In the ever-evolving landscape of Canadian real estate, rising home prices have made it increasingly challenging for many buyers to enter the market. As a result, gifted funds for down payments have become a significant enabler for many prospective homeowners, especially first-time buyers. This article explores the prevalence of gifting in Canadian mortgages, regional variations in gifted amounts, the purpose and sources of such gifts, along with the rules and processes involved.

The Prevalence and Amount of Gifted Down Payments

Key Characteristics of a Mortgage Gift:

Eligible Givers of Gifted Funds

Rules Around Gifting Money for a Down Payment

Process of Giving a Gift Towards a Mortgage

The Prevalence and Amount of Gifted Down Payments

Gifted down payments are particularly common among first-time homebuyers in Canada, where the high cost of entry into the housing market often outpaces the ability of individuals to save sufficient funds independently. According to recent data, a substantial portion of first-time buyers receive some form of financial gift to help with their down payments. The amount varies significantly by region, reflecting the diverse real estate markets across Canada.

- British Columbia and Ontario: In high-cost markets like Vancouver and Toronto, gifts tend to be larger, often necessary to meet steep down payment requirements. Recent surveys indicate average gifts in these regions can exceed $100,000.

- Prairie Provinces and Atlantic Canada: In areas with more moderate housing prices, such as in Manitoba, Saskatchewan, and the Atlantic provinces, the average gifted amounts are generally lower, ranging from $20,000 to $50,000.

What is a ‘Gift’?

A gift for a mortgage refers to a sum of money given by a family member or sometimes a close friend to a homebuyer, which is used specifically as part or all of the down payment on a property. This gift helps the recipient cover the upfront costs required to purchase a home and is typically used to meet the minimum down payment requirements set by mortgage lenders or to make a larger down payment to avoid or lower mortgage default insurance fees.

Equity Gifting

A gift is not always in the form of cash, sometimes it is in the form of equity. Gifting equity in real estate is a valuable method for assisting someone in buying a home, typically used when a property is being transferred from one family member to another, such as from parents to children. The equity in a property is the difference between the market value of the home and any outstanding mortgage balance. This equity can be used as a gift, reducing the amount the recipient needs to borrow from a lender. Here are some common forms that gifted equity can take:

- Direct Equity Transfer: The equity can be used as a direct contribution towards the down payment required for a mortgage. For instance, if a home is worth $500,000 and has a mortgage of $300,000, there is $200,000 in equity. A portion or all of this equity could be gifted to the buyer to meet the down payment requirement.

- Selling Below Market Value: A common form of gifting equity is to sell the home below its market value to a family member. For example, if parents wish to sell their home valued at $500,000 to their child, they might sell it for $300,000, effectively gifting $200,000 in equity. This transaction lowers the purchase price for the buyer, reducing the mortgage amount needed.

How Does Gifting Equity Work?

- Appraisal: An appraisal is usually required to determine the fair market value of the home. This ensures that all parties understand the actual value of the property and the amount of equity being gifted.

- Gift Letter: Similar to monetary gifts, a gift letter is often required by lenders. This letter should state the relationship between the giver and the recipient, the amount of equity being gifted, and that the gift does not need to be repaid.

- Mortgage Application: The recipient will need to apply for a mortgage on the remaining home value, if necessary. The lender will consider the gifted equity as part of the down payment.

- Legal Documentation: Proper legal documentation must be prepared, often involving a lawyer, to ensure the transfer of equity is legally sound and meets all local and federal regulations.

Considerations and Limitations:

- Tax Implications: There can be tax implications for both the giver and the receiver, including potential capital gains tax for the giver if the property has appreciated in value since it was originally purchased.

- Eligibility for Loans: Lenders may have specific rules regarding how much gifted equity they will accept and what loan products are eligible. Some lenders may also require the recipient to invest some of their own funds, despite the equity gift.

- Legal and Financial Advice: Due to the complexity of such transactions, it is advisable for both parties to seek legal and financial advice to understand the full implications of transferring equity.

Gifted equity can be a great way to help a family member purchase a home while minimizing their financial burden. However, it’s essential to handle such transactions with clear documentation and legal guidance to ensure compliance with all regulations and to address any financial implications effectively.

Living Inheritance

A “living inheritance” is a financial strategy that has gained popularity among older generations looking to support their children’s futures while still alive. This approach involves transferring wealth to children or grandchildren during the parents’ or grandparents’ lifetime, rather than waiting to leave an inheritance after passing away. One of the most significant applications of this concept is in assisting with the purchase of a home, enabling younger family members to secure housing and establish their lives at a stage when they can fully appreciate and utilize the support.

