… The Reverse Mortgage Calculator That Plans for Reality—Not Best-Case Scenarios

If you’ve ever tried a reverse mortgage calculator online, you’ve probably felt that little twinge of doubt after seeing the number pop up. Is that real? Is that optimistic? What’s missing? You’re not wrong to wonder. Most calculators are built to spark curiosity, not to stand up to scrutiny.

That’s why I built my reverse mortgage calculator differently. It’s designed for Canadians who want answers they can actually plan around, not just a headline figure that feels good in the moment and falls apart later.

Let me walk you through why my calculator is a better choice—and how it changes the conversation for homeowners and financial professionals alike.

What I’ll Cover

Most Reverse Mortgage Calculators Are Built to Impress, Not Inform

Conservative Assumptions Aren’t Pessimistic—They’re Professional

Ranges Beat Single Numbers—Every Time

Net Proceeds Matter More Than Gross Loan Amounts

Province Is Used Properly—Not as a Marketing Lever

How professionals and homeowners can use this tool in practice

Most Reverse Mortgage Calculators Are Built to Impress, Not Inform

The reality is that many Canadian reverse mortgage calculators are lender-centric. Their job is to answer one question quickly: “What’s the biggest number we can show without being technically wrong?”

So they:

- Show a single, precise-looking number

- Assume best-case appraisals

- Ignore or gloss over setup costs

- Skip the explanation of how the number was calculated

That’s fine if you’re browsing casually. It’s not fine if you’re making a retirement, downsizing, or estate decision.

My calculator starts from a different premise: If you can’t defend the number later, it doesn’t belong on the screen now.

Conservative Assumptions Aren’t Pessimistic—They’re Professional

Instead of chasing the highest possible outcome, my calculator uses conservative planning assumptions on purpose. That includes:

- Age-based loan-to-value ranges, not best-case LTVs

- Property-type adjustments for condos and rural homes

- Eligible value caps to avoid overstating results

- Realistic setup-cost ranges, not “from $0” fantasy numbers

This is the same mindset I use in client files. If the real outcome comes in better, great. If it comes in worse, you were already prepared.

That’s how you remove stress from the process.

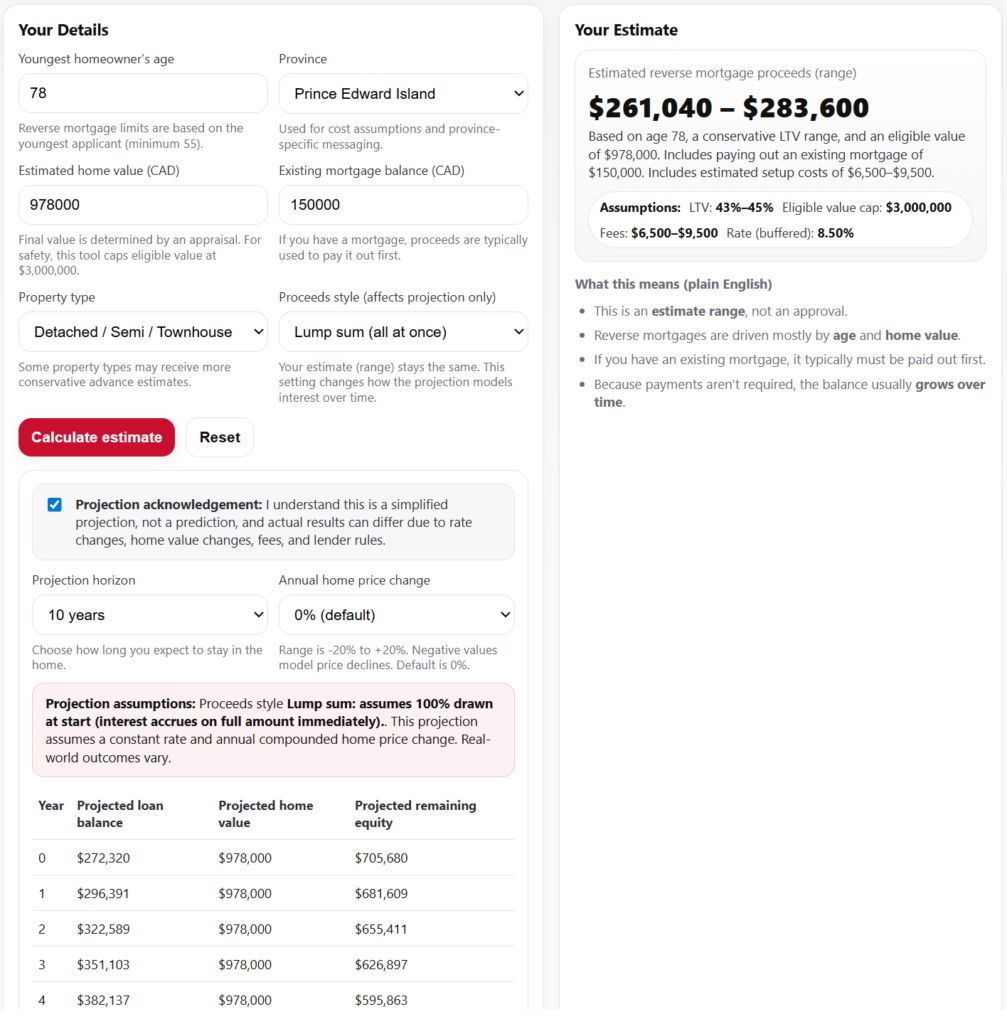

Ranges Beat Single Numbers—Every Time

Most calculators will tell you something like, “You may qualify for $312,456.” It looks precise. It feels authoritative. And it’s usually misleading.

