… When the Market Moves: How Rising and Falling Home Prices Affect a Reverse Mortgage

Over the last few years, Canadian homeowners have ridden a wild wave. Home prices surged at a pace most people never expected—then, just as quickly, they started pulling back. If you have a reverse mortgage, or you’re considering one, it’s natural to ask: What does this mean for me now—and later?

The short answer is that changing home prices don’t “break” a reverse mortgage, but they absolutely change how it behaves. And that has real implications for cash-flow planning, long-term flexibility, and what ultimately happens to your estate.

Before I get into the weeds, here are the key topics we’ll walk through together:

How rising home prices affect a reverse mortgage

What falling home prices change—and what they don’t

The role of time and compounding when markets shift

Implications for financial planning in retirement

Implications for estate planning and family conversations

How Rising Home Prices Affect a Reverse Mortgage

When home prices are rising, a reverse mortgage often feels very comfortable.

As values climb:

- The gap between your home value and the loan balance tends to widen

- Remaining equity is preserved for longer

- Flexibility increases—downsizing, selling, or transitioning to care becomes easier

In strong markets, homeowners sometimes gain a false sense of security. Rising values can mask the fact that interest is quietly compounding in the background. The math still matters—but appreciation gives you more runway.

This is why many reverse mortgages originated during boom years look “healthy” on paper today.

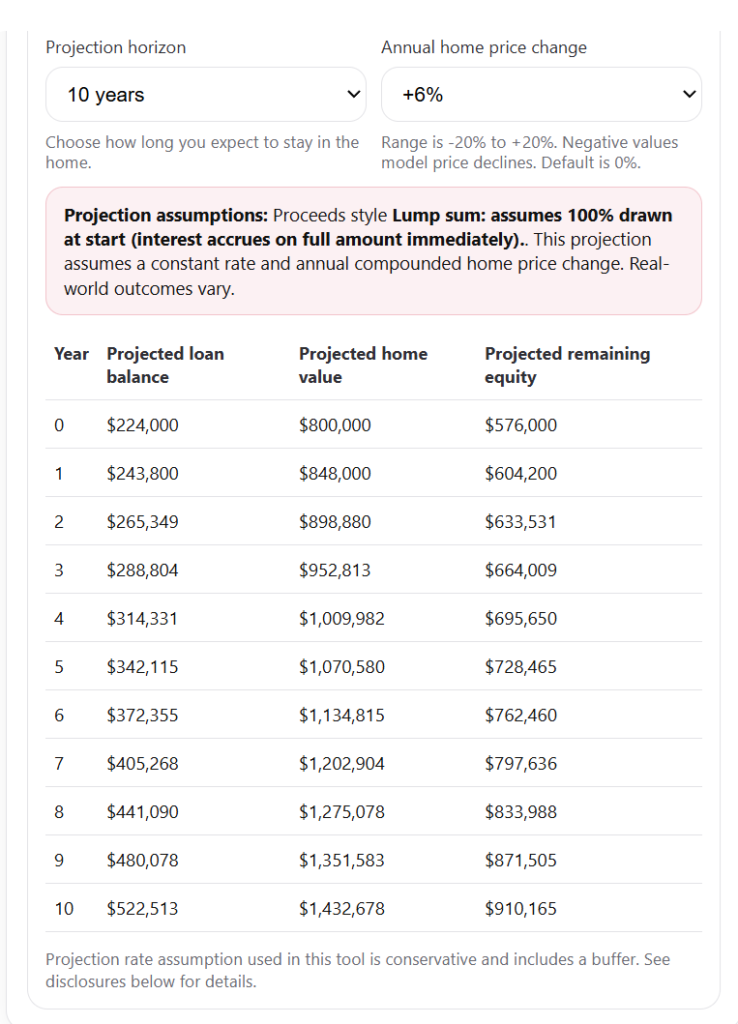

Over the past 10 years, home prices have increased on average of 6 percent. This means if you took out a Reverse Mortgage then on a $800,000, not only would you have $224,000 in your pocket in an original lump sum payment (that would be generating income), but you would also have $910,000 in remaining equity. That’s awesome!!!

What Falling Home Prices Change—and What They Don’t

When prices start to fall, the conversation shifts.

What does change:

- Remaining equity can shrink faster

- Long-term flexibility narrows

- Estate outcomes may look very different than originally expected

What does not change:

- You still own your home

- You are not required to make monthly payments

- You cannot be forced to sell simply because prices drop

- Your downside is capped

In Canada, reverse mortgages are non-recourse. That means neither you nor your estate can ever owe more than the home is worth. If prices fall hard and the loan balance eventually exceeds value, the lender—not your family—absorbs the loss.

That protection is critical, but it doesn’t eliminate trade-offs.

