are other options.

How can I save for a down payment using personal savings?

To save for a down payment, start by making a budget. Look for ways to spend less and save more. Open a high-yield savings account to grow your savings faster. Set up automatic transfers to keep saving regularly.

Can I use gift funds from family members for my down payment?

Yes, you can use gifts from immediate family for a down payment. Lenders need a gift letter from the donor. This letter must confirm the gift and the donor’s relationship to you. In Canada, there’s usually no tax on these gifts for the recipient.

What is the Home Buyers’ Plan (HBP), and how can it help with my down payment?

The Home Buyers’ Plan lets first-time homebuyers in Canada use up to $35,000 from their RRSP for a down payment. This money isn’t taxed as income if you repay it within 15 years. You must be a first-time buyer, have a home purchase agreement, and plan to live in the home.

Are there any government grants or assistance programs available for down payments?

Yes, there are government grants and programs for down payments, especially for first-time buyers. The First-Time Home Buyer Incentive offers a shared equity mortgage. Many provinces and cities also have grants or loans for down payments.

Can I use crowdfunding platforms to raise funds for my down payment?

Yes, you can use platforms like DownPaymentDreams.com or Feather the Nest to raise funds. These platforms help you raise money for your down payment. Remember, the funds are considered gifts and must be documented for lenders. Be aware of fees and tax implications.

What is a rent-to-own agreement, and how can it help with a down payment?

A rent-to-own agreement lets renters apply part of their rent to a down payment. It’s a lease option with a chance to buy the home later. While it helps with saving, it can be risky due to upfront fees and the chance of losing the option to buy.

Can I borrow against other assets to fund my down payment?

Yes, you can borrow against assets like home equity or life insurance for a down payment. But, it increases your debt and may affect taxes or mortgage terms. Always talk to a financial advisor before borrowing against assets for a down payment.

How do lenders verify the source of down payment funds during the mortgage application process?

Lenders check the source of down payment funds to ensure they’re real and not borrowed. They look at bank statements, gift letters, or other documents. Proper documentation is key to avoid mortgage approval issues and meet lending rules.