… When Lenders Pull Out the Magnifying Glass at the Last Second

If you’ve ever had a mortgage deal that felt like it was sailing smoothly through underwriting, only to suddenly slow to a crawl with more questions, more documents, and more back-and-forth than you thought possible, you may have run into deep due diligence.

This is the lender equivalent of a deep dive—a second, more intense layer of review that goes well beyond standard underwriting. And in today’s tighter lending environment, it’s becoming more common.

If you’re a borrower, realtor, or even another mortgage pro, understanding what deep due diligence is, why it happens, and how to prepare for it can make the difference between a closed deal and a dead deal.

Topics I’ll Cover

Why Lenders Are Doing It More Now

How It Follows Standard Underwriting

Why a Mortgage May Be Selected for Deep Due Diligence

When Deep Due Diligence May Occur

How It Can Impact the Borrower and the Deal

What Deep Due Diligence Is

Deep due diligence is exactly what it sounds like—a lender taking a much closer, more forensic look at your mortgage file. Instead of simply confirming the basics, they dig deeper into income sources, asset origins, property history, and even market conditions.

It’s not a random paperwork exercise. It’s risk management on a granular level, where the lender isn’t just asking, “Does this deal meet our guidelines?” but also, “Are there any hidden risks here that we didn’t spot the first time?”

Why Lenders Are Doing It More Now

In today’s market, lenders face increasing regulatory oversight, heightened fraud concerns, and shifting economic conditions. OSFI (the banking regulator) has made it clear: risk must be mitigated before funds are released.

A standard underwrite might catch the obvious—a missing T4, a shortfall in down payment funds—but deep due diligence is designed to catch the subtle things that could cause trouble down the road:

- A sudden unexplained deposit

- A property with zoning quirks or a pending special assessment

- A borrower in a volatile industry where job stability could change overnight

The truth? Lenders would rather slow down a deal than end up holding a bad loan.

How It Follows Standard Underwriting

Here’s the flow:

- Normal underwriting happens first—collecting documents, verifying income, confirming down payment, reviewing the property appraisal, and making sure everything meets lender guidelines.

- Once conditions are met, the file might be selected for deep due diligence.

- At this stage, the lender re-verifies certain items and investigates deeper. Think of it as taking the standard “yes” and running it through a second, stricter filter.

If underwriting is the initial security check at the airport, deep due diligence is the random bag search right before you board.

