You’ve finally decided—it’s time to buy a home. Maybe you’ve been scrolling through Realtor.ca late at night, dreaming about that perfect place with the big backyard or a condo downtown near your favourite coffee shop. It’s exciting, no doubt. But before you call your best friend’s realtor or start booking showings, let’s hit pause.

The truth is, your first call shouldn’t be to a realtor—it should be to a mortgage agent. Talking to a mortgage agent first is the most strategic move you can make because it sets the entire foundation for your real estate journey. It’s where clarity meets preparation. A mortgage agent helps you understand exactly what you can afford, strengthens your offer with a solid pre-approval, and identifies any issues—like credit challenges or documentation gaps—before they become roadblocks. They help you get your financial house in order: reviewing your credit, managing debt, confirming job stability, ensuring your taxes and paperwork are up to date, and assembling the complete documentation set lenders will expect.

By starting here, you’re not guessing your price range or hoping for approval later—you’re entering the market confident, credible, and ready to compete. Once you’ve worked with a mortgage agent and your finances are fully aligned, that’s when it’s time to connect with a realtor and start looking at homes that genuinely fit your lifestyle and budget. It’s the difference between house-hunting with a dream and house-hunting with a plan.

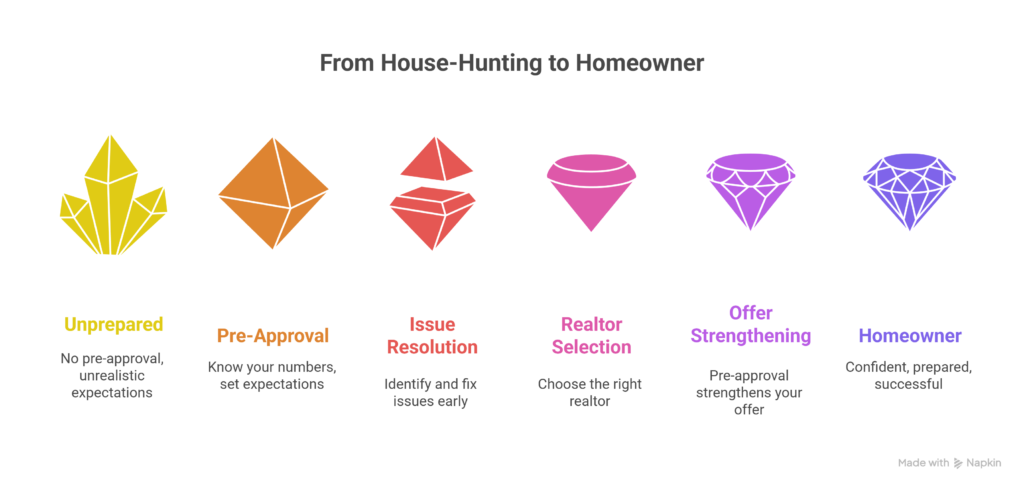

Topics Covered

Why Pre-Approval Comes Before House-Hunting

The Hidden Confidence of Knowing Your Numbers

Setting Realistic Expectations and Avoiding Disappointment

Identifying and Fixing Issues Early

Preparing and Positioning Yourself for Success

The Power of Pre-Approval in Strengthening Your Offer

Choosing the Right Realtor with the Help of Someone Who Knows

How Realtors Benefit When You Talk to a Mortgage Agent First

A Story from the Field: The Offer That Almost Fell Apart

How to Put This Strategy into Practice

Why Pre-Approval Comes Before House-Hunting

Think of mortgage pre-approval as your GPS—it sets your route before you start the drive. Without it, you’re just guessing how far your tank will take you.

When you sit down with a mortgage agent first, you’re not just getting a rate. You’re getting clarity. A pre-approval is essentially a rate hold (usually for up to 120 days) that outlines what you could qualify for based on your income, credit, and down payment. But here’s the key—it’s not a guarantee of final approval. The lender still needs to review the specific property, appraisal, and full documentation before officially approving the mortgage.

That said, a pre-approval is a powerful starting point. It gives you a realistic idea of your budget, helps you understand monthly payments, and locks in a rate while you shop—protecting you from sudden increases. It also identifies potential issues early, giving you time to fix them before you make an offer.

