… When Buying or Refinancing a Home

Buying a home (or refinancing one) is exciting — but when you add up land transfer tax, legal fees, and all the little “extras,” it can feel like death by a thousand cuts. One of the most common questions I get as a mortgage agent is: “Allen, how can I save on legal fees?”

The truth is, you can’t always avoid them, but you can be smart about where and how you spend your money. Let’s dive into five practical strategies that will help you keep more cash in your pocket.

Topics I’ll Cover

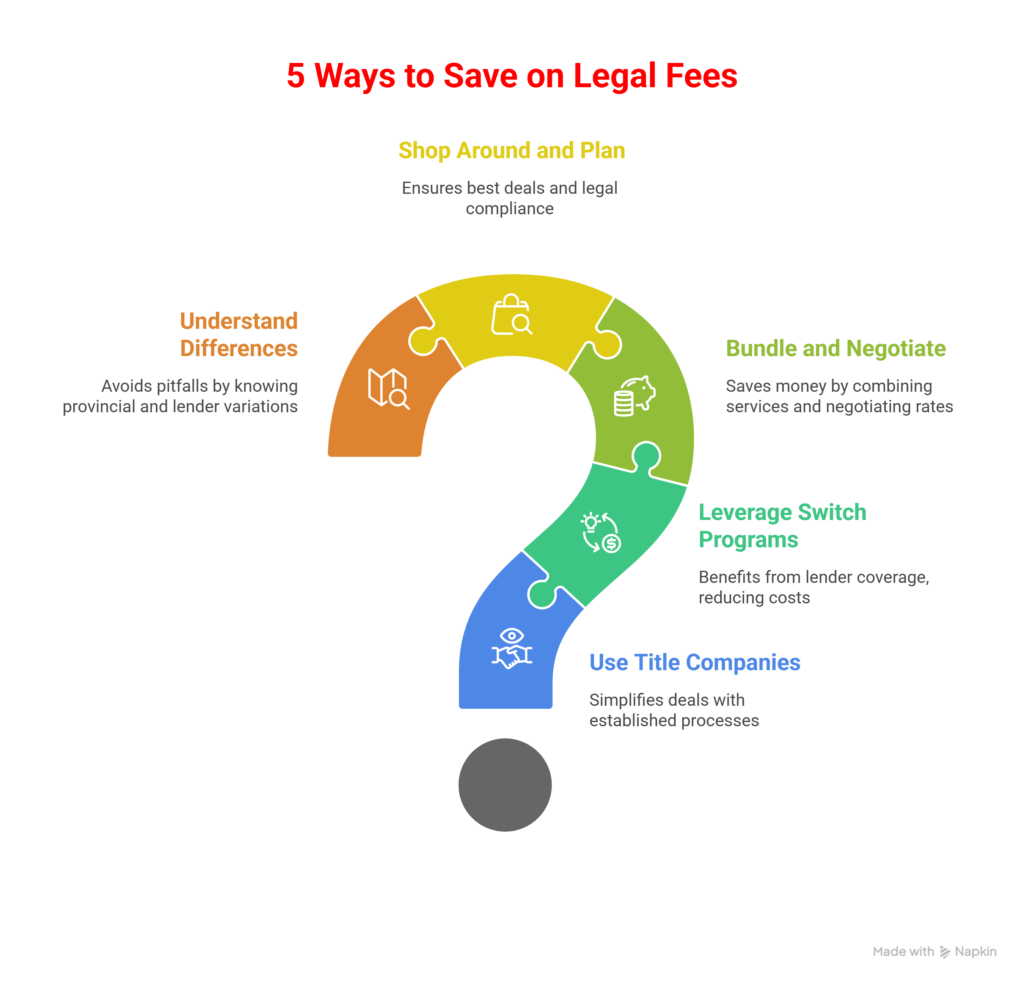

Use Title Companies Like FCT for Simple Deals

Take Advantage of Lender-Covered Switch Programs

Bundle and Negotiate Title Insurance

Shop Around and Plan Ahead with Your Lawyer

Understand Provincial Differences and Lender Types

Use Title Companies Like FCT for Simple Deals

Here’s the scoop: for straightforward mortgage deals, you may not even need a full-service lawyer. Companies like FCT (First Canadian Title), Chicago Title, or Stewart Title can handle:

- Registering your mortgage

- Title insurance

- Disbursements and paperwork

Because it’s streamlined, this route is usually $300 – $800 cheaper than hiring a lawyer.

