Navigating the real estate market can be complex, especially when conditions like “sale of current property” clauses—commonly referred to as Sale of Buyer’s Property (SBP) conditions—come into play. With the cooling real estate market, these conditions have made a strong comeback, impacting buyers, sellers, and even mortgage financing strategies. Whether you’re a home buyer, a financial planner advising clients, or a realtor facilitating these transactions, understanding the nuances of this clause is essential for making informed decisions.

What is a Condition of Sale of Buyer’s Property?

Key Features of the SBP Condition

When Is the SBP Condition Used?

Key Challenges with SBP Clauses in Mortgage Financing

John and Mary: Sale by Buyer Story

Example: Sale of Buyer’s Property Condition

Actionable Takeaways for Home Buyers

Actionable Takeaways for Home Sellers

What Is a Condition of Sale of Buyer’s Property (SBP)?

An SBP condition allows buyers a specific period to sell their existing home before committing to the purchase of a new one. If their property does not sell within the agreed timeframe, they can opt out of the purchase agreement without penalties. While this condition provides a safety net for buyers, it introduces layers of complexity for sellers and can influence mortgage financing.

Key Features of the SBP Condition

The ‘Sale of Buyer’s Property’ condition has 3 essential features you need to be aware of. There are:

- Contingency on Selling Current Home

- Specified Timeframe

- Escape Clause

Contingency on Selling Current Home

The buyer’s ability to finalize the purchase of the new property is dependent on selling their existing home. If they cannot sell their home within the agreed timeframe, they can back out of the deal without penalty.

Specified Timeframe

The SBP clause typically includes a deadline (e.g., 30 or 60 days) by which the buyer must sell their property. If the property does not sell, the agreement is null and void.

Escape Clause

Most SBP conditions include an “escape clause” to protect the seller. This allows the seller to continue marketing their property and accept other offers. If the seller receives a better offer, they must notify the first buyer, who then has a limited time (usually 24–48 hours) to waive the SBP condition or let the deal fall through.

When Is the SBP Condition Used?

The SBP condition tends to be used when the real estate market is slow and it takes home longer to sell. Buyers may use an SBP condition to ensure they’re not financially overcommitted. Often they don’t know how much they can get for their current home and there is uncertainty if it will sell at the price they want. These buyers need the proceeds from their current home sale to fund the down payment or closing costs for the new home.

Key Challenges with SBP Clauses in Mortgage Financing

There are some unique challenges to financing a deal that contains an SBP condition as the condition introduces uncertainties around the amount of down payment the purchaser will be able to bring to the deal, affecting loan-to-value ratios. Loan-to-value ratios have a direct impact on mortgage qualification and the interest rate of the mortgage. This condition not only causes difficulties for the buyer’s financing of the deal but also the sellers’ ability to make any financing arrangements themselves as they are uncertain if their home will sell.

Financing Approval Delays

One of the most significant challenges with SBP conditions is the delay in securing mortgage financing. Most lenders are reluctant to approve financing for a new property if the buyer’s current home sale is uncertain. This delay can create a ripple effect, potentially jeopardizing the transaction.

Valuation Concerns

Lenders often require firm data on the sale price of the buyer’s current property to assess their borrowing capacity. Without a finalized sale, lenders may undervalue the buyer’s financial position, affecting the size and terms of the mortgage.

Market Risk

In a slow real estate market, buyers might struggle to sell their current property, leaving their ability to fulfil the SBP condition in question. Sellers are equally at risk if the deal falls through due to the buyer’s inability to secure financing.

Chain Reactions

When multiple SBP conditions are linked in a chain (e.g., Buyer A needs to sell to Buyer B, and so on), a single failed sale can collapse the entire sequence of transactions, creating financial and emotional stress for all parties involved.

Escape Clauses and Legal Complexities

For sellers, escape clauses (allowing them to accept another offer while the SBP is pending) can lead to legal complications if poorly worded. Without proper protections, sellers might inadvertently commit to multiple contracts, risking potential lawsuits.

Mortgage Agent Perspective

The real tricky thing about the Sale of Buyer’s Property condition is that, from a lender’s perspective, important information that determines if the borrower will receive a mortgage commitment is missing.