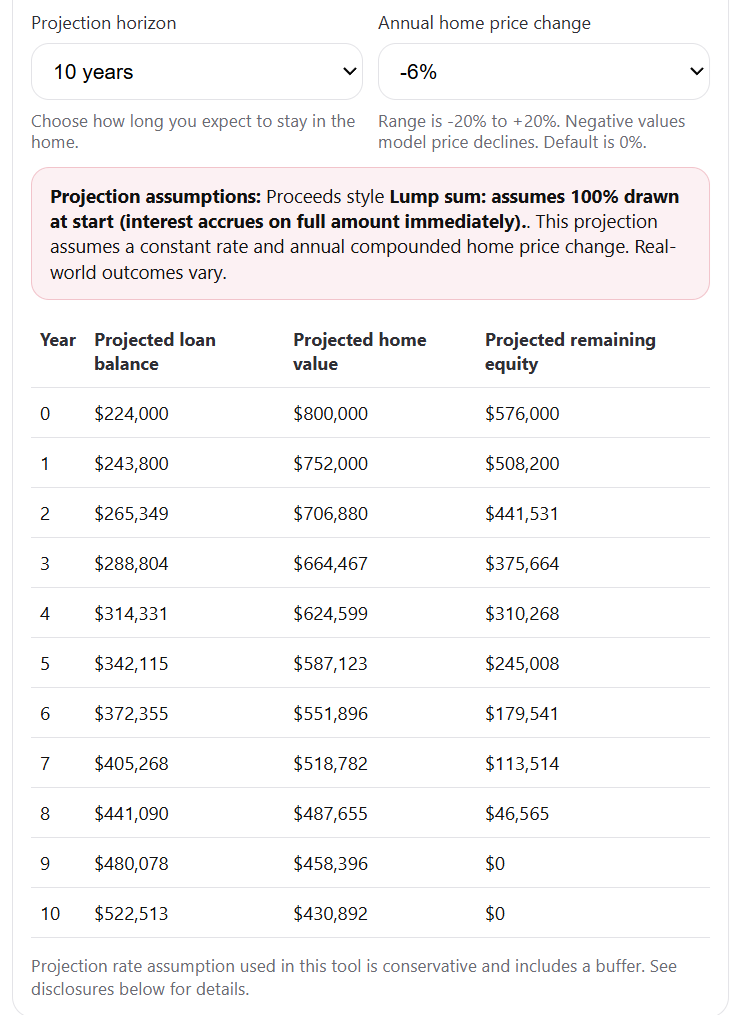

To compare assume over the next 10 years, home prices have decrease on average of 6 percent. This means if you took out a Reverse Mortgage then on a $800,000, not only would you have $224,000 in your pocket in an original lump sum payment (that would be generating income), but no remaining equity in your home.

Time and Compounding Matter More in a Down Market

Reverse mortgages are time-sensitive products. When prices fall while interest continues to compound, two forces are working against equity at the same time.

This doesn’t create risk in the traditional sense—there’s no margin call—but it does accelerate outcomes:

- Equity may be consumed sooner

- Selling earlier versus later can produce dramatically different results

- “Waiting it out” isn’t always neutral

In down markets, how long you stay in the home becomes just as important as how much you borrowed.

What This Means for Financial Planning

From a planning perspective, falling prices raise the bar for intentional use.

A reverse mortgage can still be an effective cash-flow strategy, but it works best when:

- Initial draws are sized conservatively

- Funds are accessed as needed, not all at once

- It’s coordinated with CPP, OAS, pensions, and investment withdrawals

In volatile markets, the reverse mortgage often shifts from being a “nice-to-have” to a buffer—a way to reduce forced investment sales or smooth income during rough patches.

Used thoughtfully, it can protect other assets even when housing markets are under pressure.

Estate Planning: Where Market Changes Really Show Up

Estate planning is where price changes have the biggest emotional impact.

If prices rise:

- More equity may flow to heirs

- Timing becomes more flexible

If prices fall:

- There may be little or no equity left

- Heirs need clarity about options early

Heirs generally have three choices:

- Sell the property and keep any remaining equity

- Repay the loan and retain the home

- Walk away with no further obligation

What matters most isn’t the outcome—it’s expectation management. Families that talk about this early avoid confusion and stress later.

An Example Story

A couple in their early 70s who took a modest reverse mortgage during a strong market. Their plan was simple: stay put, supplement income, and reassess in ten years.

Then prices softened.

Because they’d drawn conservatively, they still had options. They chose to sell earlier than planned, preserved meaningful equity, and downsized on their terms. Had they waited another five years, the outcome would have looked very different.

Same product. Same house. Different timing.

Allen’s Final Thoughts

Changing home prices don’t make reverse mortgages good or bad—they make them revealing. Rising markets hide trade-offs. Falling markets force clarity.

A reverse mortgage can still be a powerful part of a retirement strategy, but it works best when it’s used intentionally, revisited periodically, and integrated into a broader plan that includes cash flow, housing transitions, and estate goals.

That’s where I come in. My role isn’t just to explain how a reverse mortgage works—it’s to help you understand how it fits now, how it might behave if markets change, and what that means for you and your family down the road. Whether you’re a homeowner, a financial professional, or a realtor supporting a client, I’m here to help you think it through before decisions become irreversible.