…Thinking Outside the Bank to Finance Your Home

Buying a home isn’t always a straight line, and Merix Financial is built for the detours. Merix is a monoline mortgage lender – meaning they only do home loans, and they focus on doing them really well. They work entirely through brokers (no branches), so they offer flexibility that big banks often don’t. In other words, Merix can be your best move when a traditional lender’s box is just too tight for your situation.

Here are the topics we’ll cover:

Qualifying for Your First Home with Merix

When Your Income or Life Doesn’t Fit a Bank’s Template

Specialty Programs: Doctors, Newcomers, and Other Heroes

Investing or Renting? Merix Has You Covered

Bridging Gaps: Borrowed Down Payment & Bridge Loans

When Merix Might Not Be the Best Move

How to Prepare Your Merix Application

What is Merix?

Merix is a dual-channel monoline lender. That’s like being 2 mortgage lenders in one.

The first lender is their Prime division (Merix Standard Channel) where Merix competes directly with:

- The Big Banks

- Major monolines

- Prime insured and insurable lenders

Clients of this channel:

- Strong credit borrowers

- Standard income verification

- Insured, insurable, and conventional deals

- Competitive rates (often beating banks)

- More favourable IRD penalty calculations than many banks

- Portability and standard prime features

If you qualify cleanly within prime guidelines, this is the channel we go with.

This is the side of Merix that most people are referring to when they say “Merix competes with and usually beats the banks.”

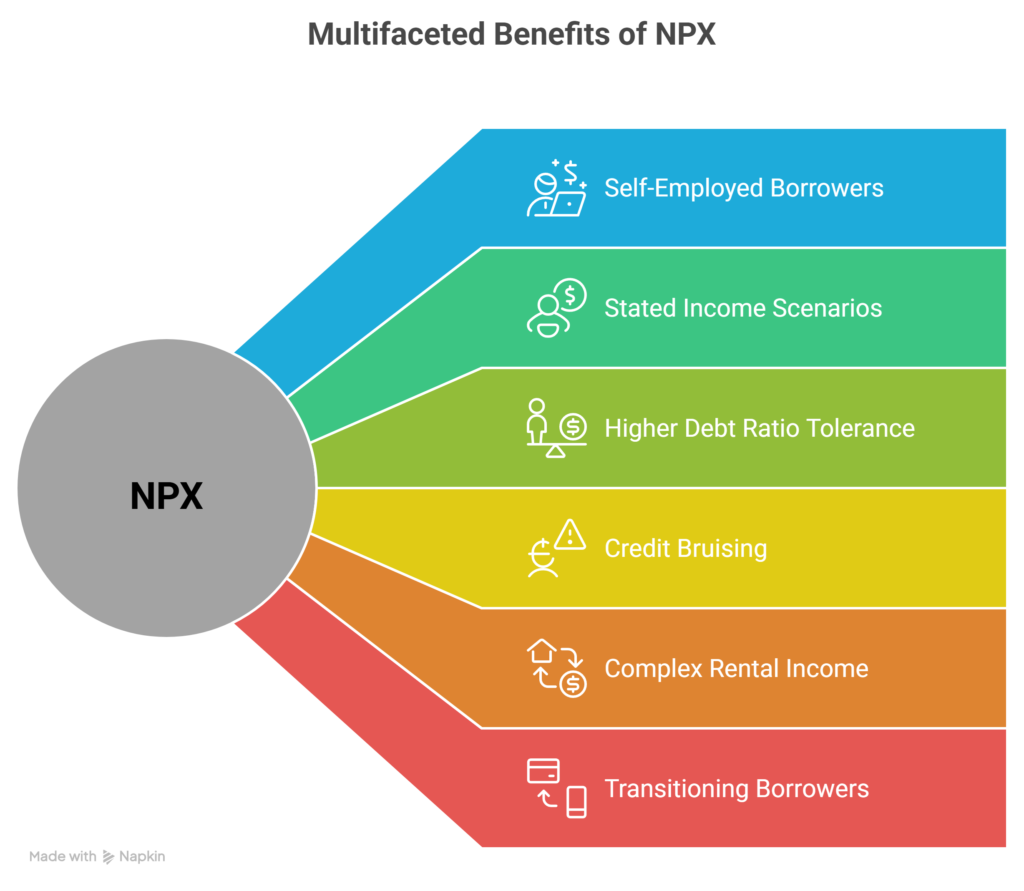

The second lender is Merix’s alternative division (NPX).

You may need a little more help and understanding, or your situation may be a little more complicated. If so, Merix NPX is for you.

This is not private lending — it’s structured, institutional alternative lending.

NPX is designed for:

- Self-employed borrowers with income challenges

- Stated income scenarios

- Higher debt ratio tolerance

- Credit bruising (not catastrophic, but outside prime box)

- Complex rental income structures

- Borrowers transitioning from alternative back to prime

NPX products include:

- XTEND

- EXACT

- AXIS

- XTREME

These programs expand qualification guidelines while still being institutional — meaning rates are higher than prime, but significantly lower than private lending.

