… The Quiet Escape Hatch from a Collateral Mortgage

Here’s an uncomfortable truth that comes up again and again in my practice: many homeowners have a collateral mortgage and don’t even know it.

They didn’t choose it. They weren’t walked through the implications. They just signed where they were told to sign—often at a bank branch—assuming a mortgage is a mortgage. Years later, at renewal or when life changes, they discover their mortgage is structured very differently than they thought… and that difference suddenly matters. A lot.

Allow me to pull back the curtain. You’ll learn what a collateral mortgage is, how it differs from a standard mortgage, why banks default to them, how mortgage penalties quietly reinforce borrower lock-in, and how collateral transfer programs can sometimes provide a clean, strategic exit—without unnecessary cost or friction.

Topics I’ll Uncover in This Article

Why You Want to Transfer Your Mortgage

Many Clients Never Chose to Go Collateral

Who Sells Collateral Mortgages by Default—And Why

What a Mortgage Transfer Is and Why Borrowers Want One

Why Collateral Mortgages Complicate Transfers

Mortgage Penalties: Why Banks Charge More Than Monoline Lenders

How Penalties Reinforce Borrower Lock-In

What a Collateral Transfer Program Actually Does

Which Lenders Offer Collateral Transfer Programs

A Story That Ties It All Together

How Realtors and Clients Can Put This Knowledge to Work

Why You Want to Transfer Your Mortgage

Most clients consider transferring their mortgage when they realize their current loan no longer serves them—not because they planned to leave, but because circumstances changed. Often it starts with something simple, like rates improving at renewal. But very quickly the conversation deepens. Clients discover their mortgage structure is rigid, their penalties are higher than expected, or their lender offers little flexibility if life doesn’t go exactly as planned. A transfer becomes a way to regain control—lowering interest costs, improving cash flow, and moving into a mortgage that’s designed to work with them rather than against them.

For many, a transfer is also about risk management. Life events like selling earlier than expected, upsizing, downsizing, separation, or refinancing plans expose the true cost of penalties and restrictive terms. Clients aren’t looking to break their mortgage—but they want the freedom to do so if needed without being financially punished. Transferring to a lender with transparent penalties, better features, and a cleaner structure is often the only opportunity to fix a mortgage they didn’t fully understand when they first signed.

You may want to transfer your mortgage:

- To secure a lower interest rate at renewal

- To reduce monthly payments or shorten the amortization

- To move out of a rigid or lender-friendly mortgage structure

- To escape a collateral mortgage that limits flexibility

- To reduce exposure to high or unpredictable mortgage penalties

- To move to a lender with clearer, more transparent penalty calculations

- To improve mortgage features such as prepayment privileges or portability

- To simplify future renewals, refinances, or exits

- To correct a mortgage choice they didn’t fully understand at signing

- To align the mortgage with changing life plans such as selling, upsizing, downsizing, or separation

Many Clients Never Chose to Go Collateral

Most clients I meet didn’t choose a collateral mortgage. They discovered it later—usually when something went wrong.

At the bank, the conversation sounded like this:

“Here’s your mortgage approval.”

“Here’s your rate.”

“Sign here so we can also give you flexibility later.”

What rarely gets explained is that the mortgage being registered is not a standard mortgage at all—it’s a collateral charge, often registered for far more than the amount borrowed, and designed to lock multiple credit products under one legal umbrella.

You don’t feel this on day one.

You feel it when you try to leave.

What Is a Collateral Mortgage

A collateral mortgage is a mortgage registered on title as a collateral charge, rather than a traditional (standard) charge.

In practical terms:

A standard mortgage:

- Is registered for the exact loan amount

- Secures one specific mortgage loan

- Is relatively easy to discharge or transfer

A collateral mortgage:

- Is often registered for more than the loan balance

- Can secure multiple current or future debts

- Gives the lender far broader legal control over the property

Collateral mortgages are commonly paired with HELOCs, credit cards, or other lending products—but even borrowers with no HELOC can still have a collateral charge on title.