See Living Inheritance: New Beginnings

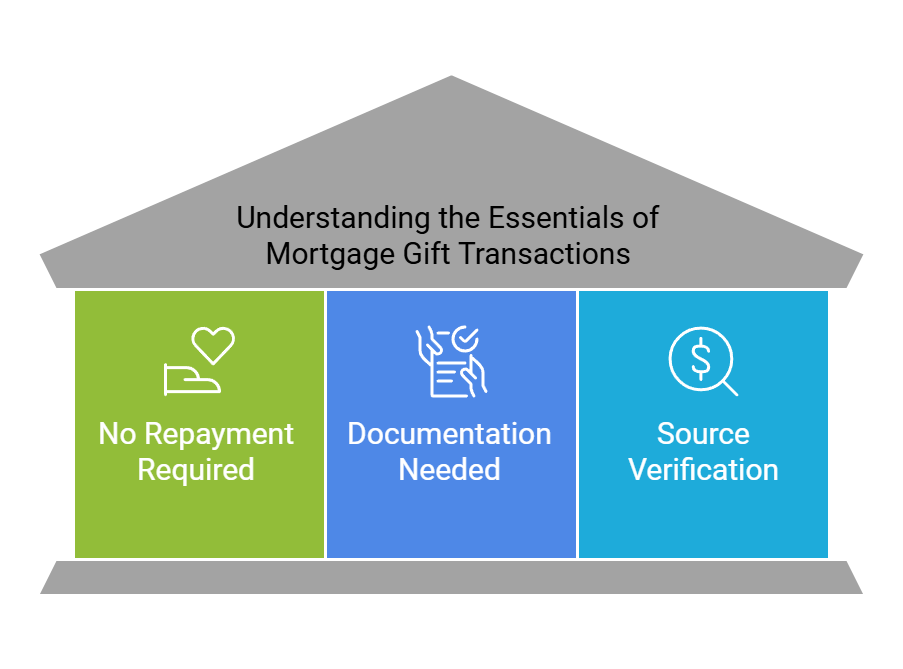

Key Characteristics of a Mortgage Gift:

- No Repayment Required: The most critical aspect of a mortgage gift is that it is exactly that—a gift. This means there is no expectation or legal obligation for the recipient to repay the money.

- Documentation Needed: To qualify as a gift under lender requirements, the donor usually needs to provide a “gift letter” to the mortgage lender. This letter confirms the relationship between the donor and the recipient, states the amount of the gift, and clarifies that the money is a gift and not a loan.

- Source Verification: Lenders often require proof that the funds have come directly from the donor’s account to ensure transparency and to comply with anti-money laundering regulations.

Purpose of a Gift

- Enable Homeownership: Gifts can significantly enhance a buyer’s ability to afford a home, especially in markets where saving for a down payment is challenging due to high property prices.

- Reduce Loan Amount: By increasing the down payment, a gift can reduce the loan-to-value ratio, potentially qualifying the borrower for better mortgage terms and rates.

- Avoid Mortgage Insurance: In Canada, buyers with less than a 20% down payment typically need to purchase mortgage default insurance. A larger down payment, bolstered by a gift, might help avoid or reduce the cost of this insurance.

The primary purpose of gifting funds for a mortgage down payment is to help the recipient qualify for a mortgage by meeting the minimum down payment requirements, which can range from 5% to 20% of the purchase price, depending on the total value of the property and the loan type. Gifts can also help reduce the loan amount, potentially avoiding the need for mortgage default insurance, which is required for down payments of less than 20%.

Gifts for mortgages are a practical solution for many homebuyers, helping them to overcome the financial barriers of entering the real estate market. It’s important for both donors and recipients to understand the implications and requirements of such gifts to ensure a smooth transaction that complies with lender policies.

Eligible Givers of Gifted Funds

Not everyone can gift funds that will be recognized by lenders. Most Canadian mortgage lenders require that gifted funds come from immediate family members. This typically includes:

- Parents

- Grandparents

- Siblings

- Guardian

- Legal dependant

In some cases, lenders may also accept gifts from close relatives such as aunts, uncles, or even family friends, though additional documentation and justification may be required. There are lenders who are willing to allow gifts from non-immediate family members but this is the exception. Spousal gifts may or may not be permitted depending on the lender. See me for details.

Rules Around Gifting Money for a Down Payment

- Documentation: The donor must provide a gift letter to the lender, stating that the money is a gift and not a loan. This letter should confirm that the donor does not expect repayment.

- Source of Funds: Lenders may require proof of the source of the gifted funds to ensure compliance with anti-money laundering regulations.

- No Obligation: The gift must be unconditional, with no obligations tied to the ownership or use of the property.

If giving money unconditionally is a matter of concern, other strategies may be implemented to assist with home ownership such as shared equity programs, co-signing the mortgage to help with qualification, applying for a joint mortgage, house hacking, or purchasing the home tenants in common. Contact me for details.

Process of Giving a Gift Towards a Mortgage

The process typically involves several key steps:

- Gift Letter: The donor can write a gift letter, which includes the donor’s name, relationship to the recipient, amount of the gift, and a statement that no repayment is expected, however, most lenders require applicant’s donors to complete that lender’s templated gift letter (which I will provide). Lenders often require the gift letter to be no older than 90 days before the closing of the purchase transaction.

- Transfer of Funds: Funds should be transferred to the recipient’s bank account preferably well before the closing date (usually at least 15 days) of the home purchase to avoid any delays or issues in the mortgage approval process.

Often an exception can be made by the underwriter to accept gifted funds deposited into the applicant’s account less than 15 days prior to closing if the source of the gift can be verified by verbal inquiries to the donor of the gifted funds to verify the details of the gift letter or through notarized gift letter - Documentation for Lenders: The recipient needs to provide the mortgage lender with the gift letter and proof of the transfer, such as bank statements.

Summary

Gifted down payments are a vital component of the Canadian housing market, especially for first-time buyers struggling with affordability issues. Understanding the rules and processes related to gifting is crucial for both donors and recipients to ensure a smooth transaction. As housing markets continue to evolve, the role of gifted funds remains a key factor enabling many Canadians to achieve their homeownership dreams.