Renovating a home can be a smart investment, but strategic financing is crucial to maximizing returns while avoiding unnecessary financial strain. Choosing the right funding option can determine how much you can invest in upgrades, and understanding how appraisers assess renovations ensures your improvements translate into tangible home value appreciation.

There are several ways to finance home renovations, each with unique benefits and considerations. The right choice depends on factors such as the scale of the project, available home equity, and long-term financial goals.

Home Equity Line of Credit (HELOC)

Mortgage Refinance for Renovation Financing

Purchase Plus Improvements Mortgage (For Buyers of Fixer-Uppers)

Unsecured Personal Loans & Credit Cards (Short-Term Option)

Government Grants & Rebates for Energy-Efficient Upgrades

How Appraisers Adjust Value for Renovations

Strategies to Ensure Renovations Increase Appraised Value

Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit (HELOC) is an excellent option for large-scale renovations that require flexibility, such as kitchen remodels, basement finishing, or energy-efficient upgrades. A HELOC functions as a revolving line of credit, secured against your home’s equity, allowing you to borrow as needed instead of taking a lump sum upfront.

One of the main advantages of a HELOC is its low interest rate, which is significantly lower than personal loans or credit cards. Additionally, interest-only payments provide flexibility in managing cash flow. However, since HELOCs have variable interest rates, monthly payments can fluctuate. To qualify, homeowners must have at least 20% remaining equity in their property after borrowing.

Mortgage Refinance for Renovation Financing

For homeowners looking to finance a substantial renovation project, refinancing an existing mortgage can be a practical solution. This involves breaking the current mortgage and replacing it with a new one, potentially at a lower interest rate, while borrowing additional funds for renovations.

The main advantage of refinancing is that it provides access to large sums of money at competitive mortgage rates, consolidating the renovation cost into a single predictable monthly payment. However, refinancing comes with its downsides, particularly penalty fees for breaking a fixed mortgage early. Additionally, borrowers need at least 20% home equity after refinancing to qualify.

Purchase Plus Improvements Mortgage (For Buyers of Fixer-Uppers)

Buyers purchasing a fixer-upper can include renovation costs in their mortgage through a Purchase Plus Improvements Mortgage. Lenders approve the mortgage based on the post-renovation value, but the additional funds are only released after the renovation work is completed.

This financing option allows buyers to immediately increase their home’s value with low-interest renovation funding. However, the process requires detailed contractor quotes upfront and mandates that renovations be completed within 90–120 days. Lender and insurer approvals (CMHC, Sagen, or Canada Guaranty) are also required, adding additional layers of paperwork and oversight.

Second Mortgage

For homeowners who do not wish to refinance their first mortgage, a second mortgage is another financing option. A second mortgage is a separate loan placed behind the first mortgage, using home equity as collateral.

The main advantage is that homeowners can access significant funds without breaking their first mortgage, avoiding associated penalties. However, second mortgages typically have higher interest rates than HELOCs or first mortgages and add an additional monthly payment to household expenses.

Unsecured Personal Loans & Credit Cards (Short-Term Option)

For small renovations such as flooring replacements, painting, or minor bathroom/kitchen upgrades, homeowners may opt for unsecured personal loans or credit cards. These financing options do not require home equity, making them accessible for homeowners who may not qualify for secured loans.

While personal loans and credit cards offer fast access to cash, they come with higher interest rates—ranging from 10–20% for personal loans and 19%+ for credit cards—and shorter repayment terms, making them less ideal for substantial renovation projects.

Government Grants & Rebates for Energy-Efficient Upgrades

For those looking to make eco-friendly home improvements, several government grants and rebate programs are available. The Canada Greener Homes Loan & Grant offers grants of up to $5,600 and interest-free loans up to $40,000 for energy-efficient renovations. Additionally, provincial and municipal rebate programs provide incentives for insulation, high-efficiency windows, HVAC systems, and solar panels.