The trade-off? FCT won’t provide Independent Legal Advice (ILA). So if your deal involves a private mortgage, a matrimonial transfer, or complex terms, you’ll still need a lawyer. But for a clean switch or refinance with an A lender, this is often the fastest, cheapest option.

Take Advantage of Lender-Covered Switch Programs

Here’s a little-known money-saver: some lenders will cover your legal fees when you switch your mortgage to them at renewal. In fact, they may even pay for the appraisal and discharge fee too.

That means you could move your mortgage for a better rate with zero out-of-pocket cost.

Realtors, this is a great tip to share with your clients: “Did you know some lenders will pay your legal costs if you switch to them?” That kind of guidance makes you look like the trusted expert.

Bundle and Negotiate Title Insurance

Title insurance is mandatory with most lenders, but you don’t have to just accept whatever fee shows up on the invoice. Many lawyers or title companies will bundle title insurance with registration fees for a lower total price.

Pro tip: ask upfront if there’s a bundled package. I’ve seen clients save $200–$300 just by asking the right question.

Shop Around and Plan Ahead with Your Lawyer

Not all real estate lawyers charge the same — and fees can vary wildly, even for identical services. Some lawyers charge flat fees, while others bill hourly.

- A flat-fee lawyer is usually more predictable.

- Rushing a deal adds “rush fees” (often $200 – $500). By giving your lawyer 2–3 weeks’ notice, you avoid paying the “last-minute premium.”

I once had a client in Pickering who left their lawyer scramble until the last five days before closing. The rush courier fees alone added $350. A little planning ahead would have saved them that money for paint and furniture.

Understand Provincial Differences and Lender Types

Legal costs also depend on where you live and who your lender is.

- Ontario: You pay legal fees and one of the highest land transfer taxes in Canada (with an extra municipal tax in Toronto).

- Alberta: No land transfer tax — just a smaller land title and mortgage registration fee.

- A lenders (big banks): You only pay your own lawyer or title company.

- B lenders: You also pay the lender’s legal fee ($800 – $1,500).

- Private lenders: You pay two sets of lawyers plus ILA, so legal costs often run $3,500 – $6,000+.

In other words, the more complex the lender type, the more you pay in legal fees.

A Story That Brings It All Together

I once worked with a young couple in Sudbury refinancing to access equity for renovations. They were tight on budget and dreading legal costs. Instead of defaulting to a lawyer, we used FCT, and their closing costs came in about $700 cheaper than expected. That money went straight into their new kitchen backsplash — a much better use of funds!

On the other hand, a client in Windsor needed a private second mortgage to consolidate debt. Despite looking for shortcuts, there weren’t any: two lawyers were mandatory. Their legal bill topped $4,500. The difference? Knowing which path applies to your situation is what makes all the difference.

Allen’s Final Thoughts

Legal fees are part of the cost of doing business in real estate, but that doesn’t mean you shouldn’t look for smart ways to save. From using FCT or other title companies for simple deals, to switching lenders that cover your legal costs, to shopping around for a flat-fee lawyer, the opportunities are there.

As your mortgage agent, I’m not just here to get you the right mortgage — I’m here to make sure the entire process makes financial sense from start to finish. That means:

- Connecting you with cost-effective legal options.

- Helping you understand which costs are unavoidable.

- And making sure you’re never surprised by a bill you didn’t budget for.

Because at the end of the day, the money you save on legal fees is money you can put into your new home, your renovations, or simply your peace of mind.