There is nothing inherently wrong with a collateral mortgage and for many clients it is the most suitable product. The problem is that for many others, it is not the most suitable product, and that’s when problems arise. There is so much more to a mortgage than just the rate.

Collateral Mortgage Vs Standard Mortgage: Why the Difference Matters

The difference rarely matters while everything is calm.

It matters when:

- You want to switch lenders

- You need to refinance

- You sell before maturity

- You separate or restructure debt

A standard mortgage keeps exit paths clean.

A collateral mortgage adds friction, cost, and negotiation power—for the lender.

On paper, transferring a standard mortgage and a collateral mortgage can look similar. The cost difference often isn’t visible until you’re deep into the process.

A standard mortgage transfer is usually straightforward—many lenders cover basic legal fees, discharge costs are modest, and the transaction stays contained.

A collateral mortgage, on the other hand, often triggers additional legal work, higher discharge fees, and, in many cases, a forced refinance instead of a true transfer. That’s where costs quietly balloon. What should have been a clean switch can turn into thousands of dollars in legal fees, penalties, and lost negotiating power. This isn’t because the borrower did something wrong—it’s because the mortgage was structured in a way that made leaving expensive.

Who sells collateral mortgages by default—and why

In Canada, collateral mortgages are most commonly issued—by default—by the major banks, including RBC, TD Canada Trust, Scotiabank, BMO, and CIBC.

Banks prefer collateral mortgages because they:

- Make it easier to cross-sell credit

- Reduce borrower mobility

- Strengthen the bank’s position on title

- Increase lifetime client profitability

From a business standpoint, it’s efficient. From a consumer standpoint, it’s rarely transparent.

What a mortgage transfer is—and why borrowers want one

A mortgage transfer (or switch) is when you move your mortgage to a new lender:

- Without increasing the loan balance

- Usually at renewal

- To improve rate, product features, or service

With a standard mortgage, this is routine.

With a collateral mortgage, it often becomes expensive or impossible without refinancing.

Why collateral mortgages complicate transfers

Most lenders are reluctant to accept another lender’s collateral charge because:

- The registered amount may be excessive

- The legal language is extremely broad

- Risk exposure is harder to isolate

When a transfer fails, the borrower is forced into a refinance, which means:

- Full discharge

- New registration

- Legal fees

- Re-qualification under current rules

And that’s when mortgage penalties hit hardest.