First, since the buyer hasn’t sold their home yet, we don’t know how much down payment they will bring to the purchase of the new home. This means we don’t know the borrower’s borrowing capacity (debt ratios) or the amount of mortgage the borrower will need to purchase the new home. Further, we cannot calculate loan to value on the new home, which is a key ratio in determining what kind of mortgage is needed, if mortgage default insurance is required, what interest rate is available, what mortgage product is most suitable, and so forth.

Fundamentally, until the Sale of Buyer’s Property condition has been waived by fulfillment (sale of buyer’s home), lenders cannot begin to underwrite the mortgage.

To address the Sale of Buyer’s property condition so it does not conflict with the condition of financing, it is wise if realtors chain conditions in the offer to facilitate mortgage underwriting after the Sale of Buyer’s property condition has been satisfied by fulfillment. For a more in-depth conversation, contact Allen Ehlert.

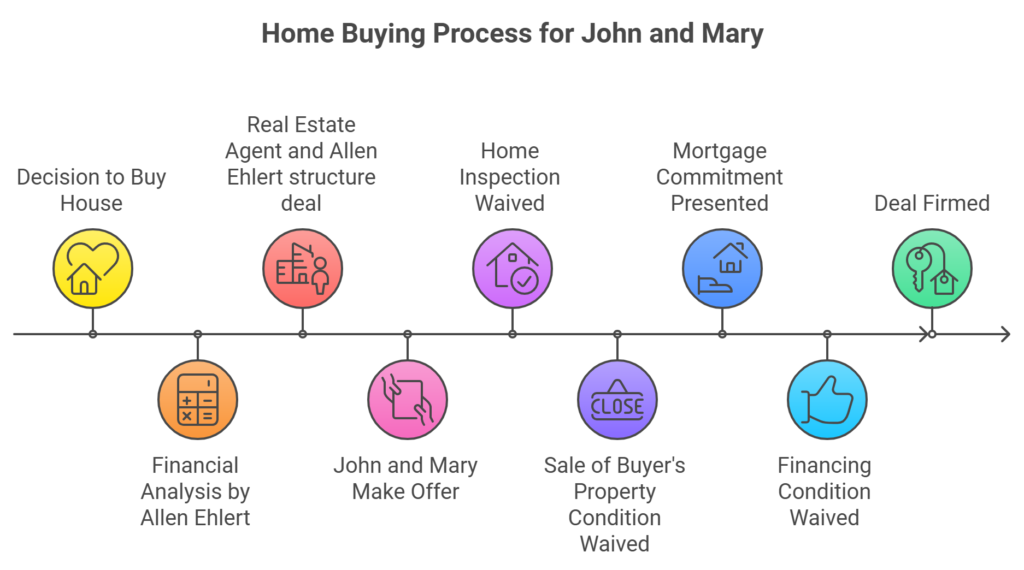

John and Mary: Sale by Buyer Story

Homeowners John and Mary want to make an offer to purchase a very cute home closer to work to shorten their commute and enhance their lifestyle. Unfortunately, they haven’t put their house up for sale yet. They have spoken with 3 different real estate agents; each provided a different assessment as to how much John and Mary can get for their home.

John and Mary have been working with mortgage agent Allen Ehlert. Based on their financial, professional, and personal profile, Allen Ehlert took the assessments of the different realtors and conducted a pro forma analysis so John and Mary could get a good idea about the most suitable mortgage product for them, given their goals and objectives, and how buying this very cute home would impact their broader finances. Basically, they needed to ask Allen Ehlert, “Can we afford this home?”

Once Allen Ehlert demonstrated that this very cute home was within their reach, not wanting to lose out on getting this very cute home, John and Mary asked their chosen real estate agent to make an offer on the house conditional on financing, home inspection, and Sale of Buyer’s Property.

As John and Mary are working with mortgage agent Allen Ehlert, they had their real estate agent give him a call. Their real estate agent sought the advice of Allen Ehlert on how to structure the offer from a financing perspective. Allen Ehlert suggested that the period for the condition of financing begins after the Sale of Buyer’s Property has been fulfilled. By chaining the conditions, the deal is not put at risk by having insufficient time to get a mortgage commitment from a lender. Further, given the nature of the Sale of Buyer’s Property condition, sellers will understand why the timing of the conditions are being put in an order.

The offer was accepted by the seller of the very cute home.

