The structure of the regulatory framework for the mortgage industry in Canada is intricate and multi-layered, involving federal, provincial, and municipal entities along with key market participants such as the Bank of Canada and the Canada Mortgage and Housing Corporation (CMHC). This article explores the roles and responsibilities of these entities, detailing how they collectively contribute to controlling the mortgage industry, protecting Canadians, and ensuring a healthy mortgage market.

Federal Level Regulation

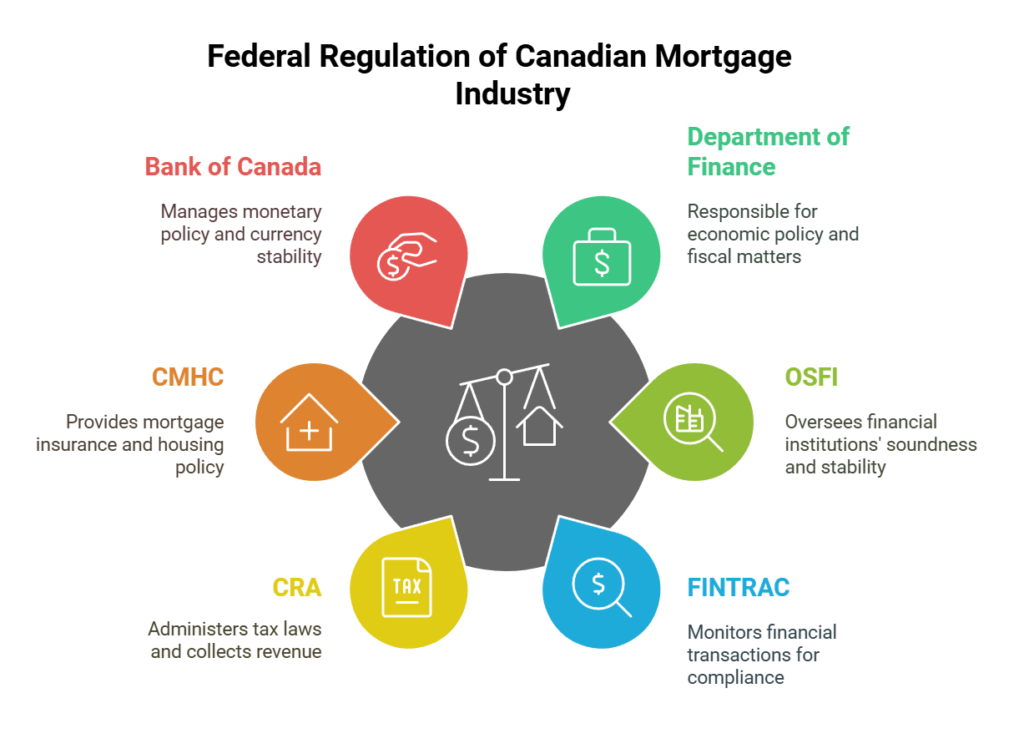

At the federal level, the Canadian mortgage industry is regulated and influenced by the following federal government entities:

- Department of Finance

- Office of the Superintendent of Financial Institutions (OSFI)

- Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

- Canada Revenue Agency (CRA)

- Canada Mortgage and Housing Corporation (CMHC)

- Bank of Canada

Department of Finance Canada

At the federal level, the Department of Finance plays a pivotal role in overseeing the Canadian mortgage landscape. It develops policies related to financial institutions, including mortgage lending practices, and sets regulatory frameworks aimed at maintaining the stability and integrity of the financial system.

The Federal Department of Finance is the most central and powerful entity in the regulation of the mortgage industry, but its role is more about setting broad economic policies and regulatory frameworks rather than direct oversight or enforcement. It influences the mortgage market primarily through legislative measures and fiscal policies that impact the overall financial and economic environment in Canada.

Key responsibilities of the Department of Finance in the mortgage sector include:

- Policy Development: The Department of Finance develops policies that influence the entire financial sector, including mortgage lending. These policies can affect everything from mortgage qualifications to interest rates and the overall stability of the housing market.

- Legislative Role: The department proposes and helps enact legislation that governs the operation of financial institutions, mortgage rules, and the housing market. This includes adjustments to the laws that can impact mortgage insurance, lending practices, and borrower qualifications.

- Economic Management: Through its management of economic policy, the Department of Finance impacts inflation, employment rates, and Canada’s overall economic growth, which in turn influences mortgage rates and housing demand.

However, while the Department of Finance sets the stage for regulatory policies, other federal entities like the Office of the Superintendent of Financial Institutions (OSFI) and the Canada Mortgage and Housing Corporation (CMHC) play more direct roles in regulation and enforcement. OSFI, for example, is responsible for supervising and regulating banks and other financial institutions to ensure that they are sound and compliant with the established guidelines, such as the B-20 guideline on residential mortgage underwriting practices.

