… Who Should Use One, and Who Shouldn’t

A Home Equity Line of Credit is often talked about like it’s a single, simple product. As if a HELOC at one lender is basically the same as a HELOC anywhere else. Easy money. Cheap money. Flexible money.

That assumption is where people get hurt.

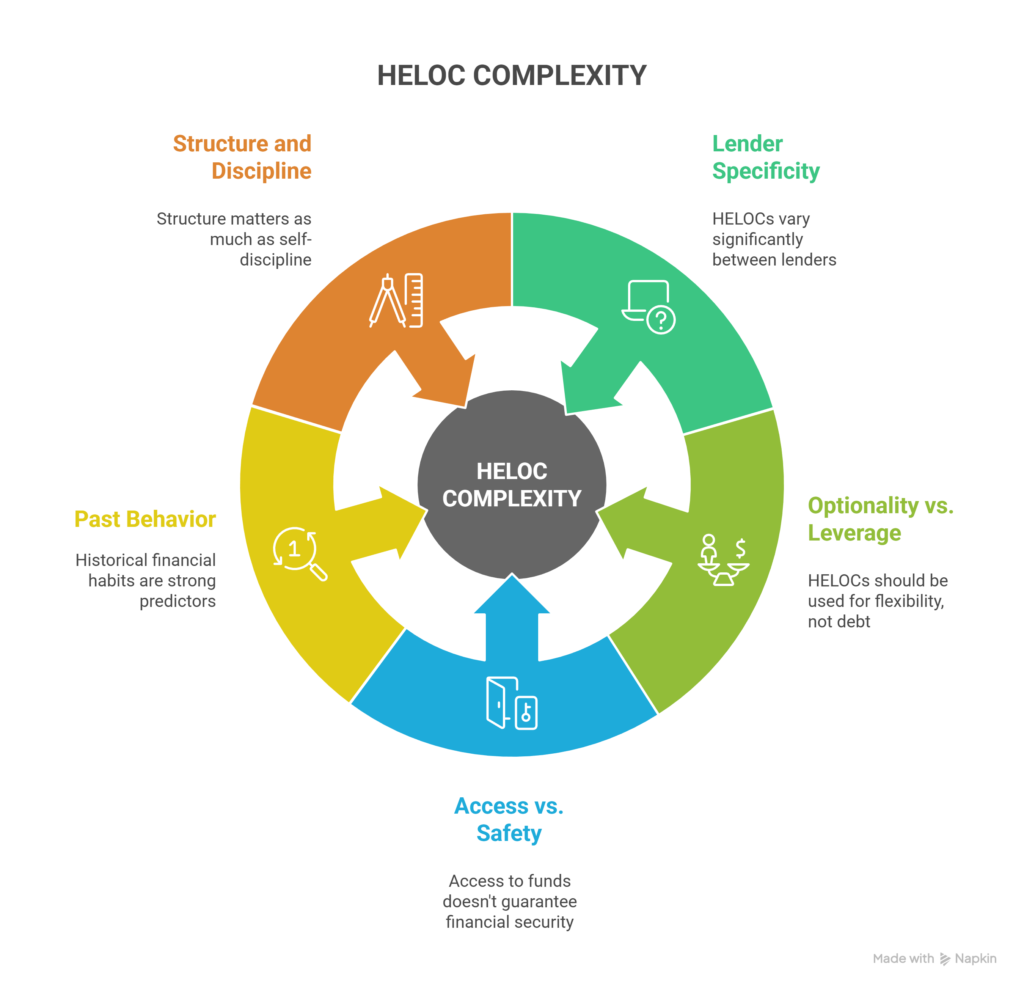

In reality, a HELOC is a complex financial instrument, wrapped in friendly language, sold in very different forms by very different lenders—and it behaves wildly differently depending on who is using it and how it’s structured.

Some borrowers use HELOCs brilliantly and sleep well at night.

