… How your credit card limit can kill your mortgage application

You’ve done everything right. You pay your bills and your credit cards on time. You don’t miss payments. You might even pay them off every month. So when you start house hunting, it feels reasonable to assume your credit cards are a non-issue especially when you have nothing on balance. On top of that, your credit rating is outstanding!

And yet—somehow—the numbers don’t work the way you expect, and that mortgage application receives rejection after rejection after rejection.

What the heck is going on???

This is one of the most common (and frustrating) surprises I see as a mortgage agent. Simply having credit cards—especially high-limit ones—can quietly erode your ability to buy a home, even if you rarely use them.

Allow me to reveal why.

What I’m going to cover

Why credit cards matter even when you “don’t owe anything”

Capacity beats usage (every single time)

The $1,000 = $5,000 rule of thumb

A story that illustrates the problem

Why reducing limits beats paying balances

My 90 Day Pre-Mortgage Credit Fix

How buyers and realtors can put this into practice

Why credit cards matter even when you “don’t owe anything”

When a lender underwrites a mortgage—especially a major bank—they are not just asking:

“How responsible has this borrower been?”

They are asking:

“What is the maximum financial strain this borrower could face?”

Credit cards represent unsecured borrowing capacity. From the lender’s perspective, that capacity can be used at any time—often at the worst possible moment, like right after you take on a mortgage.

So instead of focusing on how much you owe, lenders focus on how much you could owe.

That distinction changes everything.

Capacity beats usage (every single time)

Here’s the key mental shift:

- Usage = how much of your credit you choose to use

- Capacity = how much credit is available to you

Mortgage underwriting is built on capacity, not behaviour.

That’s why:

- Paying a card down to $0 doesn’t necessarily help

- Keeping a $20,000 limit “just in case” can hurt

- Explaining that you’re disciplined doesn’t change the math

Lenders assume a deemed monthly payment on your available credit, even if you never carry a balance.

The $1,000 = $5,000 rule of thumb

Here’s the simple math I teach clients:

Every $1,000 of unused credit card limit costs roughly $5,000 in mortgage buying power.

Why?

- Lenders typically assume ~3% of the limit as a monthly payment

- That monthly payment eats into your Total Debt Service (TDS)

- Mortgage payments are just another monthly payment competing for space

A quick example

You have:

- A $10,000 credit card

- Another $3,000 credit card

- $13,000 total limit capacity

Lenders assume a monthly debt whether you use it or not:

- $13,000 × 3% ≈ $390/month

That $390/month could otherwise support about:

- $60,000–$70,000 of mortgage (depending on rates and amortization)

All without carrying long-term debt or owing a penny on either card!

A story that illustrates the problem

Let me tell you about “Mark and Sarah” (names changed, but the situation is real).

They’re both professionals. Solid incomes. Great credit scores. They pay their cards off regularly, but they like having flexibility:

- One premium card with a $20,000 limit

- A backup card with a $10,000 limit

They find a home they love—and then hit a wall.

The mortgage amount comes in $150,000 lower than expected. That’s a lot less house that could put them out of the market!

Why?

Not income. Not credit score.

It was the $30,000 of unused unsecured credit quietly soaking up their borrowing room.

Once we reduced limits—without closing their oldest card—the numbers worked. Same people. Same income. Same house. Different structure.

Scale It (What This Looks Like in Real Life)

| Unused Credit Limit | Assumed Monthly Debt | Mortgage Buying Power Lost |

| $1,000 | $30 | ~$5,000 |

| $5,000 | $150 | ~$25,000 |

| $10,000 | $300 | ~$50,000 |

| $15,000 | $450 | ~$75,000 |

| $20,000 | $600 | ~$100,000 |

Why reducing limits beats paying balances

This part feels backwards, so allow me to be blunt.

- Paying balances improves credit scores

- Reducing limits improves mortgage affordability

They solve different problems.

If you pay a $6,000 balance down to $0 on a $20,000 card:

- Your score may improve

- Your mortgage qualification barely moves

If you reduce the limit from $20,000 to $5,000:

- Your assumed payment drops dramatically

- Your buying power increases immediately

From the lender’s point of view:

A zero balance today does not prevent a maxed-out card tomorrow.

My 90 Day Pre-Mortgage Credit Fix

Here is my professional, pre-mortgage credit optimization checklist you can use before going for that pre-approval or home purchase, during refinance planning, or even at renewal. By following this plan, you could add tens of thousands and even more to the mortgage you will qualify for.

Phase 1 — Assess (90+ days before application)

Pull and review both credit bureaus

- Confirm:

- Limits

- Balances

- Account type (credit card, unsecured LOC, loan)

- Old/closed accounts still reporting

- Identify total unsecured credit limits (this is the key number)

Do not start changes before you understand the full picture.

Identify Credit Card exposure

Flag:

- High-limit credit cards

- Unsecured lines of credit

- Redundant or unused cards

Ask:

“If this entire limit were maxed tomorrow, what would the lender assume?”

Phase 2 — Clean Up Balances (75–90 days out)

Pay down revolving balances first

Target:

- Credit cards

- Unsecured LOCs

Goal:

- Get utilization below 30% on each account

- Ideally under 10–20% on cards you plan to keep

!!! Do NOT reduce limits yet if balances remain !!!

Let balances report

- Wait for at least one full statement cycle

- Confirm updated balances appear on credit bureau

This protects your credit score before structural changes.