In conclusion, while the Department of Finance is extremely influential due to its capacity to shape financial legislation and economic policy, the most “powerful” entity in terms of direct regulation and oversight of the mortgage industry might be considered OSFI, due to its regulatory and supervisory functions.

Office of the Superintendent of Financial Institutions (OSFI)

OSFI is an independent agency that regulates and supervises financial institutions and pension plans at the federal level. It ensures that banks, insurance companies, and trust and loan companies are sound, competitive, and resilient. In the mortgage sector, OSFI sets and enforces guidelines, such as the B-20 residential mortgage underwriting practices and procedures, which include stress testing borrowers’ ability to repay loans.

The B-20 guideline, officially known as “Residential Mortgage Underwriting Practices and Procedures,” is a set of standards issued by the Office of the Superintendent of Financial Institutions (OSFI) in Canada. These guidelines are designed to ensure that both federally regulated lenders, such as banks, and borrowers practice sound and prudent underwriting procedures when issuing residential mortgages. First introduced in 2012 and subsequently updated (most notably in 2017 and again in 2020), the B-20 guideline aims to strengthen the Canadian housing market by requiring lenders to adhere to more rigorous standards.

Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

FINTRAC is the central federal agency responsible for detecting, preventing, and deterring money laundering and the financing of terrorist activities in Canada. It collects, analyzes, and discloses financial information and intelligence on suspected money laundering and terrorist financing activities. Mortgage lenders, brokers, and other financial entities are required to report suspicious transactions, large cash transactions, and international electronic fund transfers to FINTRAC.

Increasingly, FINTRAC is requiring licensed mortgage professionals to collect information about mortgage applicants and pass that information to FINTRAC. Such requirements are adding to the amount of support documentation mortgage professionals must collect from Canadians.

Canada Revenue Agency (CRA)

The CRA is involved in combating money laundering in the real estate sector, including mortgages, through its enforcement of tax laws and audits. It collaborates with other agencies to investigate financial crimes where tax evasion may be related to money laundering activities.

There is continuing conversation between industry players in regards to the identification of borrowers and the prevention of money laundering for the CRA to create a portal or some other technology licensed mortgage participants can access to verify financial and identification information on mortgage applicants.

Canada Mortgage and Housing Corporation (CMHC)

CMHC, a Crown Corporation, serves as a central pillar in Canada’s housing market by providing mortgage liquidity, housing assistance, and research. CMHC’s mortgage-backed securities and Canada Mortgage Bonds programs significantly support the availability and affordability of mortgage financing. CMHC also administers the National Housing Act, facilitating various housing programs and risk management tools to protect and stabilize the mortgage market.

Bank of Canada

The Bank of Canada contributes indirectly to mortgage regulation through its monetary policies, primarily by setting the key interest rate which influences mortgage rates across the country. Its policies are critical in controlling inflation and stabilizing the economic environment, impacting mortgage lending rates and the borrowing costs for Canadians.

Provincial Level Regulation

At the provincial level, the Canadian mortgage industry is regulated and influenced by the following provincial government entities:

- Provincial and Territorial Regulators

- Land Title and Property Offices

Provincial and Territorial Regulators

Each province and territory has its regulatory body for mortgage brokers. These regulators ensure licensing, conduct examinations, and enforce local legislation that governs mortgage brokering in their respective regions.

In Canada, each province and territory has its own regulator responsible for overseeing mortgage brokers and lenders. These regulators ensure that industry practices meet provincial standards and protect consumers. Here’s a list of the provincial and territorial mortgage regulators across Canada:

Provincial and Territorial Mortgage Regulators

- Alberta: Real Estate Council of Alberta (RECA)

- British Columbia: British Columbia Financial Services Authority (BCFSA)

- Manitoba: Manitoba Securities Commission

- New Brunswick: Financial and Consumer Services Commission (FCNB)

- Newfoundland and Labrador: Service NL

- Nova Scotia: Nova Scotia Securities Commission

- Ontario: Financial Services Regulatory Authority of Ontario (FSRA)

- Prince Edward Island: Consumer, Corporate and Insurance Division of the Department of Justice and Public Safety

- Quebec: Autorité des marchés financiers (AMF)

- Saskatchewan: Financial and Consumer Affairs Authority of Saskatchewan

- Northwest Territories: Department of Municipal and Community Affairs

- Nunavut: Department of Community and Government Services

- Yukon: Professional Licensing & Regulatory Affairs, Department of Community Services

These entities regulate various aspects of the mortgage industry within their jurisdictions, including licensing, compliance with local laws, and consumer protection. They also play a crucial role in maintaining the integrity and professionalism of the mortgage industry.

Land Title and Property Offices

Provincial land title offices play a crucial role in the mortgage process by managing the registration and transfer of property titles, which is essential for the execution of mortgage agreements. This function ensures the legality and enforceability of mortgages, contributing to market security and integrity.