This is what makes Merix strategically powerful:

They can serve both the clean borrower and the “almost clean” borrower under one umbrella.

Qualifying for Your First Home with Merix

If you’re stepping onto the property ladder, Merix can be a helpful partner.

For example, Merix makes fixed-rate mortgages customizable: you can pick weekly or monthly payments, and you even have portable and assumable mortgage options (meaning you can move the loan to your next home). These perks help first-timers manage costs and stress. If you are short on cash, Merix can also combine tools – like flexible down payment options – to get the deal done.

Realtor Tip: If a first-time buyer says “I barely have 5% saved,” remember Merix’s Borrowed Down Payment Program. You can suggest they explore it: it lets them cover 100% of their down payment with borrowed funds (like a loan) if needed. That way, your client can qualify sooner and still buy the house they want.

When Your Income or Life Doesn’t Fit a Bank’s Template

Banks love straight paycheques. But what if you’re a freelancer, contractor, or run your own business? Merix’s website highlights a whole NPX suite of products for these scenarios. For example, the XTEND Mortgage boosts your borrowing power by using non-stress-tested rates, extended debt ratios, and even considering rental income. The EXACT Mortgage lets you qualify at your contract rate with a longer amortization (useful if your income might rise). The AXIS Mortgage is tailored for small business owners or investors who need flexible debt ratio rules. And XTREME is built for people with variable income – think tradespeople or consultants.

In plain terms, this means Merix will dig deeper into your actual finances. If you take big business deductions or have a variable gig, your bank might turn you down. Merix will instead look at your 12-month bank statements, accountant letters, or rental contracts. This can significantly increase the loan amount you qualify for.

Client Scenario: You’re self-employed and your tax returns are very low (thanks to deductions), but you have strong deposits. A Merix broker could use the XTEND product: it allows “stated income” and skips the big bank stress test. Merix might approve a higher mortgage based on your cash flow, letting you buy that home you need.

Speciality Programs: Doctors, Newcomers, and Other Heroes

Merix offers niche solutions too. If you’re a new doctor or dentist, their Medical Professionals Program lets you qualify on your future income. In practice, Merix will look at the salary you’ll earn as a licensed professional, even if you’re currently a resident or in school. You can finance up to 90% of the home’s value under this program, which banks often won’t allow for someone just starting their career.

If you’re new to Canada, Merix’s New to Canada Program is helpful. The site calls it “flexible and simple”, allowing you to use gifted down payment funds or work subsidies. They’ll look at alternative credit (like international credit history) and won’t automatically decline you for a lack of Canadian credit. The site notes you can qualify with a mix of savings and gifts, and you still have all the normal mortgage term options (fixed or variable).

Realtor/Client Example: Suppose you have a client finishing medical residency. The banks want two years of pay stubs, which they don’t have. Merix’s medical program would let them use the projected MD salary for qualification. Or imagine a buyer who just became a permanent resident last year. You can point out that Merix accepts gift letters and lets you qualify with flexible credit data – a big relief for someone without a two-decade Canadian credit history.

Investing or Renting? Merix Has You Covered

Buying a rental property or second home? Merix handles that too. They explicitly offer a Second Home Program up to 95% LTV if you (or your family) will occupy it part of the year. This higher LTV for a second home is more generous than many banks allow. They also have a Rental Property Program: if the home will be fully rented out, Merix has an option for you. Their NPX AXIS Mortgage is also a go-to for small investors, as it’s designed for people with rental income.

In practical terms, if you’re buying a duplex to rent or a vacation place to use some weekends, Merix can work with you. The website says the rental program is “perfect for homeowners looking to purchase an investment property” that’s fully rented. And the second-home program will finance up to 95% of the price as long as you’ll live there at some point.

Bridging Gaps: Borrowed Down Payment & Bridge Loans

Sometimes you need cash flow flexibility. Merix offers two solutions:

- Borrowed Down Payment Program: This lets you cover your down payment with borrowed funds. As Merix explains, “Whether it’s the full down payment amount, or just a portion, any amount can qualify” under this program. In other words, you can take out a loan or use a line of credit for your down payment and still get approved.

- Bridge Financing: This is a short-term loan for buying before selling. Merix’s bridge loan “gives you the funds you need to make an offer” on your new home before you close on your old one. It can cover your down payment and closing costs so you don’t have to rush. Once your old home sells, you use those proceeds to pay off the bridge loan.

Client Example: Suppose you’ve taken a private construction loan during a renovation. You finish the reno and want to lock in a better rate. You could use Merix’s refinancing (via an NPX product) to pay off that private loan. (Merix doesn’t explicitly advertise a “private mortgage payoff”, but their refinancing solution can effectively do that.) Or say you’re upgrading homes and need to overlap closings: a Merix bridge loan has you covered.