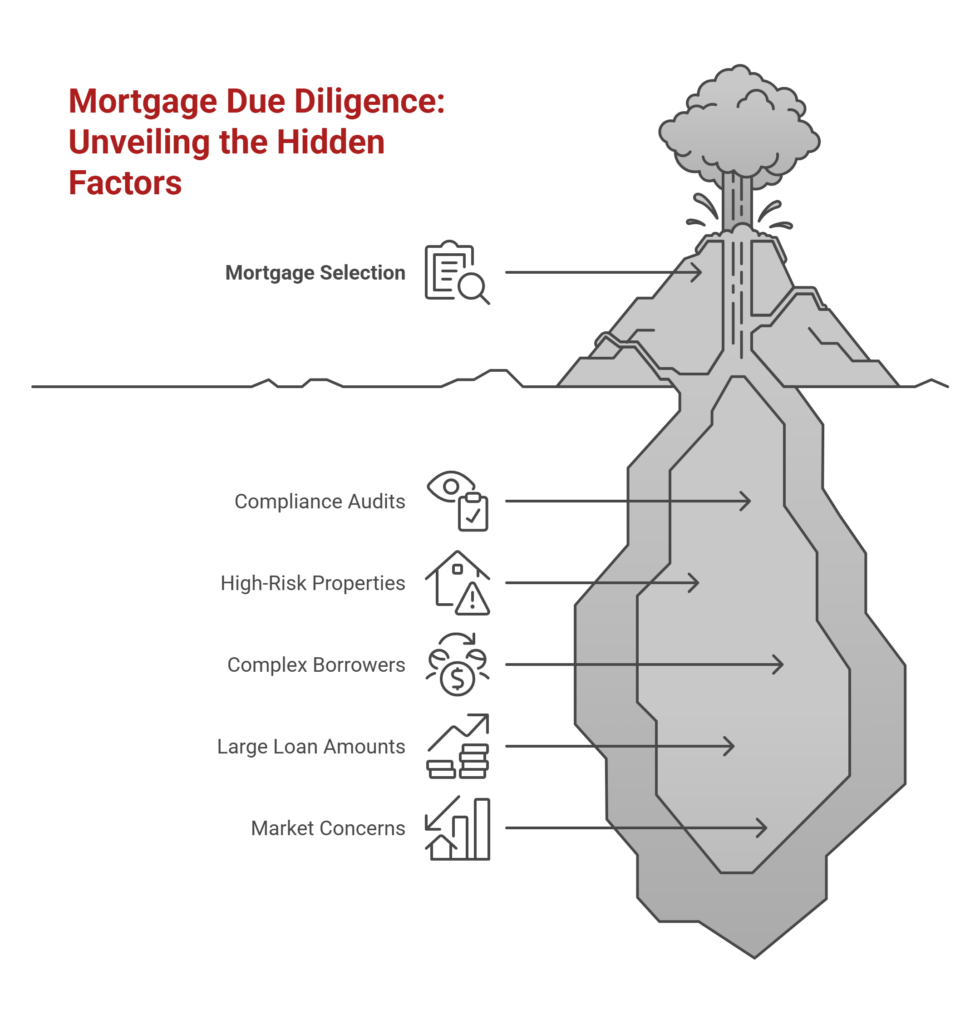

Why a Mortgage May Be Selected for Deep Due Diligence

Not every mortgage gets the full microscope treatment, but here are some common triggers:

- Random compliance audits – some files are chosen purely for quality control.

- High-risk property types – rural homes, unique builds, or properties with secondary suites.

- Complex borrower profiles – multiple income sources, self-employed, or heavy reliance on commissions/bonuses.

- Large loan amounts – higher exposure means more scrutiny.

- Market concerns – properties in declining-value neighbourhoods.

When Deep Due Diligence May Occur

This can happen after your deal has been fully approved but before the funds are sent to your lawyer or FCT.

Sometimes, deep due diligence is triggered late in the process—yes, even days before closing. That’s why a deal that feels “done” can suddenly stall.

How It Can Impact the Borrower and the Deal

For borrowers, deep due diligence can mean:

- More document requests: extra bank statements, tax returns, proof of large deposits.

- Third-party verifications: the lender might call your employer again, order another appraisal review, or verify zoning with the municipality.

- Delays: if information isn’t readily available, closing dates can be pushed.

- In rare cases, deal collapse: if deep due diligence uncovers something that changes the risk profile, the lender can withdraw the approval.

A Story from the Trenches

‘Mike’ was buying a home in Whitby with a clean approval from a major bank. We were two weeks from closing when his file was randomly pulled for deep due diligence.

The lender asked for updated bank statements, which revealed a recent $40,000 deposit from the sale of some personal assets. The problem? No paper trail. We had to scramble to get receipts, transfer confirmations, and even a sworn statement from the buyer of those assets.

It delayed closing by three days, but we kept the deal alive. Without fast responses, Mike could have lost both his home and his deposit.

How Realtors & Clients Can Put This to Practice

- Realtors: Build “document readiness” into your buyer prep. The more organized your client’s paperwork is, the less painful a deep dive will be.

- Clients: Keep a clean paper trail for all funds, especially large deposits. If you sell a vehicle or get a bonus, document it like you’re preparing for a court case.

Allen’s Final Thoughts

Deep due diligence isn’t meant to scare you—it’s meant to protect the lender (and indirectly you) from surprises. But it can be stressful if you’re not ready for it, especially if it pops up late in the game.

That’s where I come in. As your mortgage agent, my role doesn’t end when you get the approval email. I anticipate what might trigger a deep dive, prepare you ahead of time, and if the lender does start asking for “one more thing,” I handle the back-and-forth so you’re not left scrambling.

Whether you’re a first-time buyer, a seasoned investor, or a realtor guiding your clients through the process, I’m here to make sure that even if a magnifying glass gets pulled out, you still make it to the finish line—keys in hand, stress-free.