Mortgage Terms

Get a Better Understanding of Mortgages!

The Surge in Private Mortgages

Surge in Private Mortgages: If you’re a homeowner, buyer, realtor, or financial professional, you’ve probably felt it already. Deals are more complex. Financing conversations are happening earlier. And outcomes that used to be automatic now require real strategy. That’s not a slowdown—it’s a shift.

The 10 Principles of APR

10 Principles of APR: But APR — the Annual Percentage Rate — is where the real truth lives, not in the advertised rate—which is NOT what you pay. APR exists to answer a more important question: what does this mortgage actually cost once everything required is accounted for?

Is Your Mortgage Rate Lying to You?

Is Your Mortgage Lying? The interest rate is only part of the story. The real story—the one that tells you what the mortgage actually costs you—is hidden in a number most people barely glance at: APR.

My World of Shadow Banking

… Inside the Black Box of Mortgage Lending and Real Estate Finance Most Canadians think mortgages are simple. You walk into a bank, talk to someone behind a desk, sign some papers, and that’s that. Clean. Simple. Straightforward. That’s so yesterday! But the truth—one...

Prime Rate Panic-Proofing

Prime Rate Impact Calculator: If you’ve ever watched the news, heard “rates are moving,” and felt your stomach drop a little—yeah, you’re not alone. Most Canadians don’t actually need more opinions about interest rates. They need clarity. That’s exactly what my Prime Rate Impact Calculator is built to do: turn prime-rate chatter into real numbers you can understand, stress-test, and use to make smart decisions

What a Mortgage Agent Does

What a Mortgage Agent Does: My world of real estate finance is like a black box to most people, including financial professionals like bankers, lawyers, accountants, and financial planners. Sure, they might have some high-level exposure and education to the general concepts around real estate finance and mortgages in particular, but how my world works from the inside and what really goes on is a mystery and hidden from public view, especially that part of my world that is shadow banking.

10 Big Benefits of Going Variable

Variable Mortgages. If you’ve ever surfed—or even watched someone surf—you know it’s all about balance. You don’t fight the wave; you ride it. That’s exactly what it feels like to hold a variable-rate mortgage. Sure, the water can get choppy, but if you’ve got good footing, it can take you further, faster, and often cheaper than the safer route.

Canadian Land Transfer Tax Calculator

Land Transfer Tax Calculator: Buying a home in Canada is a thrilling adventure — whether it’s a downtown condo, a family home in the suburbs, or a cabin near the lake. But between deposits, inspections, and closing paperwork, there’s one cost that often catches buyers off guard: the Land Transfer Tax (LTT).