When you know your numbers upfront, everything about the home-buying process becomes easier, faster, and far less stressful.

The Hidden Confidence of Knowing Your Numbers

When you’ve already spoken to a mortgage agent, you don’t just have a number in mind—you have confidence.

But here’s something even more important: knowing what you can buy isn’t the same as knowing what you should buy. A lender might approve you for a certain amount, but that doesn’t mean it fits comfortably into your life. My job as a mortgage agent isn’t just to tell you what the bank says you can borrow—it’s to help you understand what makes sense for your lifestyle, goals, and long-term financial health.

Maybe you want room in your budget for travel, savings, or daycare. Maybe you don’t want to feel the pinch every month just to afford your new home. Together, we’ll look at what payment range feels comfortable for you so your home adds to your life instead of squeezing it. The goal is to help you avoid becoming “house rich and cash poor.”

Imagine walking into an open house knowing your financing is rock solid and your budget feels right. You’re not guessing or hoping—you’re shopping with clarity and confidence. That peace of mind shows in negotiations, and it helps you make choices that feel just as good five years down the road as they do on closing day.

Setting Realistic Expectations and Avoiding Disappointment

Here’s another advantage of knowing your numbers early—it keeps your expectations realistic and your emotions grounded. Too often, buyers start by looking at homes that are outside of what’s comfortable for their budget, only to feel deflated when they realize they can’t afford what they’ve been dreaming about. That kind of disappointment can take the excitement right out of the process.

When you know your real numbers from the start, you can focus on properties that truly fit your financial comfort zone. That means fewer heartbreaks and a lot more confidence in your search. You’ll make decisions that make sense, not ones driven by wishful thinking.

And sometimes, those numbers reveal something important—you might not be ready yet. Maybe it’s smarter to wait a little, build up a bigger down payment, or pay off a small debt before diving in. That’s not a setback—it’s strategy. It’s about making sure that when you do buy, you’re not stretching yourself thin. You’re buying a home that complements your life, not complicates it.

Identifying and Fixing Issues Early

One of the biggest advantages of talking to a mortgage agent first is that it gives you time to spot and solve problems before they become deal-breakers. Maybe your credit score needs a quick boost, or your debt-to-income ratio is a bit too high. Perhaps your income structure — especially if you’re self-employed or earning commissions — needs to be documented differently to satisfy a lender’s requirements.

These are the kinds of things that can derail a deal if discovered after you’ve already made an offer. By starting with a mortgage agent, we can identify those red flags early and develop a plan to fix them. That might mean paying down a credit card, consolidating debt, adjusting your savings strategy, or adding a co-applicant.

This proactive approach ensures that when you do find the right property, you’re not scrambling or panicking. You’re ready. And that preparation gives you — and your realtor — a real advantage in a competitive market.

Preparing and Positioning Yourself for Success

A good mortgage agent doesn’t just find you a rate — they help you get your act together before the lender ever sees your file. That means reviewing every piece of your financial puzzle to make sure it tells the right story.

We’ll take a deep dive into your credit, debts, income stability, job history, and even the way your taxes are filed. We’ll make sure you have a complete documentation set — things like a recent job letter, pay stubs, Notice of Assessment, and proof of down payment — ready to go. This preparation not only speeds up your approval once you find a home, but it also shows lenders you’re organized, reliable, and ready to close.

Think of it as the difference between walking into a job interview unprepared versus walking in with a polished résumé and references in hand. When your file is clean, consistent, and complete, lenders say “yes” faster — and your stress level drops dramatically.

The Power of Pre-Approval in Strengthening Your Offer

A pre-approval doesn’t just give you confidence — it gives your offer power. When sellers see that you’re already pre-approved, they know your financing has been vetted and your offer is serious. In multiple-offer situations, that’s often the deciding factor between winning and losing a bid.

Pre-approval also allows you to move quickly when you find the right home. You can submit offers without hesitation, shorten or even remove financing conditions when appropriate, and show sellers that you’re not just interested — you’re ready. It tells them that your deal is solid, your financing is real, and your closing is secure.

