Mortgages are in some ways a lot like pharmaceuticals. A drug that is good for one person is bad for another. So too is it with mortgages and financial products in general. This is why it is important to work with a licensed professional to discover the mortgage that is best for you.

Readvanceable vs Conventional Mortgage

When to Choose BMO Homeowner ReadiLine

When to Choose Scotiabank STEP

When to Choose TD Home Equity FlexLine

Readvanceable Mortgage Comparison

Top Readvanceable Mortgages

There are three readvanceable mortgages that dominate the Canadian mortgage landscape:

- BMO Homeowner ReadiLine Mortgage

- TD Home Equity FlexLine Mortgage

- Scotiabank STEP Mortgage

Each are readvanceable collateral mortgages. A readvanceable collateral mortgage is a specialized financial product that combines a traditional mortgage with a revolving line of credit secured against your home’s equity.

Unlike a conventional mortgage, which is registered only for the exact loan amount borrowed, a collateral mortgage typically registers for a higher amount, often up to the full value of the home. This feature enables homeowners to conveniently access additional funds as they pay down their mortgage without needing to refinance, reapply, or incur extra legal costs.

Collateral mortgages, however, are not for everyone. Due to their higher registered amounts, they may limit your flexibility when switching lenders, as moving to another financial institution usually involves refinancing, incurring legal fees, and possibly additional administrative steps. Additionally, borrowers may face higher initial legal and administrative costs compared to conventional mortgages.

Readvanceable vs Conventional Mortgage

A readvanceable collateral mortgage is especially suitable if you foresee needing frequent or ongoing access to funds. For example, homeowners who anticipate periodic expenses, such as renovations, tuition costs, investment opportunities, or financial emergencies, will benefit significantly from the flexibility these mortgages provide.

As you pay down your principal, you automatically increase available credit on your secured home equity line, eliminating the hassle and expense of refinancing each time additional borrowing is required. Professionals with variable incomes—such as real estate agents, commission-based workers, or self-employed individuals—can leverage this feature to smooth cash-flow fluctuations.

By contrast, conventional mortgages may be better for homeowners whose primary goal is straightforward: predictable monthly payments, a clear repayment timeline, and the ability to easily switch lenders for better rates at renewal. A conventional mortgage has less flexibility because it doesn’t allow automatic re-borrowing without refinancing or requalifying, but it tends to be simpler to manage, with fewer upfront legal and administrative complexities.

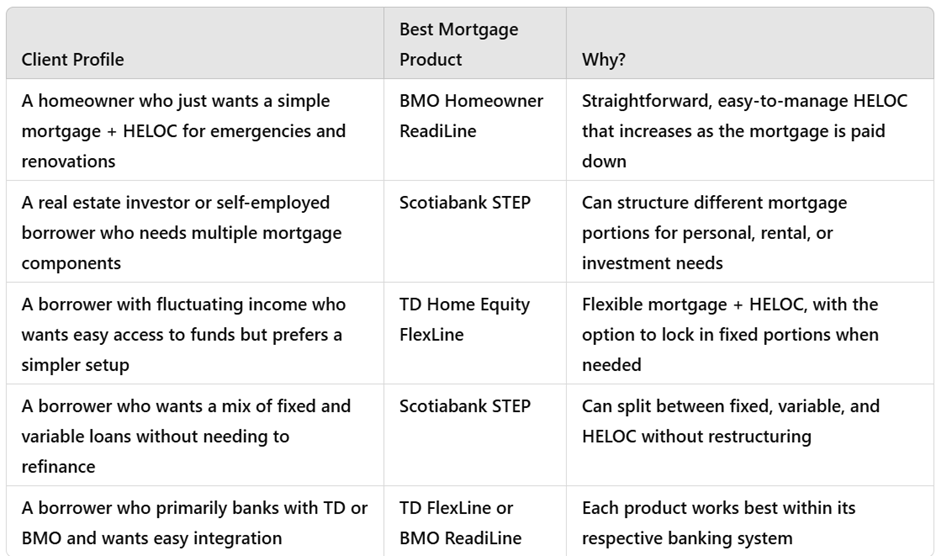

Consider a practical scenario: A homeowner employed as a permanent government worker who values financial predictability but still wants an accessible financial safety net could benefit from a TD Home Equity FlexLine. They get a stable, fixed mortgage alongside a straightforward HELOC to handle occasional or emergency expenses.

On the other hand, a self-employed individual or a real estate investor would find the Scotiabank STEP or BMO ReadiLine more advantageous, as these products offer multiple loan segments, including fixed-rate, variable-rate, and HELOC portions, to better manage diverse financial activities.

