…How I Use the Hidden Power of Mortgage Exceptions to Get You a Better Deal

If you spend any time around mortgages in Canada, you’ll hear a lot about guidelines, ratios, and rules. But here’s the reality that rarely gets explained outside underwriting departments: mortgage approval is rarely as rigid as it appears.

Behind every approval—or decline—is a framework called underwriting policy. These policies give lenders structure and consistency. But they also leave room for exceptions, where a skilled mortgage professional can present a file in a way that helps a lender say yes instead of no.

In other words, underwriting is part science and part judgment. And if you know how to work within the system, there’s often more flexibility than most people realize.

Whether you’re a realtor helping clients purchase a home, a financial professional guiding a client’s long-term strategy, or a borrower trying to understand why one lender said no while another said yes, understanding how underwriting exceptions work can change everything.

Topics I’ll Cover in This Article

What Mortgage Underwriting Policies Are

Why Mortgage Policies Exist in the First Place

The Difference Between Policy and Exceptions

How Prime Lenders Handle Exceptions

How Alternative Lenders Use Flexible Underwriting

The Role of Private Lenders in Exception-Based Lending

Why You have to Use Me to Get Your Exceptions

Real-Life Examples of Underwriting Exceptions

The Story of a Deal That Almost Died

How Realtors Can Use This Knowledge

How Financial Professionals Can Apply These Insights

What Borrowers Should Understand About Mortgage Approval

The Value of a Skilled Mortgage Agent in Exception Lending

What Mortgage Underwriting Policies Are

Mortgage underwriting policies are essentially the rulebook lenders use to evaluate risk.

These policies outline things like:

- Maximum Gross Debt Service (GDS) and Total Debt Service (TDS) ratios

- Minimum credit score requirements

- Acceptable income verification methods

- Down payment rules

- Property types allowed

- Employment history requirements

For example, a typical prime lender policy might say:

- Maximum GDS: 39%

- Maximum TDS: 44%

- Minimum credit score: 680

- Two-year employment history preferred

At first glance, these rules look absolute.

But they rarely are.

Most lenders also include something called “exception authority.”

And that’s where things get interesting.

Why Mortgage Policies Exist in the First Place

Policies serve three major purposes.

First, they protect lenders from excessive risk.

Second, they ensure consistency so every borrower is evaluated fairly.

Third, they satisfy regulators and insurers like:

- Office of the Superintendent of Financial Institutions

- Canada Mortgage and Housing Corporation

- Sagen

- Canada Guaranty

These organizations require lenders to maintain prudent lending standards.

But regulators also recognize something important:

Real life rarely fits perfectly inside a spreadsheet.

That’s why policies almost always include room for judgment.

The Difference Between Policy and Exceptions

An exception is when a lender approves a mortgage outside their standard guidelines, because the overall risk still makes sense.

Think of underwriting policies as guardrails.

They keep the car on the road.

But sometimes the driver needs a little room to maneuver.

Examples of common underwriting exceptions include:

- Slightly higher debt ratios

- Shorter employment history

- Non-traditional income sources

- Lower credit scores with strong compensating factors

- Unique property types

What matters most is the total story behind the borrower.

A talented mortgage agent knows how to present that story.

How Prime Lenders Handle Exceptions

Prime lenders—banks and major financial institutions—generally follow the strictest policies.

But even they allow measured flexibility.

For example, a lender might normally cap TDS at 44%.

But they might approve 46% or 47% if the borrower has:

- A high credit score

- Significant savings

- Stable employment

- A strong net worth

Prime lenders often refer to these as “compensating factors.”

Typical examples include:

- Credit score above 760

- Large liquid assets

- Minimal consumer debt

- Long tenure with employer

In these cases, the file may be escalated to a senior underwriter or credit committee.

That’s where the art of mortgage structuring really begins.

How Alternative Lenders Use Flexible Underwriting

Alternative lenders operate with more flexible underwriting frameworks.

Many of these lenders exist specifically to approve borrowers who don’t perfectly fit traditional bank policies.

Examples include:

- Self-employed borrowers

- Commission-based income

- Recently incorporated business owners

- New immigrants to Canada

- Borrowers rebuilding credit

Instead of focusing strictly on ratios, alternative lenders often evaluate:

- Overall financial stability

- Equity in the property

- Borrower behaviour patterns

A borrower who might be declined by a bank due to income complexity could still be approved by an alternative lender with a slightly higher rate.

The key point?

Flexibility increases as you move across the lending spectrum.

The Role of Private Lenders in Exception-Based Lending

Private lending is essentially pure exception lending.

