… The Silent Risk within Your Wall

A Home Equity Line of Credit sounds harmless enough. Flexible. Affordable. Smart. It’s often pitched as “just in case” money—something you set up and forget about until life throws you a curveball.

But here’s the uncomfortable truth: for many homeowners, a HELOC doesn’t just sit quietly in the background. It subtly reshapes behaviour, increases exposure to risk, and—if misused—can turn a strong financial position into a fragile one.

You don’t hear these stories as often. But I see them regularly.

Before we get into the details, here are the exact fault lines where HELOCs most often go wrong:

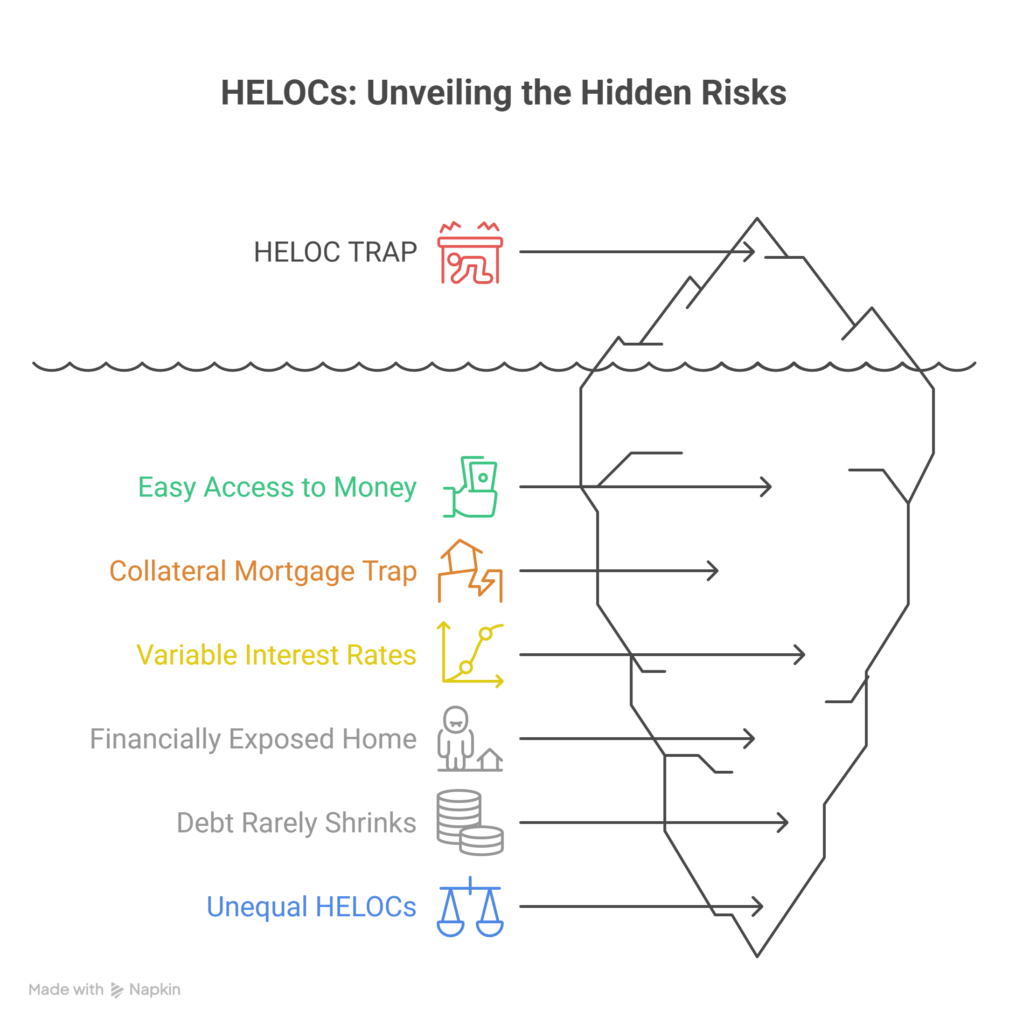

- Easy Access to Money Changes Behaviour

- HELOCs and the Collateral Mortgage Trap

- Variable Interest Rates Can Destabilize Cash Flow

- When Your Home Becomes Financially Exposed

- HELOC Debt Rarely Shrinks on Its Own

- Not All HELOCs Are Created Equal

Let’s walk through each one—plainly, honestly, and without sales spin.

Easy Access to Money Changes Behaviour

This is the risk no one wants to talk about, because it isn’t mathematical—it’s psychological.

A HELOC removes friction. There’s no new application every time you borrow. No awkward pause. No forced moment of reflection. The money is simply there.

At first, it’s sensible:

- “I’ll only use it for emergencies.”

- “It’s cheaper than a credit card.”

- “I’ll pay it back quickly.”

Then real life creeps in.

Renovations run over budget.

Cash-flow gaps last longer than expected.

A lifestyle expense gets justified because “it’s temporary.”

Slowly, the HELOC stops being a safety net and starts becoming a habit. No blow-up. No crisis. Just quiet normalization of debt.

If you’ve ever carried balances longer than planned or relied on credit to smooth everyday life, a HELOC doesn’t fix that behaviour—it amplifies it.

HELOCs and the Collateral Mortgage Trap

One of the most misunderstood—and dangerous—parts of the HELOC conversation is how closely they are tied to collateralized mortgages. In fact, many homeowners don’t even realize they have one.

When a HELOC is set up at most major institutions, it’s often registered as a collateral charge against your home, not just for your mortgage balance, but for much more—sometimes up to 125% of the property value. Many banks make the collateral charge mortgage their default mortgage, and require you to demand a standard charge mortgage (as if you would know to do that) if you didn’t want to be ‘locked in’. That single legal registration then secures multiple products: your mortgage, your HELOC, and potentially any future credit the lender decides to attach.