For example, a mortgage charge, commonly referred to as a mortgage lien, is registered with the land titles office or land registry in the province where the property is located. This registration process ensures that the mortgage is recognized as a legal claim against the property by any parties reviewing the title. Here’s how it typically works across different provinces:

Land Titles Office or Land Registry System

- Land Titles System: In provinces that use a land titles system (also known as the Torrens system), the mortgage is registered directly against the title of the property. This system provides a high level of certainty and security of title, as the government guarantees the accuracy of the records. Provinces like Alberta, British Columbia, Manitoba, and Saskatchewan operate primarily under this system.

- Registry System: Some provinces still use a registry system where the details of the mortgage are recorded, but the system is based more on the documentation rather than a guarantee of title. This system is less common and is being phased out in many areas in favour of the more secure land titles system. Nova Scotia, for example, has areas that still operate under a registry system.

Provincial Examples

- Alberta: Service Alberta manages the land titles registry where mortgages are registered.

- British Columbia: The Land Title and Survey Authority of British Columbia (LTSA) handles all land title registrations.

- Ontario: The Land Registry Offices under ServiceOntario record all real estate transactions, including mortgages.

- Quebec: The Registre Foncier (Land Registry) records all transactions affecting real estate, including mortgages.

- Nova Scotia: The Property Online service allows for the registration and searching of properties, where mortgage documents are registered.

When a mortgage is registered with the land registry office, the mortgage becomes a part of the public record. This allows any interested parties, such as potential buyers or other lenders, to see the encumbrance on the property. This registration helps protect the rights of the lender, ensuring they have a legal claim to the property should the borrower default on the loan.

Municipal Level Regulation

While municipal governments do not directly regulate mortgage lending, they influence the housing market through zoning laws, property tax rates, and development charges. These factors can affect housing demand and supply, thereby indirectly influencing mortgage market conditions.

Property Taxes

Understanding property taxes and their calculations in Canada is essential for homeowners, prospective buyers, and real estate professionals alike. Property taxes are a significant source of revenue for municipalities and directly impact local services and infrastructure. Different jurisdictions have different approaches to calculating property taxes, have variations in tax rates, and offer varying insights into how these taxes can influence property investment decisions.

Zoning

For example, zoning of land is primarily governed at the municipal level, with each municipality establishing its own zoning bylaws based on local needs and planning objectives. These zoning bylaws categorize land into different zones, each with its specific rules regarding the types of buildings and uses that are permissible. Here’s an overview of the common types of zoning categories you might find across Canadian municipalities:

Residential Zoning

- Single-Family Residential: Allows for single detached homes, often with restrictions on the number of dwellings per lot or the proportion of the lot that can be covered by buildings.

- Multi-Family Residential: Permits the construction of apartments, duplexes, triplexes, townhouses, and other multi-unit dwellings.

- Rural Residential: Applies to areas typically outside urban centres, allowing for larger lot sizes and sometimes accommodating agricultural activities.

Commercial Zoning

- Retail Commercial: Designated for areas where retail stores, shopping centers, and service establishments operate.

- Office Commercial: Allows for business offices, often including banks, professional services, and corporate headquarters.

- Mixed-Use Commercial: Encourages a combination of uses, such as commercial spaces on the ground floor with residential units above.

Industrial Zoning

- Light Industrial: Suitable for businesses that do not significantly alter the character of the area or produce high levels of noise, odours, or pollution.

- Heavy Industrial: Intended for more impactful industrial activities that may generate more significant environmental disturbances.

Agricultural Zoning

- Designated for the use of farming, ranching, and other agricultural activities, often including restrictions to protect agricultural land from being developed for non-agricultural purposes.

Institutional Zoning

- Encompasses uses such as schools, hospitals, libraries, and government buildings. This zoning aims to accommodate the needs of community services and facilities.

Recreational Zoning

- Includes land used for parks, sports fields, golf courses, and other recreational purposes.

Environmental Protection Zoning

- Aims to protect areas sensitive to environmental concerns, such as wetlands, forests, and wildlife habitats. This zoning restricts development to preserve ecological integrity.

Special Purpose Zoning

- Used for specific purposes that do not fit neatly into other categories, such as airports, ports, and utilities.

Zoning laws are dynamic and can evolve as the needs and planning objectives of a municipality change. They play a crucial role in urban planning by managing land uses in a way that promotes orderly growth and development while balancing environmental, social, and economic needs.

Summary

The regulatory framework of the Canadian mortgage industry is designed to safeguard the interests of consumers while promoting a stable and efficient market. From the federal government’s high-level economic and financial policies to provincial licensing and educational requirements for mortgage professionals, and even to municipal government housing policies, each level plays a critical role. Entities like the Bank of Canada and CMHC further contribute by influencing interest rates and providing essential housing services, ensuring the system’s overall health and resilience. Together, these regulatory bodies and market participants create a structured environment that supports sustainable mortgage lending practices and protects the financial well-being of Canadians.