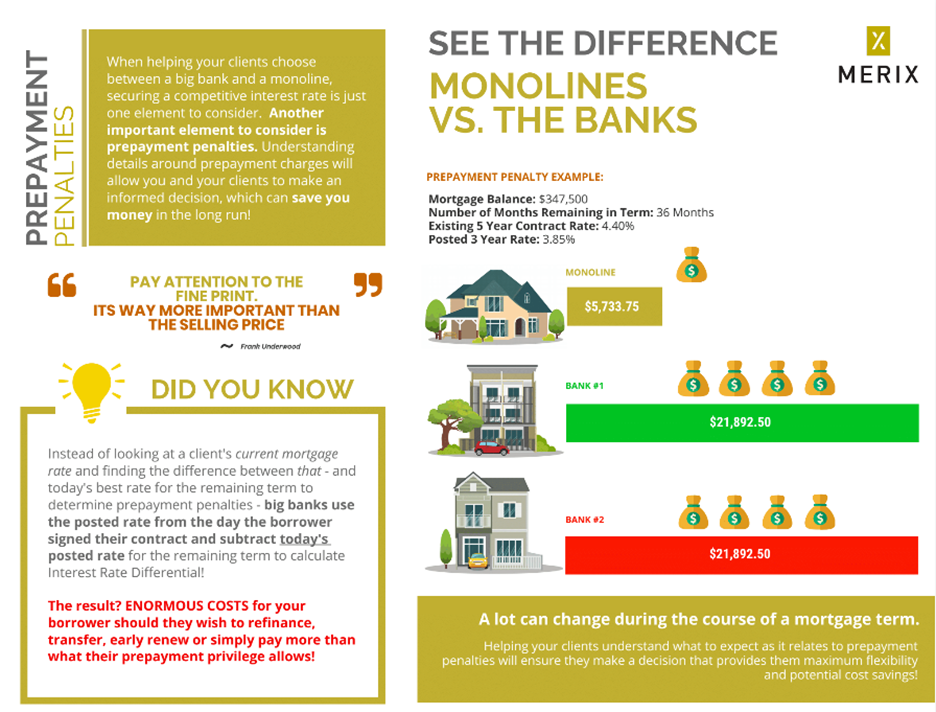

Mortgage penalties: where banks and monoline lenders diverge

Mortgage penalties are the silent enforcer of borrower lock-in—and banks and monoline lenders play very different games here.

Banks typically calculate penalties using:

- Inflated posted rates

- Interest rate differentials that exaggerate losses

- Complex formulas that favour the lender

It’s not unusual for a bank penalty to reach five figures, even when rates haven’t moved much.

Monoline lenders—such as First National Financial LP, MCAP, and RMG Mortgages—generally use:

- Contract-rate comparisons

- Transparent IRD calculations

- Predictable, materially lower penalties

Same borrower. Same balance. Completely different outcome.

How penalties reinforce borrower lock-in

Combine:

- A collateral mortgage that’s hard to move

- With a punitive bank penalty

And you’ve built a system where borrowers don’t choose to stay—they feel forced to stay.

Even when better options exist, the exit cost alone kills the move.

That’s not accidental. It’s structural.