Reverse mortgages depend on appraisals, legal structure, property marketability, and lender nuances. Showing a single number before those steps is guesswork.

My calculator intentionally shows ranges, along with plain-English explanations of what moves the number up or down. That way:

- You understand uncertainty instead of being blindsided by it

- Expectations are set early

- Planning conversations stay grounded

In my experience, ranges build trust faster than false precision ever could.

Net Proceeds Matter More Than Gross Loan Amounts

Here’s one of the biggest differences—and one most people don’t realize until closing day.

Most calculators focus on the gross reverse mortgage amount. My calculator focuses on what you actually receive.

That means accounting for:

- Appraisal fees

- Legal and registration costs

- Title insurance

- Lender setup or administration fees

- Mortgage discharge fees, if applicable

Two homeowners can qualify for the same reverse mortgage and walk away with very different cash amounts. My calculator reflects that reality, so you’re planning with net proceeds—not wishful thinking.

Province Is Used Properly—Not as a Marketing Lever

Some calculators dramatically change the estimate when you toggle provinces. That should raise an eyebrow.

In Canada, the core value of a reverse mortgage is driven by age and home value, not geography. Program rules are largely national, especially among some providers that operate coast to coast.

My calculator uses province the right way:

- To adjust legal and closing cost assumptions

- To flag regional property considerations

- To refine net proceeds—not inflate loan amounts

If province selection massively changes the estimate, something’s off.

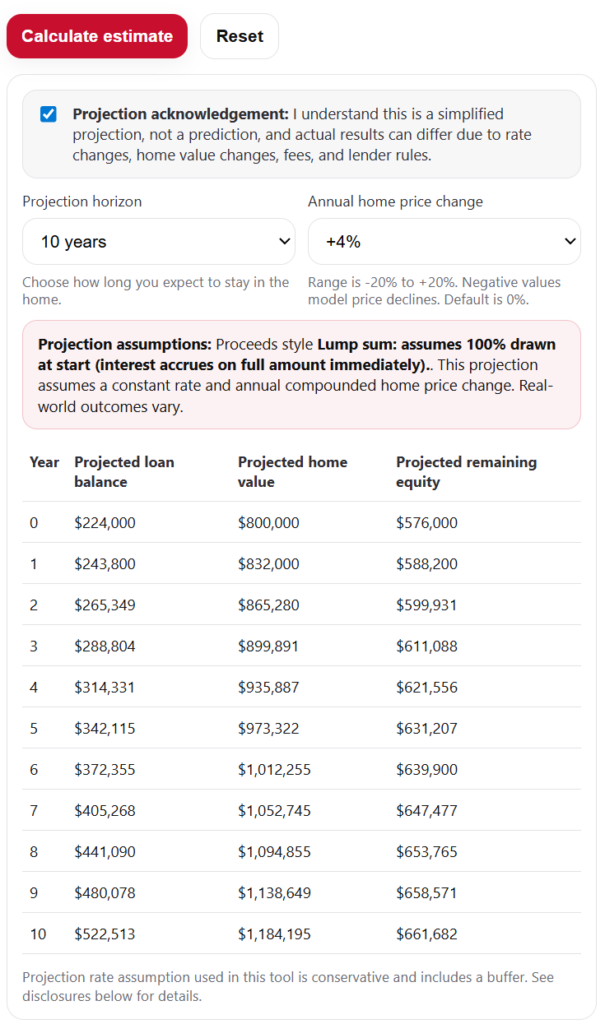

Projections Are Optional—and Clearly Labelled

Some tools avoid projections entirely. Others show long-term numbers without context, which can be dangerous.

My calculator:

- Keeps projections optional

- Requires a clear acknowledgement that they’re illustrative, not predictive

- Uses conservative rate assumptions

- Explains how compounding affects equity over time

That gives users insight without crossing into false certainty.

A Life Example

A homeowner had tried three different online calculators before calling me. One said they’d qualify for $320,000. Another showed $290,000. Mine showed a range of $260,000 to $285,000—lower than the others.

At first, they were disappointed.

Fast forward to closing. After appraisal, legal fees, and paying out an existing mortgage, their net proceeds were just under $270,000.

Suddenly, my calculator wasn’t “conservative.” It was accurate.

That’s the moment clients remember—and the reason they refer others.

How Financial Professionals and Clients Can Put This Into Practice

For homeowners

- Use the calculator to plan cash flow, not chase maximums

- Focus on net proceeds and long-term impact

- Treat ranges as a feature, not a flaw

For financial professionals

- Use the calculator to support retirement, tax, and estate planning

- Avoid awkward conversations caused by inflated expectations

- Anchor discussions in defensible assumptions

This tool fits naturally into planning conversations because it respects complexity instead of hiding it.

Allen’s Final Thoughts

Most reverse mortgage calculators are built to start a conversation. Mine is built to finish it without surprises.

It’s conservative by design, transparent by intent, and focused on real-world outcomes—not marketing headlines. My role as a mortgage agent isn’t to sell you the biggest number. It’s to help you understand what’s realistic, what’s sustainable, and what actually fits into your broader plan.

If you want help interpreting the results, pressure-testing scenarios, or coordinating with your financial planner or advisor, that’s where I come in. I’ll walk you through the assumptions, explain the trade-offs, and make sure you’re making decisions with your eyes wide open.

That’s how good mortgage planning should work—and that’s why this calculator exists in the first place.