… Where you live can matter!

It’s a question I hear all the time: “If I lived in a different province, would my reverse mortgage be bigger?” It’s a fair question—and an important one—because it gets right to the heart of how reverse mortgages actually work in Canada.

The short answer is yes and no. The core value of a reverse mortgage doesn’t really change by province—but the final estimate you see on paper absolutely can. And understanding why is what separates clean planning from costly assumptions.

Let’s break it down in plain English.

What I’ll Cover

The Core Drivers Don’t Change by Province

Legal and Closing Costs Vary by Province

Property Eligibility Is Regional, Not Just Provincial

Appraisal Complexity Can Shift the Numbers

What Doesn’t Change—No Matter Where You Live

How Financial Professionals and Clients Can Put This Into Practice

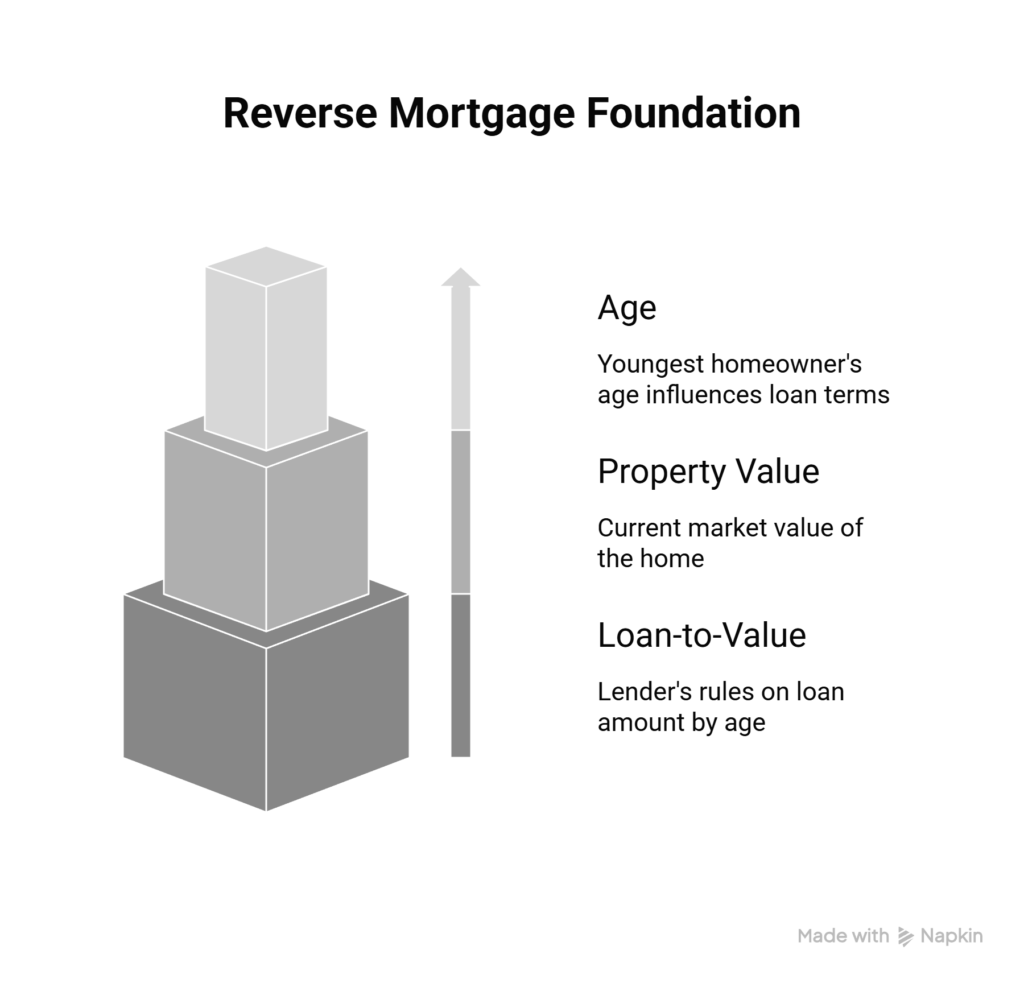

The Core Drivers Don’t Change by Province

At its foundation, a reverse mortgage in Canada is built on three pillars:

- The age of the youngest homeowner

- The current value of the property

- The lender’s maximum loan-to-value rules by age

Those rules are largely national, not provincial.

