When purchasing a property, buyers either pay for the entire property with their existing funds or they need to seek out financing by getting a mortgage. Previous to looking for a home, buyers need to have a relationship with a mortgage agent to create a financial strategy and mortgage plan to form the basis of the home purchase. With a pre-approval from a lender and or an associated rate hold, the buyer can begin to work with a realtor to find a home to purchase. When crafting an offer, it is critical the realtor include a condition of finance in the offer.

What is the Condition of Financing

Wording of the Condition of Financing

Why is the Condition of Financing Important

Steps to Fulfill the Financing Condition

Condition of Financing and The Deposit

What is the Condition of Financing

The condition of financing is a clause often included in real estate purchase agreements to protect the buyer. It allows the buyer a specific period of time (typically 5-7 business days) to secure mortgage financing for the property. If the buyer is unable to obtain financing during this time, they can cancel the agreement without penalty.

When underwriting a mortgage, as part of the transaction document package, the mortgage brokerage and lender will be required to see the waiver of the condition of financing associated with the condition (if present) of the Agreement of Purchase and Sale.

The purpose of the condition of financing is to ensure that the buyer has the mortgage funding to buy the house without being legally obligated to buy the home if they can’t get financing together.

Wording of the Condition of Financing

The typical wordings is:

“This agreement is conditional upon the buyer obtaining financing satisfactory to the buyer in their sole and absolute discretion by [date]. Unless the buyer gives notice in writing delivered to the seller or the seller’s representative confirming that this condition has been fulfilled or waived, this agreement shall become null and void, and all deposit money shall be returned to the buyer.“

To waive the condition of financing, working with their mortgage agent, the buyer receives a mortgage commitment from a lender that says if the borrower meets all the conditions described in the commitment, the lender will provide mortgage funding under the following terms.

Based on this mortgage commitment, buyers through their realtor provide a Notice of Fulfillment to the seller by or before the date stated in the condition of financing waiving the condition.

If the buyer cannot get mortgage financing by the condition date, they can ask the seller for more time or the buyer can terminate the agreement by notifying the seller in writing before the condition expires. The buyer’s deposit is refunded.

It should be noted that the mortgage commitment is not a guarantee of the mortgage being funded by the lender, and should the funding not come through due to a condition not being satisfactorily met by the lender, the buyer will likely lose their deposit and potentially face legal action for damages.

Why It’s Important

The financing condition gives buyers the confidence to proceed with the purchase, knowing they can afford it. It also allows time for the lender to assess both the buyer’s financial situation and the property’s value to ensure it meets the lender’s criteria.

Possible Outcomes

Once a condition of financing is included in the Agreement of Purchase and Sales, several outcomes are possible:

- Condition Fulfilled: The buyer obtains financing and provides a Notice of Fulfillment to the seller.

- Condition Waived: The buyer decides to proceed with the purchase without secured financing (a risky move).

- Condition Not Fulfilled: If the buyer cannot secure financing, they can terminate the agreement by notifying the seller in writing before the condition expires. The buyer’s deposit is refunded.

