… When It’s Time to Consider an Alternative Lender

If you work in a commission-based profession, you already know that income doesn’t always arrive in neat, predictable paycheques. One month can feel like a windfall, and the next might feel a little quieter. That’s simply the nature of the beast when your income is tied to performance.

The challenge arises when you apply for a mortgage. Prime lenders—banks and major institutional lenders—want to see stability and predictability in your income. They want to see a consistent income history and clear documentation that proves your earnings are reliable.

But here’s the thing: just because your income is commission-based doesn’t mean you can’t qualify for a mortgage. In fact, some commission earners qualify with prime lenders every day.

The real question is when a commission income borrower should consider an alternative lender instead of trying to force a file into prime lending guidelines that simply don’t fit the situation.

Before we dive deeper, here are the key situations where alternative lending often becomes the right solution.

Topics I’ll Cover in This Article

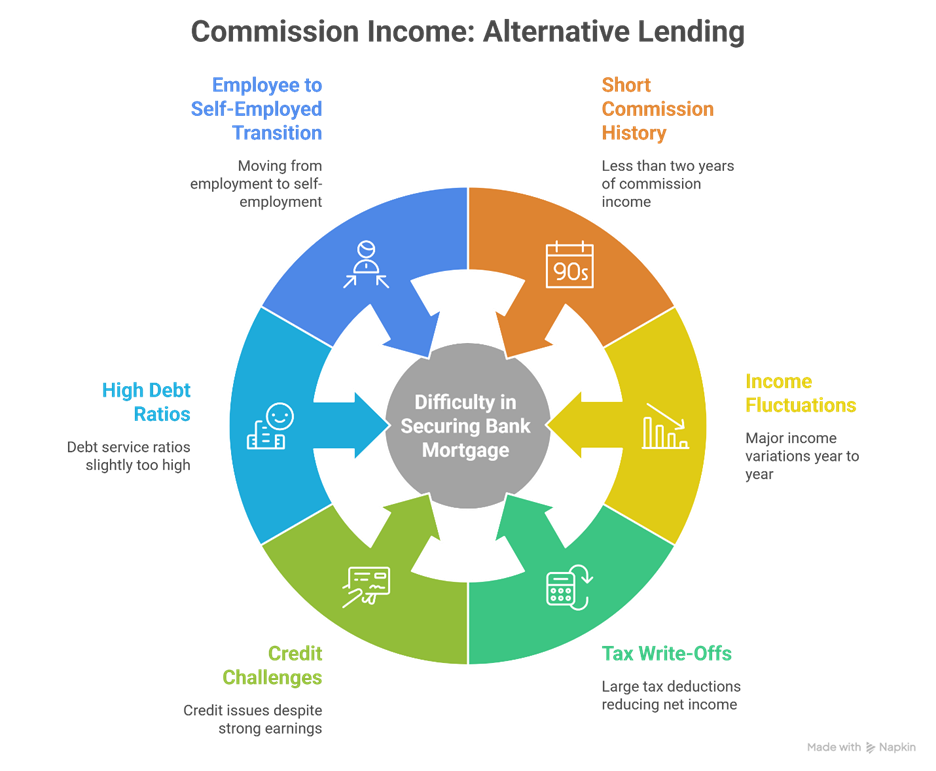

Less Than Two Years of Commission Income

Major Income Fluctuations from Year to Year

Large Tax Write-Offs Reducing Net Income

Credit Challenges Despite Strong Earnings

Debt Service Ratios That Are Just a Bit Too High

Transitioning from Employee to Self-Employed

Alternative Lenders Explained

If you’ve ever been told by a bank that your mortgage application doesn’t quite fit their guidelines, you might have heard the term “alternative lender.” For many borrowers—especially those with commission income—that phrase can sound a little mysterious.

But alternative lending is simply another segment of the mortgage market designed to help borrowers who are financially strong but don’t fit neatly into traditional bank rules.

What Is an Alternative Lender?

Alternative lenders are financial institutions that specialize in flexible underwriting.

They serve borrowers who are strong candidates, but whose financial profiles fall slightly outside traditional bank rules.

These lenders often help borrowers who have:

- commission income with shorter history

- self-employment income

- high tax deductions

- credit challenges

- slightly higher debt ratios

Alternative lenders typically charge slightly higher interest rates than prime lenders because they accept a higher level of underwriting risk. There may also be lender and broker fees to compensate for the additional underwriting and work that needs to be done to get these files approved.