Others—yes, including realtors and seasoned investors—end up boxed into corners they didn’t see coming, forced to sell properties, or staring down insolvency.

Let’s slow this down and talk honestly about who should get a HELOC, who should not, and why “a HELOC is not a HELOC.”

The big ideas you need to understand first

- HELOCs are complex, lender-specific products—not commodities

- The right borrower uses a HELOC as optionality, not leverage

- The wrong borrower mistakes access for safety

- Past behaviour predicts HELOC outcomes better than income

- Structure matters as much as self-discipline

Now let’s unpack this properly.

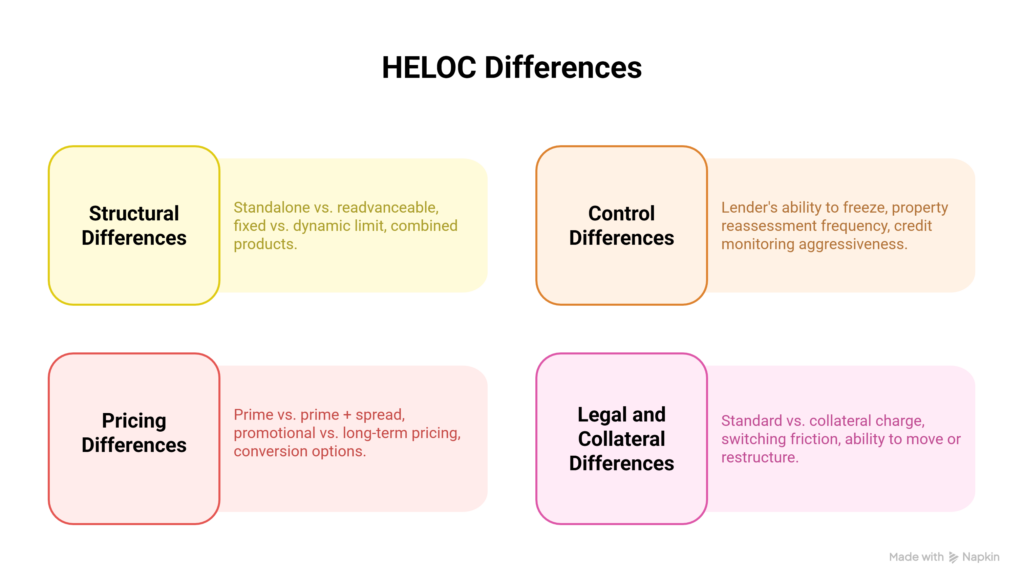

A HELOC Is Not a Commodity—It’s a Family of Products

This is where most people—and frankly many professionals—get tripped up.

A HELOC can differ dramatically depending on the lender:

Structural differences

- Standalone HELOC vs. readvanceable mortgage

- Fixed credit limit vs. dynamically re-advancing limit

- Combined mortgage + HELOC products with internal rules

Control differences

- How easily a lender can freeze the line

- How often property values are reassessed

- How aggressively credit is monitored

Pricing differences

- Prime vs. prime + a spread

- Promotional pricing vs. long-term pricing

- Conversion options to fixed rates (or lack thereof)

Legal and collateral differences

- Standard charge vs. collateral charge

- Switching friction and discharge costs

- Ability to move or restructure later

Two borrowers can both say “I have a HELOC” and be living in completely different financial realities.

This is why treating a HELOC as a generic tool is dangerous. The fine print isn’t fine—it’s decisive.

Who Should Get a HELOC

The right HELOC borrower isn’t defined by income. They’re defined by behaviour under stress.

They are structurally conservative, even when they’re successful

This borrower:

- Doesn’t max things “just because they can”

- Leaves buffers everywhere

- Is uncomfortable when debt grows without a plan

They like options—but they respect risk more than opportunity.

They think in exit strategies before entry

They can clearly articulate:

- Why the HELOC exists

- When it will be used

- How it will be paid down

- What happens if rates spike or income dips

There’s a written plan—or at least a mentally rehearsed one.