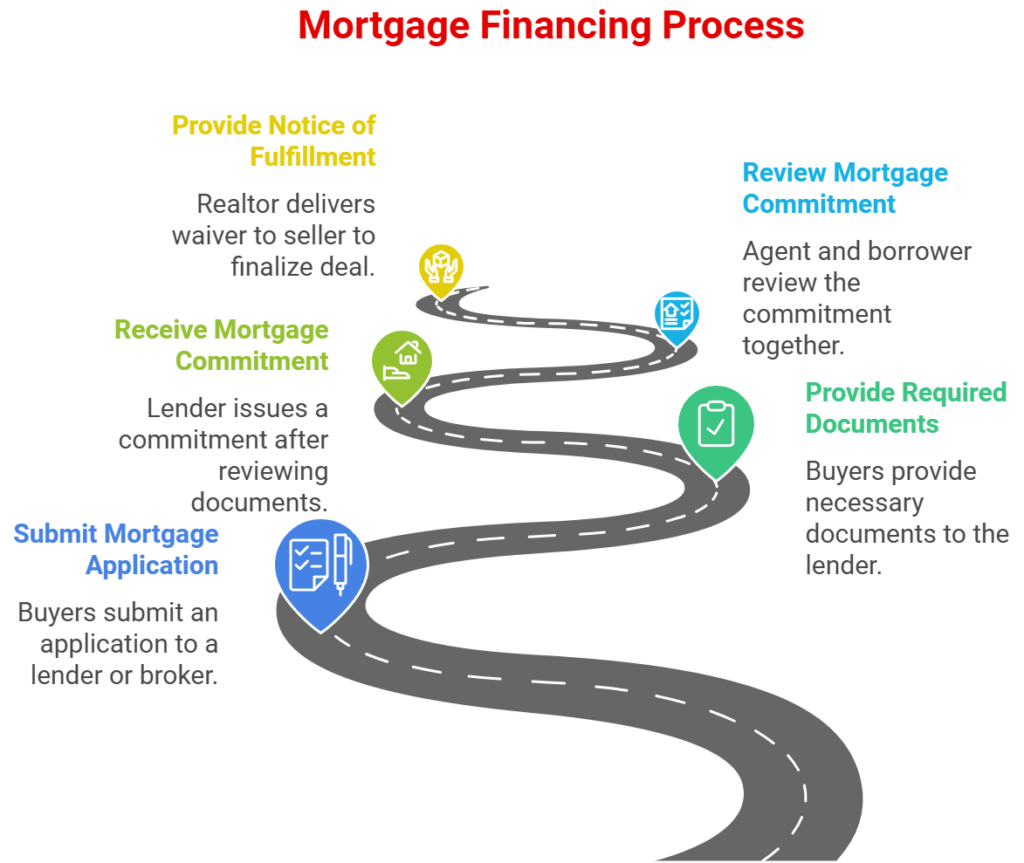

Steps to Fulfill the Financing Condition

Submit a mortgage application to a lender or broker.

Buyers will have a relationship with a mortgage agent previous to beginning their real estate journey. It is likely they have been pre-approved and have obtained a rate hold from their chosen lender.

Provide Required documents (e.g., income verification, credit history, down payment proof, Purchase and Sale Agreement, etc.).

Once buyers have an accepted offer conditional on finance, they provide any documentation required by the lender (usually information about the property itself) to enable the lender to provide the buyer with a mortgage commitment before the condition of financing expires.

Receive a mortgage commitment from the lender specific to the property.

Upon reviewing property information, if the lender is satisfied they will provide the borrower with a mortgage commitment stating the lender will provide a mortgage on the property and stated terms if certain conditions are met.

Review Mortgage Commitment

The mortgage agent reviews the mortgage commitment with the borrower so the borrower understands the conditions they must meet. If the borrower is confident they can meet the lender’s conditions, they sign the mortgage commitment and return it to the lender. This enables the borrower to move to waive the condition of financing.

Provide Notice of Fulfillment to the Seller.

To waive the condition of financing to firm the deal, the buyer’s realtor has the borrower sign and complete the Notice of Fulfillment waiver and deliver the waiver to the seller thereby waiving the condition of financing.

Condition of Financing and The Deposit

If a financing condition is included in the purchase agreement and the buyer cannot secure financing within the conditional period, the buyer is entitled to receive their deposit back.

If the buyer does not waive the conditions and does not notify the seller within the conditional period, the outcome depends on the specific wording of the Agreement of Purchase and Sale (APS). However, in most cases, the agreement becomes null and void once the conditional period expires, meaning neither party is bound to proceed with the transaction.

If the APS includes a clause stating that the agreement is conditional upon the buyer waiving or fulfilling the conditions by a specific date, the agreement will typically become null and void if no action is taken by the deadline.

In this case, the buyer’s deposit is refundable, but both parties will need to sign a mutual release to authorize the return of the deposit from the trust account.

Failure to Notify

If the buyer fails to notify the seller about the fulfillment or non-fulfillment of the conditions, the agreement may still lapse automatically once the conditional period ends, depending on the wording of the agreement.

However, this lack of communication can create confusion or disputes, especially if the seller believes the buyer was acting in bad faith or if the seller continued preparing for closing under the assumption the deal was moving forward.

Seller’s Right to Clarify

If the conditional period lapses without notification, the seller (or their agent) may follow up to confirm the status. If no response is provided, the seller can consider the agreement void and begin relisting the property.

Key Considerations:

- Deposit Release:

Even if the agreement becomes void, the release of the deposit still requires a mutual release form signed by both parties. If the seller refuses to sign the form (e.g., if they believe the buyer acted unfairly), the deposit remains in the brokerage’s trust account until the dispute is resolved—potentially requiring legal intervention. - Good Faith Obligation:

Buyers and sellers are generally expected to act in good faith. If the buyer intentionally ignores the obligation to notify or provide clarity, the seller could claim a lack of good faith and potentially dispute the deposit. - Legal and Practical Risks:

While failing to notify may not automatically penalize the buyer, it can lead to misunderstandings or disputes that delay the deposit refund and affect both parties’ timelines and plans.

Read More:

- Real Estate Conditions

- Financing Condition

- Home Inspection Condition

- Sale of Current Property Condition

- Status Certificate Condition

- Appraisal Condition

Summary

In summary, if the buyer does not waive the conditions and does not notify the seller, the agreement usually becomes null and void upon expiration of the conditional period. However, failing to communicate may lead to disputes or delays in resolving the transaction, especially regarding the release of the deposit.