John and Mary immediately put their home on the market. They arranged a home inspection on the very cute home 4 days later. The home inspection was satisfactory, and John and Mary waived condition of home inspection immediately. This made the seller feel more secure that the deal would firm up.

After 12 days from offer acceptance, John and Mary accepted an offer on their house, condition of financing, and home inspection. They communicated the acceptance of this offer pending conditions to the seller of the very cute house because good communication is key to ensuring more complex deals are successful. After 5 days the buyer of John and Mary’s home waived conditions and the deal was firm.

John and Mary immediately waived the condition of Sale of Buyer’s Property.

John and Mary contacted mortgage Allen Ehlert and provided all the required documentation around the sale of their home. Allen Ehlert began underwriting their file and 3 days later presented John and Mary with a Mortgage Commitment. Allen Ehlert reviewed the conditions of the Mortgage Commitment with John and Mary.

Feeling confident they could meet those conditions, John and Mary signed the Mortgage Commitment and waived their last condition, condition of financing, to firm up their purchase of that very cute home.

Example: Sale of Buyer’s Property Condition

Imagine Sarah, a buyer, submits an offer to purchase a home contingent on selling her current property within 30 days. The seller accepts the offer, including a 24-hour escape clause. Two weeks later, another buyer submitted a higher, unconditional offer.

Sarah now has 24 hours to remove her SBP condition. However, her current property has not sold, and her lender cannot finalize financing without a confirmed sale price. As a result, Sarah must withdraw her offer, and the seller moves on to the second buyer.

This situation underscores the importance of proactive planning and expert guidance when dealing with SBP conditions.

Actionable Takeaways for Home Buyers

Have a Contingency Plan. Work with your realtor and mortgage agent to prepare for scenarios where your current property doesn’t sell as planned. Consider bridge financing if your financial profile and lender allow it.

Price Your Home Strategically. A competitively priced home increases the likelihood of a quick sale, aligning with the timeline in your SBP clause. Use professional staging and high-quality photography to attract buyers.

Negotiate Favorable Terms

Request longer timelines (e.g., 60 days instead of 30) in the SBP clause to give yourself ample time to sell your home. If possible, negotiate for 48 or 72 hours on escape clauses to provide more breathing room if another offer comes in.

Actionable Takeaways for Sellers

Vet the Buyer’s Sale Plan. Ask for details about the buyer’s current property, including its condition, listing price, and marketing strategy. Confirm the buyer’s agent is the same one handling their home sale to ensure continuity.

Use Precise Wording in Escape Clauses. Ensure the clause specifies that buyers must remove all conditions if notified of a better offer, not just the SBP condition.

Minimize Listing History Risks. Keep your property actively marketed to maintain interest and mitigate risks if the SBP falls through.

Expert Insight: Mortgage Agent Perspective

“Lenders view SBP conditions cautiously. Buyers should have a pre-approval and discuss backup financing options early to avoid surprises.” — Allen Ehlert, Licensed Mortgage Agent

Data Points to Consider

- Market Trends: SBP conditions become more common in balanced or buyer’s markets. A recent report found that 60% of conditional offers in slower markets include SBP clauses.

- Average Sale Times: Homes in slower markets take 45–60 days to sell, often exceeding the timelines in SBP clauses.

- Chain Reaction Stats: Approximately 20% of SBP-related transactions in linked chains face delays or fall through entirely.

Read More:

- Real Estate Conditions

- Financing Condition

- Home Inspection Condition

- Sale of Current Property Condition

- Status Certificate Condition

- Appraisal Condition

Summary

Whether you’re buying, selling, or advising clients, understanding the intricacies of SBP conditions is critical. Buyers must approach these clauses with realistic expectations and solid contingency plans, while sellers need clear, protective escape clauses to avoid legal and financial pitfalls.

Next Steps:

- For Buyers: Contact your mortgage agent to discuss financing options and prepare for a competitive offer strategy.

- For Sellers: Collaborate with your realtor to vet offers thoroughly and craft protective clauses.

- For Realtors: Educate your clients about the risks and benefits of SBP conditions to build trust and achieve smoother transactions.

Schedule a consultation with Allen Ehlert to assess your financial readiness for SBP offers.

By equipping yourself with knowledge and working with experienced professionals, you can confidently navigate SBP conditions and achieve your real estate goals.