Private lenders are less concerned with income documentation and more focused on:

- Property value

- Loan-to-value ratio

- Exit strategy

For example, a borrower who cannot prove income due to a recent business transition might still qualify for a private mortgage if:

- The property has substantial equity

- There’s a clear refinancing plan

- The borrower has strong assets

Private lending is often used as a temporary bridge, helping borrowers stabilize their financial situation before returning to conventional financing.

Why You Must Use Me to Get Your Exceptions

When a borrower goes directly to a prime lender (like a bank branch), the likelihood of obtaining underwriting exceptions is unlikely than when the file is structured and presented by an experienced mortgage agent like me because their process and incentives are very different.

Let’s unpack why.

Banks Typically Follow the Policy Playbook

When you walk into a bank branch, the person you speak with is usually a mortgage specialist or advisor, not an underwriter.

Their job is largely to:

- Gather the application

- Input the data into the lender’s system

- Submit the file for underwriting

The approval decision is then driven heavily by automated underwriting systems and standard policies.

These systems evaluate things like:

- Debt service ratios

- Credit scores

- Income verification

- Property value

- Loan-to-value ratio

If the numbers fall outside the guidelines, the system often automatically declines the file or flags it for review.

At that point, many branch-originated files simply stop moving forward. Your mortgage is declined.

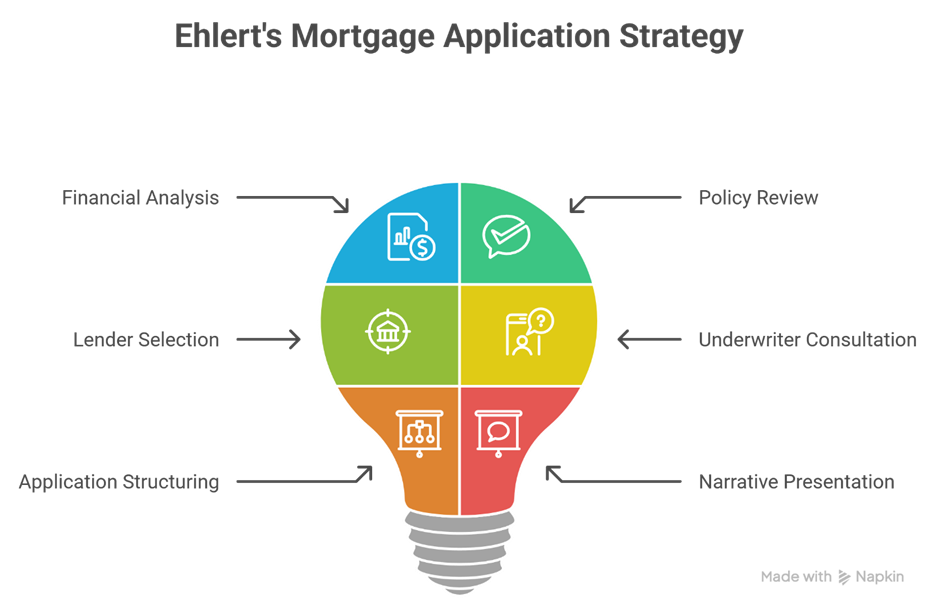

I Build Your File Strategically

As an experienced mortgage agent, I approach the process differently.

Instead of simply entering numbers into a system, I:

Analyze your full financial picture.

Identify potential policy conflicts or weaknesses in the file.

Determine which lenders are most likely to view the risk favourably.

Consult with the country’s best team of mortgage underwriters on difficult files (we have regular underwriting meetings where we collectively review the most difficult files)

Structure the application in a way that highlights compensating strengths.

Present the file with a narrative that helps the underwriter understand the full story.

This difference in presentation and lender selection is where exceptions often happen.

I Know Where Exceptions Actually Happen

Not every lender is equally flexible.

Some prime lenders are known internally for being more comfortable with:

- Slightly higher debt ratios

- Self-employed income complexity

- unique properties

- unconventional income structures

Other lenders are extremely rigid.

Borrowers who go directly to a single bank only see that bank’s policies and appetite for risk.

I on the other hand, have access to dozens of lenders across three categories:

- Prime lenders

- Alternative lenders

- Private lenders

If one lender says no, another may view the same file very differently.

Underwriters Respond to Well-Structured Files

Underwriters evaluate risk, not just ratios.

A well-presented file may highlight things like:

- Long employment stability

- Strong savings habits

- High net worth

- low overall consumer debt

- strong property value

When these strengths are clearly articulated, underwriters may approve exceptions such as:

- Debt ratios slightly above policy

- shorter employment history

- non-traditional income verification

- credit blemishes with strong explanations

Without that context, the file may simply look like a policy violation.