Phase 3 — Optimize Limits (60–75 days out)

Reduce limits on high-impact accounts

Priority order:

- High-limit, low-use cards

- Premium or backup cards

- Store or co-branded cards

Best action:

- Request a limit reduction, not a closure

Reducing limits:

- Improves mortgage affordability

- Usually causes minimal score impact

Avoid closing your oldest account

Keep:

- Oldest card

- Low limit

- No annual fee

This preserves:

- Credit history length

- Score stability

Consolidate where appropriate

If practical:

- Replace multiple cards with one lower-limit card

- Or convert unsecured exposure to secured (case-by-case)

Phase 4 — Stabilize (30–60 days out)

Freeze credit behaviour

From this point forward:

- No new credit

- No inquiries

- No limit increases

- No product switches

Lenders value stability more than perfection.

Re-pull credit to confirm results

Verify:

- Reduced limits are reporting

- Balances are low

- No surprises remain

This is where you catch issues before underwriting does.

Phase 5 — Final Pre-Submission Check

Calculate affordability with actual lender logic

Confirm:

- Deemed payments on remaining unsecured credit

- TDS impact

- Stress-test alignment

This avoids:

- Last-minute declines

- “Why is the number lower?” conversations

- Re-structuring under pressure

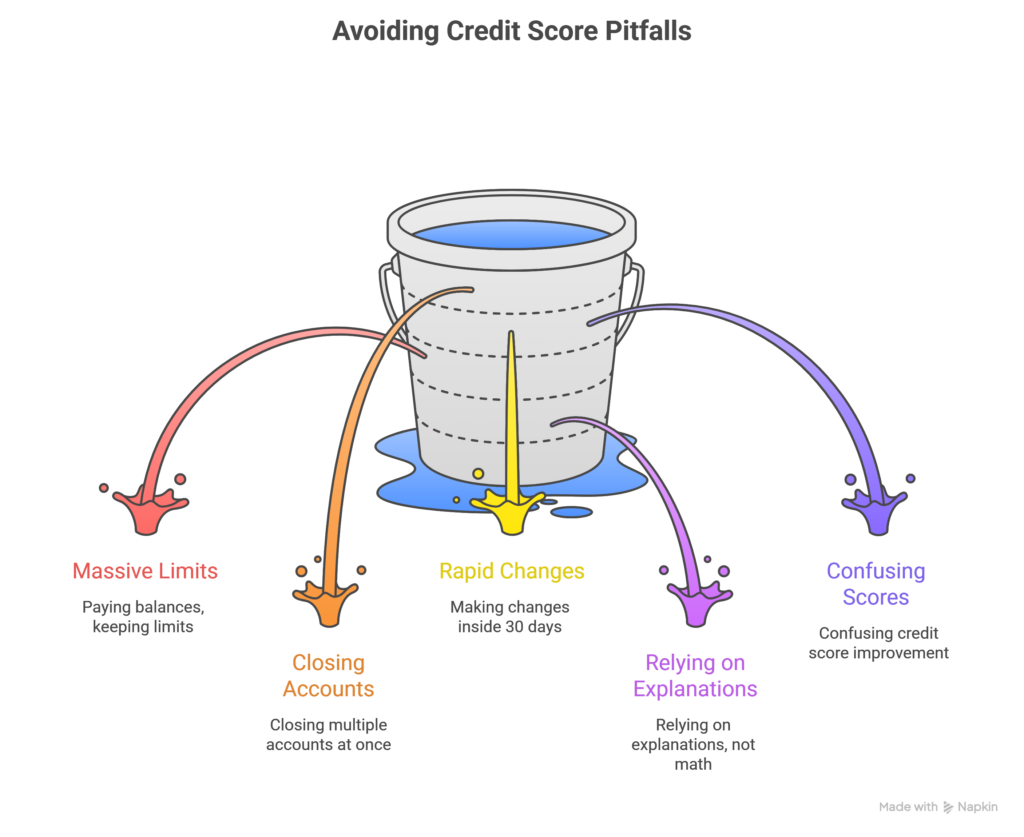

Common Mistakes This Checklist Prevents

- Paying balances but keeping massive limits

- Closing multiple accounts at once

- Making changes inside 30 days

- Relying on explanations instead of math

- Confusing credit score improvement with mortgage optimization

My One-Sentence Explanation

“We’re not fixing your credit score — we’re fixing how lenders model your risk.”

That framing changes everything.

How buyers and realtors can put this into practice

For buyers

- Start reviewing credit 90 days before shopping seriously

- Identify high-limit, low-use cards

- Pay balances down first, then reduce limits

- Avoid big credit changes inside 30 days of application

For realtors

- When affordability feels “tight,” ask about credit limits, not just balances

- Encourage clients to speak with their mortgage agent early

- Use this insight to explain why “great income” sometimes isn’t enough

This knowledge often saves deals—especially in competitive markets where buyers are stretching.

Why this feels so unfair (but isn’t personal)

Borrowers think in terms of:

- Responsibility

- Discipline

- Intentions

Lenders think in terms of:

- Stress scenarios

- Worst-case outcomes

- System-wide risk

Neither is wrong. They’re just playing different games.

Allen’s Final Thoughts

Credit cards aren’t evil. They’re useful tools. But in the context of a mortgage, they’re treated like open taps, not closed doors.

If there’s one takeaway I want you to remember, it’s this:

Mortgages aren’t qualified on how well you’ve behaved—they’re qualified on how much risk exists if things go sideways.

As a mortgage agent, my role isn’t just to find you a rate. It’s to help you understand how lenders see your financial picture, long before an underwriter does. I help clients:

- Optimize credit structure, not just credit scores

- Sequence changes without causing harm

- Translate confusing lender logic into clear, practical steps

If you’re dreaming about buying a home—or moving up to the next one—this is exactly the kind of quiet detail that can make or break the outcome. And it’s the kind of thing I’m here to help you navigate, before it becomes a problem.