They can handle variability without panic

Variable rates don’t send them into emotional decision-making. They:

- Can absorb payment swings

- Don’t rely on interest-only minimums

- Aren’t forced sellers when markets move

This emotional stability is critical.

A Story of a HELOC Used Well

I worked with a client—mid-career professional, conservative by nature—who set up a HELOC and barely touched it for years.

When a short-term income disruption hit, they used the line deliberately:

- Covered six months of expenses

- Maintained their credit profile

- Avoided selling investments at the worst possible time

Once income normalized, the balance was aggressively repaid and the line went dormant again.

No drama. No lifestyle inflation. No lingering debt.

That’s a HELOC doing exactly what it’s supposed to do.

Who Should Not Get a HELOC

This has nothing to do with intelligence or ambition. It has everything to do with patterns.

They confuse leverage with safety

This borrower sees:

- Access to money as reassurance

- Equity as “available capital”

- Appreciation as a strategy

They assume tomorrow will bail out today.

That mindset works—until it doesn’t.

They rely on optimism instead of margins

Thin cash flow + variable rates is a dangerous mix.

When life tightens:

- HELOC payments don’t pause

- Rates don’t care

- Lenders don’t negotiate

Flexibility disappears precisely when it’s needed most.

They use HELOCs to chase growth without downside planning

This is where things get ugly.

I’ve seen homeowners—and yes, realtors—use HELOCs to:

- Buy additional properties at peak pricing

- Fund down payments without margin of safety

- Stack leverage assuming perpetual appreciation

Now fast-forward.

Markets soften. Rates rise. Rental cash flow turns negative. Refinancing dries up.

Suddenly:

- The HELOC balance is too large

- The home must sell for a price the market won’t support

- Equity is trapped

- Insolvency becomes a real conversation

The HELOC didn’t cause the problem—but it accelerated it.

A Story of a HELOC Used Poorly

One investor used their HELOC repeatedly to scale. Every deal “worked” on paper—assuming rates stayed low and prices kept rising.

When both assumptions broke:

- HELOC interest costs exploded

- Cash flow collapsed

- Exit options vanished

The home became collateral for a strategy that no longer existed.

This is not rare. It’s just underreported.

What This Looks Like in Practice for Realtors and Clients

For realtors

- Don’t frame HELOCs as “tools everyone should have”

- Ask how clients behaved with debt in the past

- Flag layered leverage risks early

- Encourage conservative structuring—not maximum limits

For clients

- Treat HELOCs as loaded tools, not conveniences

- Separate emergency liquidity from investment leverage

- Assume the worst-case before hoping for the best

How I Help Clients Navigate HELOCs—Beyond Approval

My job isn’t to push HELOCs. It’s to interrogate fit.

I help clients:

- Compare HELOC structures across lenders

- Understand freeze risk, pricing risk, and exit risk

- Model rate shocks and market downturns

- Decide whether flexibility or constraint suits them better

- Avoid products that look cheap but behave expensively

Sometimes the right answer is a HELOC.

Sometimes it’s a smaller one.

Sometimes it’s none at all.

Good advice doesn’t maximize borrowing—it minimizes regret.

Allen’s Final Thoughts

A HELOC is not inherently dangerous—but it is deceptively powerful.

It magnifies behaviour.

It exposes weak assumptions.

And it rewards discipline while punishing optimism.

The biggest mistake homeowners make isn’t getting a HELOC.

It’s getting the wrong HELOC, from the wrong lender, for the wrong reasons—while assuming they’re all the same.

They’re not.

If you’re thinking about a HELOC, don’t just ask whether you qualify. Ask whether it actually makes your financial life calmer, sturdier, and more resilient.

And if you’re unsure, that’s not a weakness—that’s wisdom.

That’s where a seasoned mortgage agent earns their value: not by approving the line, but by helping you decide whether it should exist at all.