However, they provide a critical bridge that allows many borrowers to purchase or refinance property when prime lending guidelines don’t fit.

The Difference Between Light Prime and Heavy Prime

Within the alternative lending category, there is actually a spectrum. I often describe this spectrum using the terms light alternative and heavy alternative.

These aren’t official regulatory terms—they’re just shorthand I use to describe how strict or open for negotiation a lender’s underwriting policies are.

Light Alternative

Light alternative lenders operate very close to traditional bank standards but allow slightly more flexibility.

They still expect:

- good credit

- documented income

- reasonable debt ratios

But they may be more accommodating when a file has minor complexities.

For example, a light prime lender might accept:

- small income fluctuations

- a recent job change within the same industry

- commission income with strong year-to-date earnings

These lenders often compete aggressively on pricing while offering underwriting flexibility.

Heavy Alternative

Heavy alternative lending is designed for borrowers whose financial profiles are further outside traditional lending guidelines.

These borrowers may have multiple complexities in their file.

Examples might include:

- lower credit scores

- recent credit issues

- significant tax write-offs reducing net income

- higher debt ratios

- short employment, business, or commission history

In these cases, lenders focus more heavily on property equity and borrower capacity rather than strict income formulas.

Interest rates in this category are typically higher than light alternative lending because the lender is accepting greater risk. There are also lender and brokerage fees.

But the key advantage is that these lenders are willing to look at the entire story, not just a rigid checklist of underwriting rules.

How Borrowers Move Between Lending Categories

One of the biggest misconceptions about alternative lending is that it’s permanent.

In reality, it’s often part of a longer-term mortgage strategy.

Many borrowers start in the alternative lending space and later transition to prime lenders once their financial profile improves, if it makes sense for them to do so.

For example, a borrower might begin with a heavy alternative mortgage due to credit issues or short income history.

Over the next couple of years they may:

- rebuild their credit

- establish a longer, better income history

- reduce outstanding debts

At renewal or refinance, that borrower may qualify for light alternative—or even prime lending.

What This Means for Borrowers

The mortgage world isn’t a single lane highway—it’s more like a network of roads that lead to the same destination.

Prime lenders, light alternative lenders, and heavy alternative lenders all serve different purposes in the Canadian mortgage market.

Let’s talk to determine where you fit on that spectrum and I can help you to make smarter financing decisions and avoid unnecessary frustration when a bank’s guidelines don’t line up with your financial situation.

Less Than Two Years of Commission Income

One of the most common hurdles for commission earners is the two-year income history requirement.

Most prime lenders want to see two full years of commission income documented through tax returns and Notices of Assessment. If you’ve only been earning commission income for a year—or even 18 months—the lender may view your income as unproven.

This happens frequently with professionals like realtors.

Imagine you left a salaried job to become a realtor and your first full year of commissions came in at $120,000. That’s fantastic income—but a prime lender might still hesitate because they don’t have a two-year track record to rely on.

An alternative lender can step in here. They may consider one year of strong income plus your industry background.

For example, if you spent ten years in sales before becoming a realtor, an alternative lender may be comfortable recognizing that your ability to generate income didn’t just appear overnight.

Major Income Fluctuations from Year to Year

Commission income can be a bit of a roller coaster. Real estate markets shift, sales cycles vary, and sometimes the timing of deals creates large swings in annual income.

Prime lenders pay close attention to these fluctuations.

Suppose your income looks like this:

- Year one: $145,000

- Year two: $82,000

Even though $82,000 is still solid income, a prime lender may focus on the downward trend and choose to qualify you using the lower figure.

In some cases, they may even decline the application if they believe the income is unstable.

Alternative lenders tend to look at the bigger picture. They may consider things like:

- current year sales activity

- year-to-date commission statements

- market conditions in your industry

In other words, they’re often willing to recognize that commission income doesn’t always follow a straight line.

Large Tax Write-Offs Reducing Net Income

Here’s something many commission professionals learn the hard way.

When you file your taxes, your accountant helps you claim legitimate business expenses. Those deductions reduce your taxable income—and that’s great for tax savings.

But mortgage underwriting looks at things differently.

Prime lenders often rely on the net income shown on your tax return, not the gross commissions you earned.