When Merix Might Not Be the Best Move

Truth is, because Merix is a dual-channel monoline lender, there are very few people who would not benefit from being under the Merix umbrella.

If you have:

- Multiple recent collections

- Active consumer proposal or bankruptcy (very recent)

- Major payment defaults

- Severely damaged credit

You are probably not going to qualify for their prime channel, but you will likely qualify for their NPX (Alternative) lending division as Merix is extremely flexible.

However, even under NPX, there are limits.

If your total monthly obligations (mortgage + property taxes + heating + condo fees + car loans + credit cards + lines of credit + personal loans) consume too much of your income, Merix may decline.

For example:

Prime lenders typically allow up to about 44% of your gross monthly income to go toward total debt.

NPX may allow higher, depending on strength of the file.

But if you’re dramatically overleveraged, Merix won’t stretch into unsafe territory.

That’s where private lending may temporarily be required.

Heavy Construction or Raw Land Financing

Merix is not a construction lender in the traditional sense.

If you need:

- Raw land financing

- Complex multi-draw construction financing

- Heavy renovation draws with engineering oversight

You’re looking at:

- Construction-focused lenders

- Credit unions

- Or private construction financing first

Merix is ideal once the property is complete or near completion — not for speculative build phases.

Highly Complex Commercial or Mixed-Use Deals

Merix focuses on residential lending.

If the property is:

- Heavy commercial

- Mixed-use with significant commercial square footage

- Multi-unit beyond residential limits

You’re likely outside their appetite.

That’s commercial financing territory.

Ultra-Short-Term Speculators

If you are:

- Planning to flip within 3–6 months

- Buying purely for short-term arbitrage

- Using extremely high leverage intentionally

Merix may not align with your strategy.

Their products are structured for residential ownership — not short-term speculative turnover.

How to Prepare Your Merix Application

If Merix seems like the right choice, here’s what to do next:

- Gather Income Documents: Get your pay stubs, a letter of employment, T4 slips, NOAs, or 12 months of business bank statements. Merix will need proof of how you earn money.

- Prepare Down Payment Proof: Show bank statements for your savings or retirement funds. If any part of your down payment is a gift or loan, have those documents ready (e.g. a gift letter or loan statements).

- Collect Property Info: Have the property listing or appraisal, and info on any existing mortgage or liens. Merix uses this to verify the value.

- Tell Your Story: Be upfront about anything unusual – self-employment, co-signed debts, past credit bumps, etc. I will frame this for the Merix underwriters.

- Submit and Follow Up: I will enter everything into Merix’s system. Once you have a commitment, Merix’s checklist tells you exactly what to bring to closing: income verifications and down payment confirmations, for instance. Stay responsive so nothing stalls the approval.

Following these steps (and double-checking documents) will smooth the process.

Story: From Private Lender to Merix

Imagine Sarah’s situation: She needed to finish her home, so she took a short-term private mortgage at 10% interest. Now construction is done and she wants to lock in a better rate. The big banks declined her because her debt load looked high. I took her file and highlighted that the home is completed and her income is solid. Merix approved her refinance at about 6%. The result? Sarah’s payment dropped by 40%, and she’s on a stable 5-year term. This shows Merix’s strength: bridging you back to conventional financing when a bank can’t. (Merix’s site doesn’t spell out “private refinance,” but this use case is exactly the kind of transition their products support.)

Allen’s Final Thoughts

Merix Financial is a flexibility play. Not only do they often beat the banks on rate, their mortgage penalties if you have to break your mortgage are usually significantly less. They’ve funded mortgages for 200,000 Canadians over 20 years, so they know what they’re doing. Their specialty is structuring deals – be it for self-employed income, doctors, new immigrants, or complex property purchases – that mainstream lenders won’t touch easily.

As your mortgage agent, my goal is to guide you to the right lender. I’ll honestly assess your profile: if you fit a bank’s rules perfectly, I’ll steer you to prime. If your situation is a bit outside the norm, I’ll tell you how Merix can help. I’ll coordinate the application, make sure you have all the right documents (T4s, NOAs, bank statements, etc.), and advocate for you with Merix. For example, if you co-signed a loan, I’ll explain to Merix how we can exclude that debt if someone else is paying it off. I’ll highlight your strengths (like strong assets or steady rental income) so Merix sees the full picture.

In short, I’m here to translate your life situation into Merix’s language. Whether it’s a personal visit, a phone call, or email, I will make sure you’re prepared for the unique aspects of a Merix application. My promise is to keep you informed, get you the best possible rate and terms Merix will allow, and get you into your home.

Ready to see if Merix is right for you? Contact me and let’s discuss your goals – I’m here to help you find the path to homeownership, whether it’s with Merix or another lender that best fits your needs.