Choose a readvanceable collateral mortgage if your priority is financial flexibility, investment strategy implementation, and ongoing access to equity without refinancing. Alternatively, if your goal is simplicity, lower administrative complexity, and ease in switching lenders, a conventional mortgage would be the better choice. Understanding these differences and aligning them with your personal circumstances will guide you to the best mortgage solution.

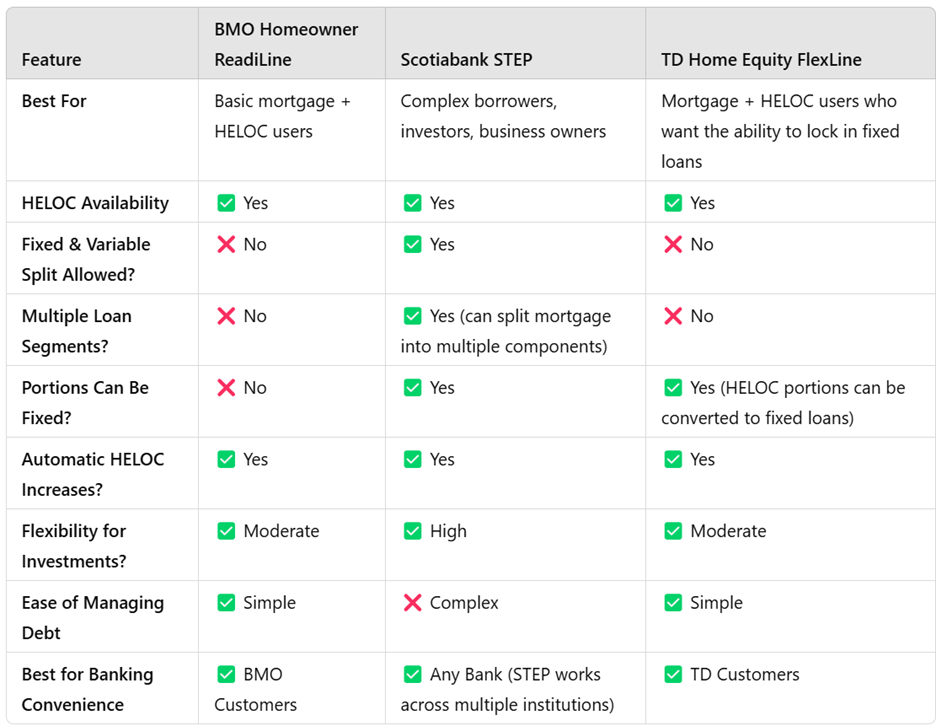

When to Choose BMO Homeowner ReadiLine

Best for: Clients who want a simple readvanceable mortgage with a focus on easy access to home equity, straightforward banking, and competitive HELOC rates.

- Clients who bank with BMO – If they already hold BMO accounts and want seamless account integration.

- Want a basic readvanceable mortgage without extra complexities – The HELOC increases as the mortgage is paid down, providing ongoing access to equity without needing to reapply.

- Flexible repayment options – Allows interest-only payments on the HELOC.

- Good for home renovations, investments, or emergency funds – HELOC funds can be used anytime.

- Ideal for clients who don’t need multiple segmented loan components – Unlike STEP, it doesn’t offer the ability to have multiple fixed/variable mortgage portions under one plan.

Best Fit: Homeowners who want a simple, flexible HELOC alongside their mortgage and don’t need multiple mortgage components.

Less ideal for: Investors or borrowers who need multiple mortgage segments for different purposes.