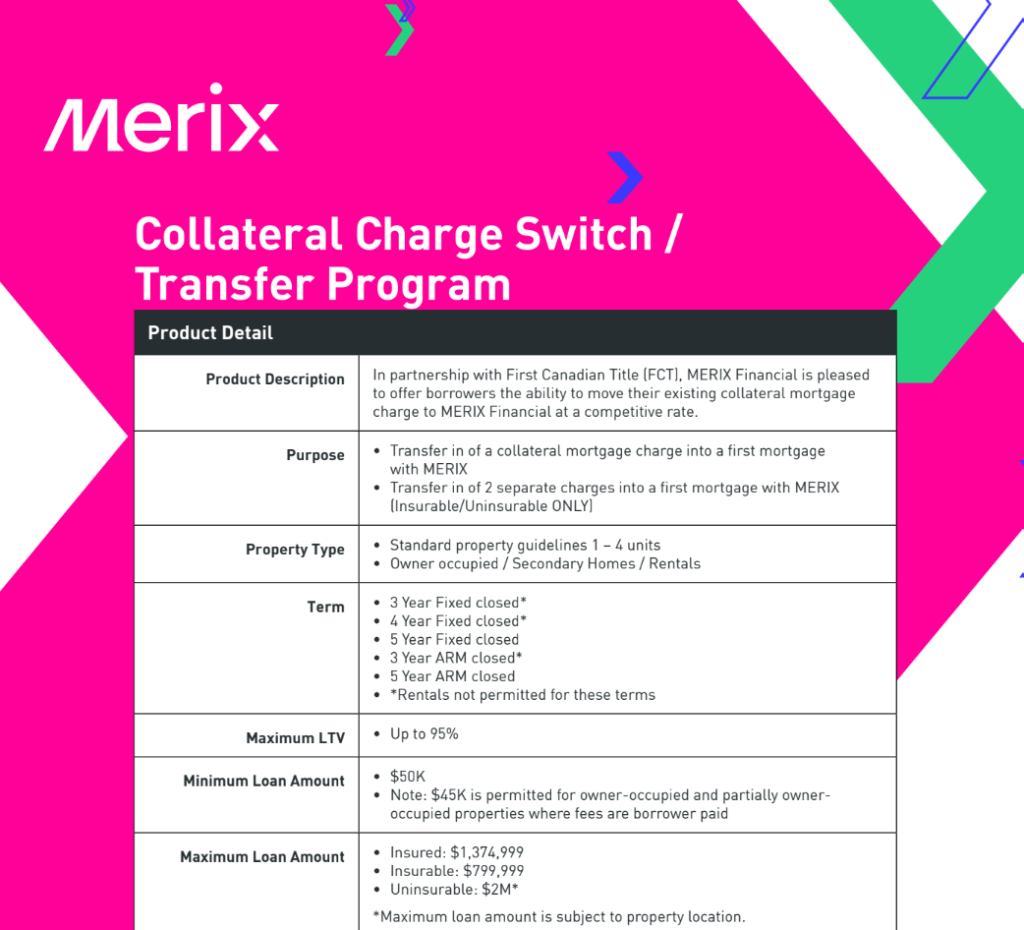

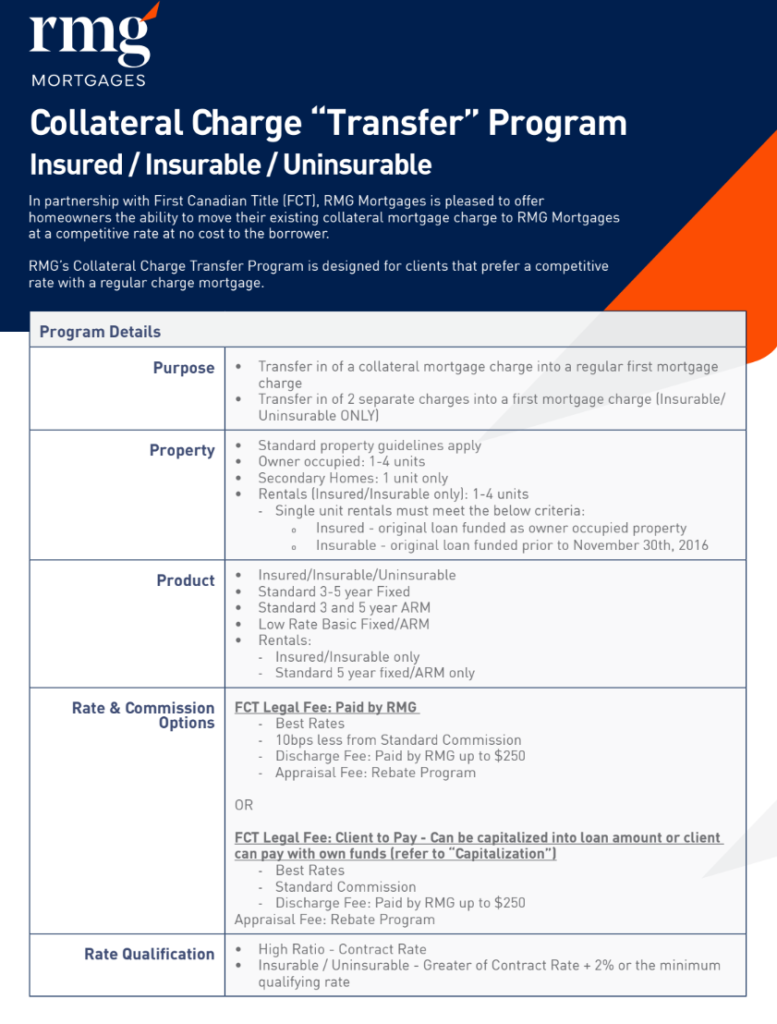

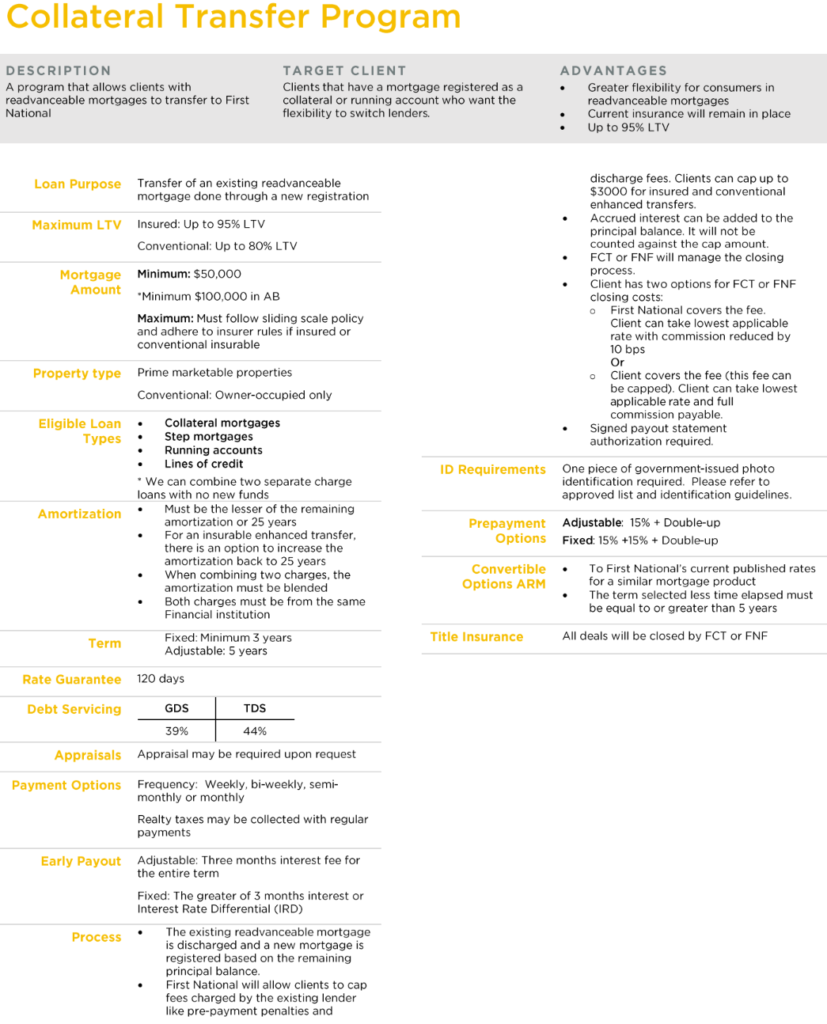

What a collateral transfer program does

A collateral transfer program allows a new lender to take assignment of the existing collateral charge, instead of forcing a discharge.

In effect:

- The charge stays on title

- The lender changes

- The mortgage is truly transferred, not refinanced

- Legal cost and penalty exposure may be reduced

These programs exist specifically to counteract the lock-in created by collateral mortgages.

Who offers collateral transfer programs

Collateral transfer programs are lender-specific and policy-driven. Historically, certain broker-channel monoline lenders have supported them, including First National Financial LP, MCAP, MERIX,and RMG Mortgages.

They typically require:

- No increase in loan amount

- No title or borrower changes

- Clean credit and property

- Acceptable originating charge language

This must be confirmed early. Assumptions are costly.

A short story from the real world

A homeowner comes to me at renewal expecting options.

Then the surprises:

- Their mortgage is collateral

- The charge is registered far above the balance

- The bank penalty wipes out any rate savings

They feel blindsided—and frankly, a little angry.

A collateral transfer program, paired with a lender using fair penalties, changes the math entirely. Same balance. New lender. No refinance. No shock costs.

That outcome didn’t come from luck. It came from understanding structure.

How realtors and clients can put this into practice

For clients:

- Ask whether your mortgage is standard or collateral

- Ask how penalties are calculated

- Don’t assume flexibility just because the rate looks good

For realtors:

- Flag collateral mortgages early in move-up or downsizing plans

- Understand how penalties and structure affect deal viability

- Bring a mortgage agent in before firm dates are set

Financing structure can quietly make—or break—a transaction.

Allen’s Final Thoughts

Collateral transfer programs exist because many borrowers were never told or explained what kind of mortgage they had or the implications of such. When combined with high bank penalties, collateral mortgages quietly strip flexibility away at the exact moment people need it most.

My role as a mortgage agent isn’t just to find a competitive rate. It’s to:

- Explain structure before it becomes a problem

- Anticipate penalties and exit costs

- Preserve options you didn’t know you were giving up

- Advocate for outcomes that make sense long-term

If you have a mortgage—or are about to sign one—this is precisely the kind of nuance that separates confidence from costly surprise. And it’s where having a professional in your corner truly matters.