Let’s say your commission income looks like this:

- Gross commissions: $160,000

- Business expenses: $55,000

- Net income on tax return: $105,000

From the lender’s perspective, you earn $105,000—not $160,000.

Alternative lenders may be more flexible in reviewing gross income trends and expense structures, particularly when those expenses are necessary for earning commissions.

Credit Challenges Despite Strong Earnings

Sometimes income isn’t the issue at all.

Commission professionals often invest heavily in their businesses—marketing, advertising, staging, transportation—and those expenses can sometimes lead to higher credit utilization or missed payments during slower periods.

Prime lenders generally require stronger credit profiles.

If your credit report shows:

- recent late payments

- collections or charge-offs

- high credit card balances

then even a strong income may not overcome those issues.

Alternative lenders are designed for situations exactly like this. They’re willing to look at the entire financial picture, including:

- income potential

- property equity

- long-term career stability

Debt Service Ratios That Are Just a Bit Too High

Debt service ratios are the mathematical guardrails of mortgage underwriting.

Prime lenders typically want to see ratios roughly around:

- Gross Debt Service (GDS) near 39 percent

- Total Debt Service (TDS) near 44 percent

If commission income is averaged down or reduced due to expenses, those ratios can creep up quickly.

You might be in a situation where you’re only slightly outside the guidelines.

Maybe you’re sitting at a TDS of 46 percent. Not wildly off the mark—just enough to cause a problem.

Alternative lenders often allow more flexibility in these ratios, particularly when the borrower has a solid down payment or significant equity in the property.

Transitioning from Employee to Self-Employed

Another common situation arises when a commission employee transitions into self-employment.

For instance, a realtor might incorporate their business or move from a salaried sales position into independent contracting.

Even if the person has years of experience in the same industry, prime lenders may still classify them as newly self-employed.

And that typically means they want to see two full years of financial statements or tax returns before approving a mortgage.

Alternative lenders may consider shorter histories when the borrower demonstrates strong industry experience and income potential.

A Story from the Field

A few years ago, I worked with a realtor who had built an incredible first year in the business.

Let’s call her Sarah.

Sarah had closed more than a dozen transactions in her first year and earned just over $130,000 in commissions. She had excellent credit and a solid down payment saved.

On paper, she looked like a perfect mortgage candidate.

But when we approached prime lenders, they all came back with the same concern.

“Come back when you have two years of commission income.”

Now, Sarah could have waited another year to buy a home. But the market conditions at the time made waiting less than ideal.

Instead, we structured a mortgage through an alternative lender. The interest rate was slightly higher, but it allowed Sarah to purchase the home she wanted.

Two years later, after establishing a longer income history, we refinanced her mortgage into a prime lender at a lower rate.

That’s the key point many people miss.

Alternative lending can be a bridge—not a destination.

How Realtors and Clients Can Put This Into Practice

If you’re a realtor or commission professional, there are a few practical steps you can take.

First, keep detailed records of your income. Year-to-date production reports and commission statements can be extremely helpful.

Second, speak with a mortgage professional before you start house hunting. Understanding your financing options early can prevent surprises later.

Third, think long term. Sometimes choosing an alternative lender for a short period can open the door to refinancing into a prime lender once your income history strengthens.

For realtors working with clients, this knowledge can be incredibly valuable. If your client earns commission income, connecting them with a mortgage professional early can prevent deals from falling apart at the financing stage.

Allen’s Final Thoughts

Commission income is one of the most misunderstood areas of mortgage underwriting. Too often, people assume that if a bank says no, the dream of homeownership is over.

In reality, that’s rarely the case.

The mortgage market in Canada includes a wide range of lenders, each designed to serve different financial situations. For commission professionals, alternative lenders can provide flexibility when prime guidelines don’t quite fit the story yet.

The important thing is having someone in your corner who understands how to structure these files properly and who knows which lender is the right fit for your situation.

That’s where I come in.

As a mortgage agent, my job isn’t just to find you a mortgage—it’s to help you navigate the entire process. I can help you:

- analyze your commission income structure

- determine whether prime or alternative lending makes the most sense

- prepare the documentation lenders want to see

- build a strategy that moves you toward prime lending over time

If you’re a realtor, a sales professional, or anyone earning commission income and you’re wondering how a lender will view your earnings, let’s talk. Together we can map out a plan that turns your income story into a mortgage approval.

Because when you understand how lenders think, you can turn what looks like a challenge into a workable solution.