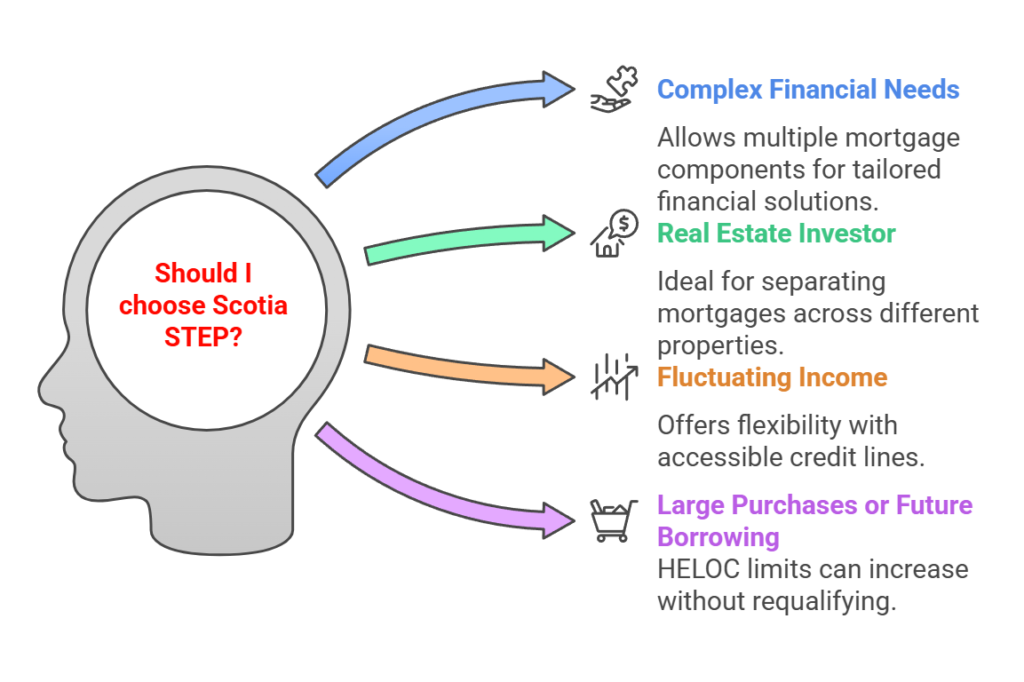

When to Choose Scotiabank STEP

Best for: Clients who want the most flexibility with multiple loan components, investment opportunities, and strategic borrowing.

- Clients with complex financial needs – STEP allows multiple mortgage components, meaning part can be fixed, part variable, and part HELOC.

- Real estate investors – Great for rental property owners who want to separate mortgages for different properties or investment segments.

- Clients with fluctuating income – Since multiple borrowing components are possible, they can separate personal vs. business vs. investment loans easily.

- Entrepreneurs or self-employed borrowers – A HELOC provides an accessible credit line during slower income months.

- Clients planning large purchases or future borrowing – Borrowers can increase their HELOC limit automatically as they pay down the mortgage, without requalifying.

Best Fit: Clients who need a highly customizable mortgage and HELOC structure that adjusts as their financial needs evolve.

Less ideal for: Those who just need a basic mortgage + HELOC without multiple segments (BMO ReadiLine or TD FlexLine would be simpler).

When to Choose TD Home Equity FlexLine

Best for: Clients who want a straightforward HELOC + mortgage setup, with flexibility to switch to fixed-rate loans if needed.

- Clients who bank with TD and want everything in one place – Ideal for TD clients who want easy online access.

- Clients who need both a mortgage and an easy-access HELOC – The HELOC provides liquidity for renovations, emergencies, or large expenses.

- Borrowers who want flexibility to lock in portions at fixed rates – Unlike BMO, TD FlexLine allows portions of the loan to be converted into fixed-rate term loans if interest rates rise.

- People who want to make interest-only payments on the HELOC – Lower required payments give more cash flow flexibility.

- Clients who want a simple mortgage + HELOC option – Doesn’t allow multiple segmented mortgage components like STEP, making it easier to manage.

Best Fit: Borrowers who need a balance between flexibility and simplicity—good for emergency access but without the need for multiple loan components.

Less ideal for: Real estate investors or those who need multiple mortgage components (STEP is better for that).

Readvanceable Mortgage Comparison

Best Choice By Client Profile

- If you want simple mortgage + HELOC access, select BMO Homeowner ReadiLine or TD FlexLine

- If you need multiple mortgage components (fixed + variable + HELOC), select Scotiabank STEP

- If you want the ability to lock in fixed rates on portions of your HELOC, select TD Home Equity FlexLine

Summary

Mortgages, much like pharmaceuticals, need to be carefully matched to an individual’s unique financial health. What works effectively for one homeowner might not suit another’s financial circumstances or goals. Understanding this concept underscores the importance of consulting a licensed mortgage professional who can guide borrowers towards the best-suited mortgage product.

Ultimately, deciding between these mortgages requires a clear understanding of one’s financial needs and preferences.

Those who prioritize flexibility, anticipate future investments, or have variable income streams will likely find the Scotiabank STEP the most beneficial.

For simplicity and basic equity access, TD FlexLine or BMO ReadiLine mortgages offer suitable, streamlined solutions.

Knowing the subtle distinctions between these products enables homeowners to select the best financial strategy aligned with their long-term financial well-being.