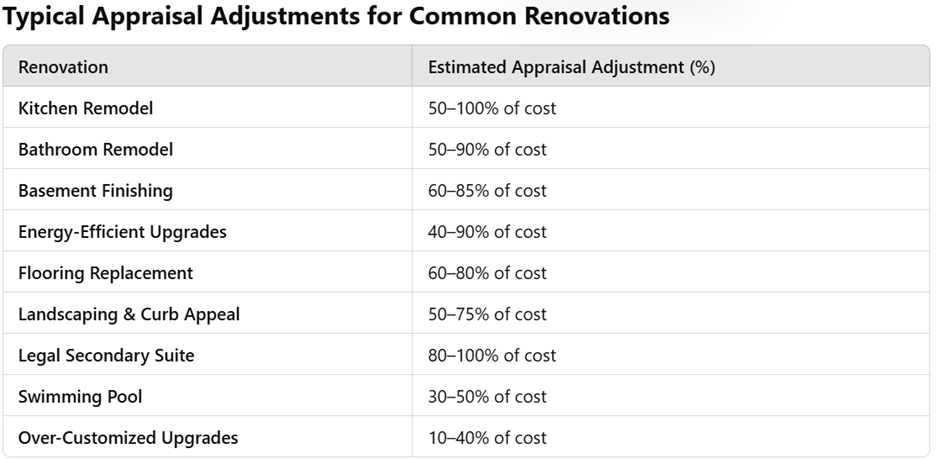

How Appraisers Adjust Value for Renovations

While renovations can increase a home’s appraised value, appraisers do not always give full dollar-for-dollar credit for every improvement. Instead, they analyze the market reaction, comparing homes with and without similar upgrades to determine how much additional value the renovation adds.

Appraisers consider neighbourhood norms, ensuring the improvements align with local buyer expectations. Over-improving beyond neighbourhood standards—such as installing a luxury kitchen in a modest neighbourhood—may not yield a proportional return. Functionality and desirability also play a role; renovations that improve a home’s livability, such as updated kitchens, bathrooms, or legal secondary suites, typically contribute more to appraised value than purely aesthetic upgrades.

How Appraisers Calculate Renovation Impact

Appraisers use paired sales analysis, a method where they compare recent sales of:

- Homes with similar upgrades

- Homes without upgrades

- Market trends and buyer preferences

For example, if two similar homes recently sold—one with a modernized kitchen and the other with its original kitchen—the difference in selling price indicates how much value the kitchen renovation added. If Home A (with an updated kitchen) sold for $850,000 and Home B (with an original kitchen) sold for $800,000, the appraisal adjustment for the kitchen update would be $50,000, even if the owner spent $60,000 on the renovation.

Ultimately, ROI depends on market demand, not renovation cost.

Strategies to Ensure Renovations Increase Appraised Value

To maximize the impact of renovations on an appraisal, homeowners should focus on projects with the highest ROI, such as kitchens, bathrooms, and legal secondary suites. Selecting neutral and modern finishes ensures broad market appeal.

Renovations should also be consistent with neighbourhood standards. Installing a high-end luxury kitchen in a budget-friendly neighbourhood may not result in full value appreciation, as appraisers base adjustments on comparable homes in the area.

Proper permits and documentation are crucial for maximizing valuation. Unpermitted work can lower a home’s appraised value, while documented renovations with receipts, permits, and before-and-after photos provide appraisers with tangible proof of value-added improvements.

Summary: Smart Renovation & Financing Strategy

To ensure a successful renovation and financing strategy, homeowners should:

- Choose HELOCs or refinancing for larger projects and leverage government rebates for energy-efficient upgrades.

- Focus on high-ROI renovations like kitchens, bathrooms, and legal rental suites.

- Prepare for an appraisal by highlighting major upgrades, providing receipts, and ensuring all work is permitted.

By making informed financial decisions and aligning renovations with market demand, homeowners can maximize both immediate returns and long-term property value.