When your mortgage agent, realtor, and lender are already aligned, it’s like having a well-oiled machine behind you. Your offer doesn’t just stand out — it stands strong.

Choosing the Right Realtor with the Help of Someone Who Knows

Once your financing is solid and your pre-approval is in place, the next step is choosing the right real estate agent—and this is where I can add real value beyond the mortgage. There are thousands of realtors out there, but the reality is that roughly 90% of transactions are handled by about 10% of agents. The challenge for most buyers is knowing who’s actually good and who just has a nice Instagram feed. I know the difference—because I work with realtors every single day. I see who negotiates well, who understands financing, who communicates properly, and who actually closes deals in competitive markets. Based on your needs, price range, and location, I can introduce you to a short list of proven agents from strong brokerages and let you decide who’s the best fit.

If you’re early in the process or want to be sure you’re building the right team from day one, booking a quick call with me is a simple way to get clarity. We’ll review where you stand financially, talk through what kind of realtor would best serve your goals, and make sure you’re set up properly before you start viewing homes.

How Realtors Benefit When You Talk to a Mortgage Agent First

Here’s a secret every good realtor will admit—working with pre-approved clients makes their life so much easier.

Realtors are business professionals, and their most valuable resource is time. They only want to spend that time with qualified buyers—people who are financially ready, committed, and capable of completing a purchase. A pre-approval separates the “just looking” crowd from serious buyers. When you’ve already met with a mortgage agent and know your budget, a realtor can focus their efforts on properties that truly fit your price range.

It’s not just about saving time—it’s about building trust and momentum. Realtors can negotiate with confidence, knowing their client’s financing won’t fall apart mid-deal. And when the mortgage agent and realtor work together from the start, they can craft stronger offers, close faster, and deliver a smoother experience for everyone involved.

For realtors, it means fewer wasted showings, more successful transactions, and happier clients who refer others. For buyers, it means your agent is working at full capacity for you—not guessing whether you can afford the homes you’re viewing.

A Story from the Field: The Offer That Almost Fell Apart

A few months ago, a young couple—let’s call them Jamie and Alex—called me in a panic. They’d fallen in love with a home, made an offer, and the seller accepted. But they hadn’t spoken to a mortgage agent yet.

When we reviewed their situation, we realized one of their income sources was commission-based, and their debt ratios were too tight for the lender they’d assumed would approve them. We scrambled for alternatives, and while we found a solution, they nearly lost the home—and a chunk of their deposit—because they didn’t get pre-approved first.

If they’d talked to me before making that offer, we could have structured their file properly, adjusted the down payment, and avoided days of anxiety. It was a happy ending, but it didn’t need to be such a rollercoaster.

How to Put This Strategy into Practice

Here’s how clients and realtors can make this simple but powerful shift:

For Homebuyers:

- Talk to a mortgage agent before you search Realtor.ca or book showings.

- Gather your key documents—income statements, T4s, recent pay stubs, and bank statements.

- Get a clear pre-approval so you know your buying limit and what your monthly payments will look like.

- Ask your mortgage agent about programs like the First Home Savings Account or RRSP Home Buyers’ Plan.

For Realtors:

- Encourage clients to speak with a trusted mortgage agent early in the process.

- Partner with a mortgage professional who can deliver fast pre-approvals and problem-solve tricky cases.

- Use joint marketing—like webinars or info sheets—to educate clients about the “finance first” approach.

When everyone’s aligned, transactions close faster and clients feel supported from day one.

Allen’s Final Thoughts

Buying your first home is one of life’s biggest milestones—but it’s also one of the most complex financial decisions you’ll ever make. Starting with a mortgage agent sets the tone for everything that follows. It’s not just about getting a rate—it’s about getting a roadmap.

By talking to a mortgage agent first, you save yourself from stress, guesswork, and heartbreak. You move forward with confidence, knowing exactly what you can afford and how to make your dream home a reality—without sacrificing the rest of your financial life.

And here’s the good news: I’m here to help you every step of the way. Whether you’re a first-time buyer, a realtor looking to streamline your process, or just someone curious about where to start—I can help you understand your options, get pre-approved, and plan strategically for success.

Let’s talk before you start house-hunting. It’s the smartest first move you can make.