Real-World Example

Imagine two borrowers with identical financial profiles.

Both have:

- Credit score of 740

- TDS ratio of 46%

- Stable professional employment

Borrower A goes directly to a bank branch.

The system flags the file for exceeding the standard 44% TDS limit.

The file is declined.

Borrower B works with me.

I contact the underwriter and show:

- the borrowers have significant liquid savings

- the property is well below market value

- their income will increase next year due to contractual raises

The underwriter approves the file as a policy exception.

Same borrower.

Same numbers.

Different outcome.

Why This Matters for Realtors and Clients

For realtors, this can mean the difference between:

- a firm deal and a collapsed transaction

- a client buying their next home or losing it

For borrowers, it can mean:

- qualifying sooner

- accessing better financing

- solving income complexity issues

Mortgage underwriting is rarely black and white.

It’s often about how the file is positioned and where it is placed.

The Bottom Line

Going directly to a bank limits you to one interpretation of your financial situation.

Working with me means the file can be:

- strategically structured

- presented to multiple lenders

- positioned for underwriting exceptions when appropriate

That’s why many borrowers who initially hear “no” from a bank later discover that financing was possible all along.

Sometimes the difference isn’t the borrower.

It’s the strategy behind the application.

Real-Life Examples of Underwriting Exceptions

Here are a few scenarios where exceptions often come into play.

Example 1 — Slightly High Debt Ratios

A borrower’s TDS is 46% instead of 44%, but they have:

- Credit score of 790

- $150,000 in liquid savings

- Stable government employment

An experienced mortgage agent can argue the risk is still very low.

Example 2 — Short Employment History

A borrower recently switched jobs but moved to a higher-paying position within the same industry.

An underwriter may treat the employment as continuous.

Example 3 — Self-Employed Income

A borrower shows modest income on tax returns but has significant retained earnings inside a corporation.

A skilled agent can present the corporate financial statements to support the file.

The Story of a Deal That Almost Died

A realtor called me in a panic.

Her clients had already sold their home and were days away from firming up on their purchase.

The bank had just declined the mortgage.

The issue?

The borrower was self-employed and had written off too many expenses.

On paper, the income looked weak.

But when I reviewed the file, the real story looked very different.

The client had:

- Strong credit

- A successful business

- Significant assets

- Large down payment

The problem wasn’t the borrower.

The problem was how the file had been presented.

By restructuring the application and presenting the financials properly, we secured approval through an alternative lender.

The deal closed.

The realtor kept their sale.

And the clients got their home.

That’s the difference exception underwriting can make.

How Realtors Can Use This Knowledge

Realtors who understand underwriting exceptions become far more effective advocates for their clients.

Instead of assuming a deal is dead after one decline, they can:

- Encourage clients to seek second opinions

- Work with mortgage professionals who understand complex files

- Structure deals with realistic financing timelines

Sometimes the difference between a failed transaction and a closed sale is simply knowing which lender to approach.

How Financial Professionals Can Apply These Insights

Financial planners and accountants can also benefit from understanding exception lending.

For example:

- Structuring income for mortgage qualification

- Advising clients on credit management

- Timing large financial decisions

A coordinated approach between financial advisors and mortgage professionals often leads to stronger financing outcomes for clients.

What Borrowers Should Understand About Mortgage Approval

Many borrowers assume mortgage approval is binary.

Yes or no.

But the truth is more nuanced.

Mortgage approval is really about risk interpretation.

Different lenders interpret risk differently.

That’s why a borrower declined by one lender may be approved by another the very next day.

The Value of a Skilled Mortgage Agent in Exception Lending

This is where experience truly matters.

A mortgage agent isn’t just filling out an application.

I’m:

- Structuring the file

- Matching borrowers with the right lender

- Presenting the story behind the numbers

- Advocating for exceptions when appropriate

Think of it like navigating a complex system.

The right strategy can unlock options many borrowers never knew existed.

Allen’s Final Thoughts

Mortgage underwriting in Canada isn’t just about formulas and ratios. It’s about understanding risk, context, and opportunity.

Policies provide structure, but exceptions provide flexibility.

And when a mortgage file is thoughtfully presented, lenders are often willing to look beyond the strict numbers.

That’s where the right mortgage professional can make a tremendous difference.

Whether you’re a realtor trying to save a deal, a financial professional helping clients plan strategically, or a borrower navigating a complicated financial situation, having someone who understands how underwriting really works behind the scenes can open doors that might otherwise stay closed.

My role is to help interpret these policies, identify opportunities for exceptions, and match clients with lenders who understand their full financial story.

Because sometimes the difference between “declined” and “approved” is simply knowing how to present the file the right way.