A 72-year-old homeowner with an $850,000 house in Ontario will generally qualify for roughly the same gross reverse mortgage amount as a 72-year-old homeowner with an $850,000 house in Alberta or Nova Scotia—assuming the properties are comparable.

That’s why reputable calculators don’t suddenly swing the estimate wildly just because you toggle provinces. If they do, that’s usually a red flag.

Where Province Does Influence the Estimate

This is where nuance matters. While province doesn’t change the headline number much, it can absolutely affect the net result—the amount of money you actually walk away with.

Legal and Closing Costs Vary by Province

Legal systems, land registries, and fee structures differ across Canada.

Some provinces tend to have:

- Higher legal fees and land registry costs

- More bundled closing charges

- Different requirements for title searches and registrations

Since reverse mortgage setup costs are often deducted from proceeds, higher provincial costs can reduce the net cash received—even if the gross loan amount is the same.

The mortgage didn’t get smaller. The expenses around it changed.

Property Eligibility Is Regional, Not Just Provincial

Reverse mortgages are sensitive to how easily a property could be sold in the future if needed. That means:

- Urban and suburban homes are treated consistently nationwide

- Rural or remote properties may face more conservative assumptions

- Very small communities can introduce additional scrutiny

This isn’t about provincial rules—it’s about market liquidity. Some provinces simply have more rural housing stock, which can influence estimates in subtle but meaningful ways.

Appraisal Complexity Can Shift the Numbers

In some provinces, appraisals are more straightforward. In others, properties are more likely to include acreage, mixed use, or limited comparable sales.

That can:

- Increase appraisal costs

- Lead to more conservative valuations

- Slightly reduce the comfort level lenders have with the estimate

Again, this affects the estimate, not whether the product exists.

What Doesn’t Change—No Matter Where You Live

It’s just as important to be clear about what doesn’t vary across Canada:

- No income qualification

- No stress test

- No mandatory monthly payments

- The same compounding mechanics

- The same basic product structure offered by providers

There isn’t a province where reverse mortgages suddenly become dramatically better—or worse.

An Example

Two clients were almost carbon copies on paper. Same age. Same approximate home value. One lived in Ontario, the other in a smaller province.

Their gross reverse mortgage estimates were nearly identical. But when we ran the full numbers, the Ontario client’s net proceeds were lower by several thousand dollars—not because the mortgage was worse, but because legal fees, registry costs, and setup expenses were higher.

Neither client was misled. But only one had planned for the difference.

That’s why context matters more than geography.

How Financial Professionals and Clients Can Put This Into Practice

For homeowners

- Focus on net proceeds, not just the headline estimate

- Expect small provincial differences in costs, not massive swings in value

- Plan using conservative ranges instead of best-case assumptions

For financial professionals

- Avoid province-based promises or comparisons

- Model scenarios using national LTV assumptions with local cost overlays

- Help clients understand why estimates differ, not just that they do

Reverse mortgages often sit alongside retirement income planning, downsizing decisions, and estate conversations. Clear expectations keep those discussions productive instead of emotional.

Allen’s Final Thoughts

So—does the value of a reverse mortgage estimate change by province? A little, but not in the way most people think. The mortgage itself is driven by age and home value. Provincial differences show up around the edges: legal costs, appraisals, and net proceeds.

My role as a mortgage agent is to strip away the noise and help you see the full picture. I build conservative estimates, explain where the numbers can move, and make sure you’re planning for reality—not best-case scenarios.

If you’re comparing options, working with a financial professional, or just trying to understand how this fits into your retirement plan, I’m here to walk you through it. Not with hype. Not with shortcuts. Just clear, honest mortgage planning—so you stay in control of the outcome.