On paper, this sounds efficient. In real life, it creates a trap.

Because everything is tied together under one collateral charge, moving your mortgage later becomes harder, slower, and more expensive. You can’t simply shop your mortgage at renewal without disentangling the HELOC. Even if another lender offers a better rate, you may be forced to:

- Pay legal fees to discharge and re-register

- Re-qualify under today’s tighter rules

- Reduce or eliminate the HELOC altogether

Now layer in human behaviour.

As people use the HELOC over time—for renovations, consolidations, or “temporary” cash flow—the balance grows. When renewal time comes, the mortgage may be paid down, but the HELOC is still sitting there, quietly large. It’s about building friction that traps you, to make things so impossibly difficult to move. Suddenly, switching lenders isn’t just inconvenient—it’s impossible.

This is where homeowners feel stuck.

They’re not trapped by a bad rate.

They’re trapped by structure.

The collateralized setup subtly encourages people to keep everything where it is, even when better options exist, because unwinding the structure feels overwhelming. And lenders know this. Collateralization reduces churn. It keeps clients anchored—not because it’s best for them, but because it’s operationally efficient for the institution.

I’ve seen this play out repeatedly: homeowners arrive at renewal assuming they’ll shop around, only to discover their HELOC has effectively handcuffed them to their current lender. Not because they made a reckless decision—but because no one explained how the structure really works at the beginning.

This is why HELOCs aren’t just about access to credit. They’re about long-term mobility. And once that mobility is gone, options disappear quietly, not dramatically.

Now you’ve lost your ability to negotiate rate.

Understanding this risk upfront—before the HELOC is set up—is the difference between flexibility and entrapment.

Variable Interest Rates Can Destabilize Cash Flow

HELOCs float. Always.

That means your borrowing cost moves whether your income does or not. And we don’t need hypotheticals—we just lived through a period where HELOC rates jumped dramatically in a very short time.

Interest-only payments that felt manageable suddenly became painful.

Now layer in:

- Commission or self-employed income

- One spouse on leave

- Already-tight monthly margins

That “cheap” HELOC turns into a constant source of stress.

Yes, many HELOCs allow portions to be locked into fixed rates—but only if you still qualify, and often only after cash flow has already been squeezed.

Volatility doesn’t announce itself politely. It just shows up.

When Your Home Becomes Financially Exposed

A mortgage is expected. A HELOC feels different.

Every dollar borrowed is secured directly against your home—the asset most people associate with safety, not leverage.

That matters more than people realize.

Missed payments can freeze access.

Credit deterioration can reduce limits.

In rare cases, lenders can demand repayment.

Even when none of that happens, many homeowners feel an underlying tension knowing their home has also become their emergency fund.

For some people, that flexibility feels empowering.

For others, it quietly erodes peace of mind.

If simplicity and certainty help you sleep at night, a HELOC can do the opposite.

HELOC Debt Rarely Shrinks on Its Own

This is the trap no one plans for.

HELOCs:

- Don’t amortize

- Don’t mature

- Don’t force repayment discipline

You can service interest indefinitely and never reduce the balance.

I regularly meet people in their 50s and 60s who proudly paid off their mortgage—yet still carry a large HELOC opened years earlier.

It started as:

- A renovation

- A bridge loan

- A “temporary” solution

It ended as permanent leverage.

Without a clear, intentional exit plan, HELOC balances tend to linger far longer than intended, quietly delaying financial freedom and retirement goals.

Not All HELOCs Are Created Equal

This is where many borrowers—and even professionals—get tripped up.

A HELOC is not one product. It’s a family of products, and lender differences matter.

HELOCs can vary by:

- Standalone vs. readvanceable structures

- Fixed limits vs. dynamically increasing limits

- How aggressively lenders monitor credit and property values

- How easily access can be frozen

- Pricing spreads over prime

- Options—or restrictions—for locking into fixed rates

- Standard vs. collateral charges

Two homeowners can both say, “I have a HELOC,” and be living in completely different financial realities.

Treating a HELOC like a commodity is dangerous. The fine print isn’t fine—it’s decisive.

A Story I See Too Often

A couple sets up a HELOC “just in case.”

They renovate. Then consolidate. Then income dips.

They’re not reckless. They’re normal.

The balance grows quietly. Rates rise. Payments sting. Stress creeps in. And now the HELOC—meant to reduce anxiety—is the source of it.

When they finally reach out, the question isn’t:

“Should we have gotten a HELOC?”

It’s:

“Why didn’t anyone explain how this could unfold?”

What This Looks Like in Practice

For realtors

- Avoid presenting HELOCs as standard or automatic

- Flag behavioural and cash-flow risks early

- Encourage clients to think beyond approval into outcomes

For clients

- Treat HELOCs like loaded tools, not conveniences

- Set written rules for use and repayment

- Assume worst-case scenarios before hoping for best-case ones

Allen’s Final Thoughts

A HELOC is not dangerous by default—but it is deceptively powerful.

It doesn’t just change your balance sheet.

It changes behaviour, emotions, and how long debt sticks around.

For some homeowners, that flexibility is a strength.

For others, it’s a slow leak they don’t notice until pressure hits.

The smartest financial decisions aren’t about maximizing access to money. They’re about choosing tools that reinforce discipline, resilience, and peace of mind.

If you’re considering a HELOC, don’t just ask whether you qualify. Ask whether it truly makes your financial life stronger.

That’s where real advice—not product sales—makes all the difference.