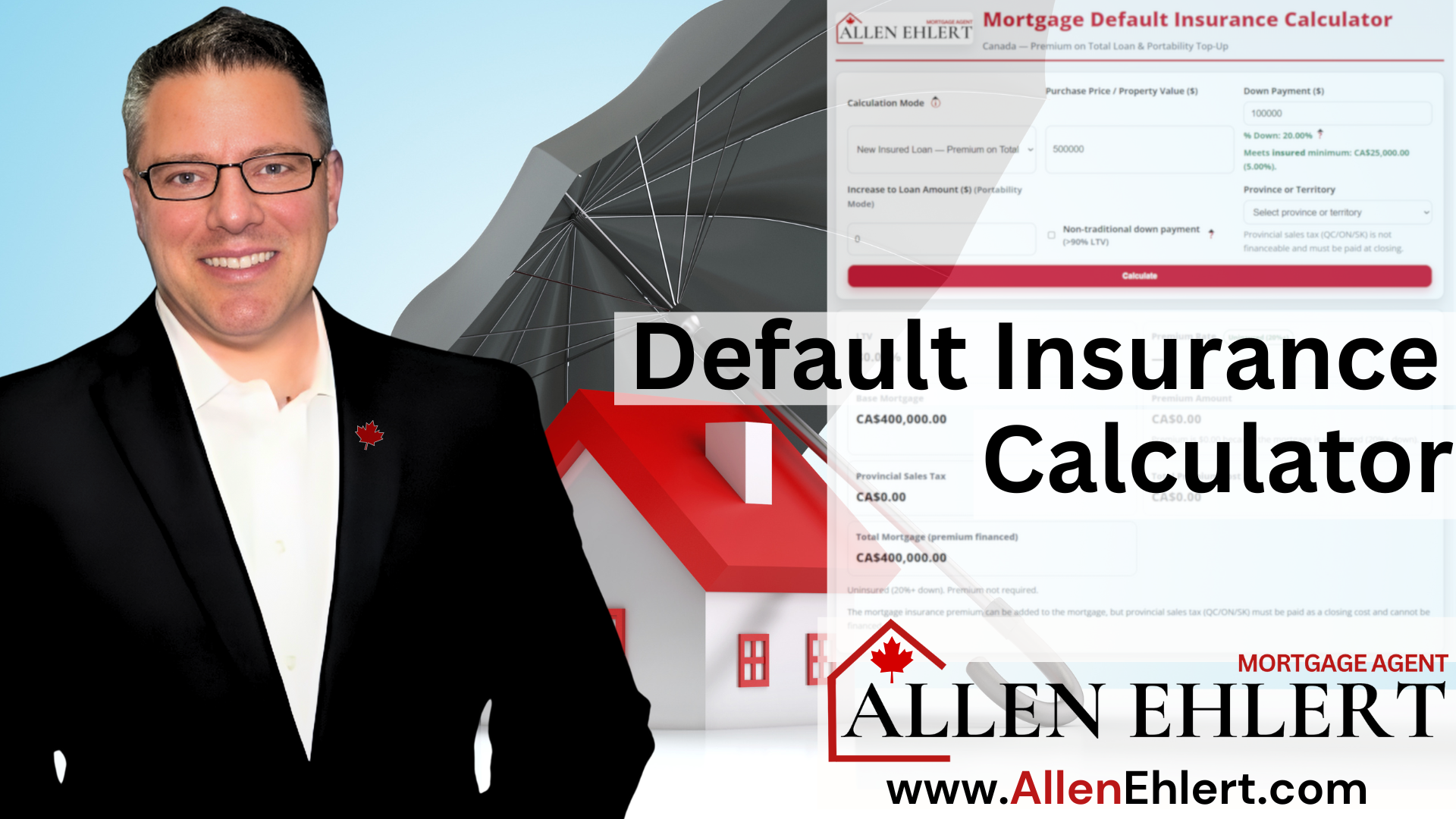

Mortgage Default Insurance Calculator

Mortgage Default Insurance Calculator: Buying a home in Canada can feel like stepping into a maze of numbers, acronyms, and fine print — but it doesn’t have to. Whether you’re a first-time buyer or a seasoned investor, understanding how default insurance works is key to knowing your real costs and options.

Canadian Closing Costs Calculator

Canadian Closing Costs Calculator: Buying a home is one of those life-changing moments that’s equal parts thrilling and nerve-wracking. Between scrolling listings, making offers, and imagining your first morning coffee in the new kitchen, it’s easy to overlook one key detail — closing costs. These aren’t the fun, HGTV-type parts of buying a home, but they’re essential.

How to Use My Mortgage Discharge Cost Calculator

Mortgage Discharge Calculator: This tool is designed to help you see—clearly and early—what it actually costs to remove a mortgage from title, based on the type of lender you’re dealing with. Whether you’re refinancing, switching lenders, selling a property, or restructuring debt, knowing these numbers in advance puts you back in control.

Why My Pre-Approval Is Better

Pre Approval: When you’re getting ready to buy a home, that pre-approval letter feels like a badge of honour — proof that you’re serious, qualified, and ready to make your move. But here’s what most buyers (and most realtors) don’t realize: not all pre-approvals are created equal.

Protect Your Mortgage

Mortgage Protection Insurance: Buying a home, especially your first home is one of those big, life-defining moments. You and your partner have been budgeting, working with your mortgage agent, hunting down listings, talking to realtors, and imagining what that first night in a place that’s finally yours will feel like. But beneath all the excitement, there’s a quieter, more grown-up question that every couple needs to ask—“If something unexpected happens, can we not lose this home we worked so hard for?”

Understanding Contributory Income

Contributory Income: Every once in a while, a mortgage file comes along that makes you smile—not because it’s easy, but because you know exactly what lever to pull to make the deal work. Contributory income is one of those levers. It’s the quiet, seldom-talked-about income source that can turn a “maybe” into a confident “yes,” especially when buyers are stretched, ratios are tight, or affordability feels like a moving target. And if you’re a realtor guiding clients or a borrower trying to qualify, understanding how contributory income works is like unlocking a hidden chapter in the rulebook.

Understanding Shelter Costs

Shelter Costs: If you’ve ever felt like lenders were speaking a different language when they talk about “shelter costs,” you’re not alone. Clients often look at me like I’m explaining astrophysics when I break down why lenders assign a shelter cost—even when a borrower is living in their parents’ basement and paying nothing more than a smile and a promise to take out the garbage.

10 Benefits of Choosing Fixed

Fixed Mortgages: Let’s face it—choosing a mortgage can feel like standing at a financial crossroads with a blindfold on. Do you gamble on a variable rate, hoping the market stays friendly, or do you lock into a fixed rate and sleep peacefully at night knowing exactly what your payment will be?

Consumer-Directed Finance Is Almost Here

Consumer Directed Finance: Let’s be real—getting a mortgage in Canada can sometimes feel like dragging a sack of bricks uphill. Between pay stubs, NOAs, bank statements, and all the back-and-forth emails, it’s no wonder many clients feel stressed before the real house hunt even begins. But what if I told you there’s a new way coming that could cut through the red tape, give you more control, and make the whole process smoother?

Canadian Home Carrying Cost Calculators

Canadian Home Carrying Cost Calculator: You’ve found the dream home: open-concept kitchen, backyard for summer BBQs, maybe even a finished basement for movie nights. The mortgage payment looks doable. But here’s the kicker: just because you can afford the payment doesn’t mean the bank will agree.

Ultimate Canadian Closing Costs Calculator

The Ultimate Canadian Closing Costs Calculator. This tool doesn’t just spit out a random number—it walks through all the hidden (and not-so-hidden) expenses that come with buying a home in Ontario. It accounts for the type of buyer you are, the kind of mortgage you’re getting, and every little adjustment in between.

“What’s Your Lowest Rate?”

Lowest Rate: If you’ve ever called a mortgage agent and led with the question, “What’s your lowest rate?”, you’re in good company — it’s probably the most common question in our industry. And honestly, I get it. Rates are tangible. They’re plastered all over billboards, bank websites, and radio ads.

Canada’s Ultimate Home Purchase Price Calculator

Purchase Price Affordability Calculator: Buying a home is exciting—no doubt about it. But let’s be honest: it’s also one of the biggest financial decisions you’ll ever make. The million-dollar (well, sometimes literally) question is, “How much house can I actually afford?” That’s where my Purchase Price Affordability Calculator comes into play.

Loan-to-Value’s Mortgage Impact

When you’re house hunting, refinancing, or even just thinking about tapping into your home equity, there’s one little number that keeps popping up: Loan-to-Value (LTV). It sounds technical—and it is—but once you get it, you’ll see why lenders, insurers, and even private investors obsess over it. And here’s the kicker: your LTV doesn’t just decide if you qualify, it directly impacts the rate you’ll pay.

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate