Did you know over 40% of Canadians use support payments in their mortgage applications? This fact shows how important support payments are for getting a mortgage. It’s key to know how these payments affect your mortgage chances and long-term finances.

In Canada, support payments are a big part of household income. They can greatly affect your mortgage application. If you get or give support payments, understanding their role in mortgages is essential. This article will help you use support payments to increase your mortgage income. This way, you can feel sure about your mortgage process.

Key Takeaways

- Support payments are a big part of many Canadians’ mortgage eligibility.

- It’s important to know how support payments change your income for mortgage applications.

- Having correct support payment documents can make your mortgage application stronger.

- Think about the tax effects of support payments when looking at your income.

- Rules on support payments for mortgages differ by province.

Understanding Support Payments and Mortgages

Support payments are key when you’re looking at getting a mortgage. They can come from court orders or agreements to help a spouse, partner, or kids. Knowing about these payments is crucial, whether you’re getting or paying them, to meet mortgage requirements.

What Are Support Payments?

A court order or agreement may order the payment of support. They help a spouse, partner, or kids after a split or divorce. There are two main kinds: spousal and child support. Each has its own rules and affects your money and taxes.

Types of Support Payments

There are two main kinds of support payments for mortgage purposes:

- Spousal Support Payments: These are for the upkeep of a spouse or partner. They’re based on both incomes and how long the relationship lasted.

- Child Support Payments: These cover costs like food, clothes, school, and hobbies for kids. They can come from a court or agreement.

Here’s a table to show the differences:

| Type of Support Payment | Purpose | Mandated By |

|---|---|---|

| Spousal Support Payments | Financial upkeep of a spouse or partner | Court order or agreement |

| Child Support Payments | For child expenses | Court order or agreement |

This information helps you see how support payments affect your mortgage income. It makes sure you meet the financial needs for a mortgage.

How Support Payments Affect Mortgage Eligibility

It’s important to know how support payments affect your chance of getting a mortgage. Lenders look at support payments to make sure you can handle your debts. They use the Debt Service Ratios to check if you qualify for a mortgage.

Impact on Debt Service Ratio (GDS and TDS)

Lenders check your ability to pay your mortgage by looking at the Debt Service Ratio. The GDS ratio looks at your housing costs versus your income. The TDS ratio adds in other debts like loans and credit cards. Support payments can change your GDS and TDS ratios, which can affect your mortgage eligibility.

- GDS Ratio: This includes mortgage principal, interest, property taxes, and heating costs, divided by your gross income.

- TDS Ratio: This includes the GDS components along with other obligations like car loans and credit cards, divided by your gross income.

| Ratio Type | Components | Impact of Support Payments |

|---|---|---|

| GDS | Mortgage principal, interest, property taxes, heating costs | Support payment income can increase gross income, improving GDS ratio |

| TDS | All GDS components plus other debts (loans, credit cards) | Support payments can positively affect TDS ratio by enhancing gross income |

Income Consideration in Mortgage Calculations

Lenders consider support payment income when calculating mortgages. This can make it easier to get a mortgage if your support payments are steady and documented. Make sure all your support payments are consistent and legally proven to be included in the mortgage calculations.

“Support payments can significantly enhance your gross income, making it easier to meet the required Debt Service Ratios for mortgage approval, provided you can substantiate the reliability of this income source.”

To use support payments in mortgage calculations, you need to understand their effect on GDS and TDS ratios. Keeping accurate records and steady payment history is key to using support payments well in your mortgage application.

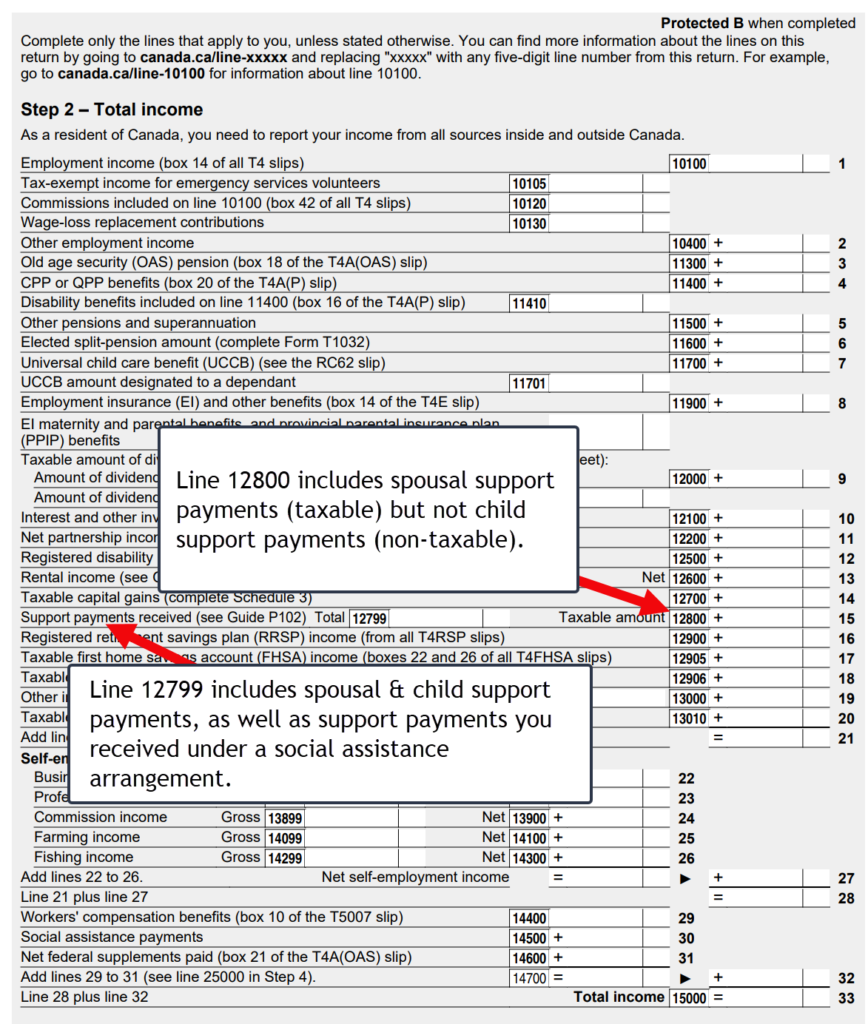

Tax Implications of Support Payments on Income

It’s important to understand how support payments affect taxes in Canada. Both payers and recipients need to know about income tax and T1 forms. It’s key to know the difference between spousal and child support payments.

Tax Deductibility of Spousal Support

Spousal support payments might be tax deductible for the payer, lowering their taxable income. But, the person getting support must pay taxes on it. The Canada Revenue Agency (CRA) has rules for this, like the support coming from a legal agreement or court order.

Tax Treatment of Child Support

Child support has different tax rules than spousal support. If the agreement was made after April 1997, the payer can’t deduct child support from their taxes. The person getting support doesn’t have to pay taxes on it. This affects how both people plan their finances, like when getting a mortgage.

| Support Type | Tax Deductibility (Payer) | Taxable Income (Recipient) |

|---|---|---|

| Spousal Support | Yes | Yes |

| Child Support (Post-April 1997) | No | No |

Documentation Requirements for Mortgages

When you’re looking into mortgage documentation, it’s key to have all your records ready. Making sure you handle support payment processing and other documents correctly can help you get your mortgage approved.

Providing Court Orders and Written Agreements

One big step is to give lenders the right court orders and written agreements. These documents prove you’re legally bound to make support payments. They help lenders check if you’re legally supposed to make payments and what those payments should be.

Validating Payment History

Along with court orders and agreements, you also need to show a solid payment history. Lenders want to see you’ve been making payments regularly, often for a year or more. This shows they can count on you to keep up with your payments.

By getting your mortgage documentation in order, including court orders, written agreements, and a solid payment history validation, you make a strong case. This can boost your chances of getting a mortgage.

Support Payments and Mortgage Affordability

It’s key to know how support payments affect your mortgage affordability. These payments, like spousal or child support, are crucial in figuring out what mortgage you can handle.

Calculating Mortgage Affordability with Support Payments

Figuring out what mortgage you can afford is more than just looking at your main income. You must include support payments in your calculations. They add regular, predictable money to your budget. This way, you get a better idea of the mortgage you can manage without going over your budget.

For easy and accurate calculations, use an online support payment calculator. These tools let you enter your support payment details. This gives you a clear idea of how much mortgage you can afford.

Using Online Support Payment Calculators

Online tools for support payments make checking your finances easier. A support payment calculator looks at your total income. This includes your regular income and support payment options. It then uses this information to figure out what mortgage you can afford.

Here are some things to keep in mind when using these calculators:

- Income Sources: Make sure to include all your income, including support payments.

- Current Financial Obligations: List your current debts accurately to get a true picture of what you can handle.

- Support Payment Options: Try different support payment amounts to see how they change your mortgage limit.

Below is a table showing how various support payment amounts can change your mortgage affordability:

| Support Payment Amount | Total Monthly Income | Maximum Mortgage Affordability |

|---|---|---|

| $500 | $3,500 | $350,000 |

| $1,000 | $4,000 | $400,000 |

| $1,500 | $4,500 | $450,000 |

By using these tools and including all your income, you can make a smarter choice about your mortgage. This ensures you pick a mortgage that suits your financial situation.

Using Support Payments as Income for Mortgage Applications

Lenders look at different income sources, including support payments, when you apply for a mortgage. It’s important to know the rules for support payments.

Criteria for Accepting Support Payments as Income

Support payments can boost your income for a mortgage application. But, they must meet specific criteria. Payments should be steady, reliable, and likely to keep going for a long time. They should have been coming in for at least six months without missing a beat.

- The support must be legally mandated, such as through a court order or legally binding agreement.

- Ensure that the payments are regular and have been consistently received over a specified period.

- The payer’s track record of reliability is also taken into consideration.

- The anticipated continuation of the support payments over the mortgage term is necessary for validation.

Examples of Accepted Documentation

Getting your mortgage application right is key when using support payment income. Lenders will look at your support payment guidelines closely. They want clear proof of how the payments work.

| Document Type | Description | Requirement |

|---|---|---|

| Court Order | A legal document issued by a court mandating the support payments. | Must be up-to-date and reflect current payment arrangements. |

| Written Agreement | A formal agreement signed by both parties detailing the support payment schedule and amounts. | Should be notarized or otherwise authenticated to ensure legality. |

| Payment Receipts | Documentation showing the receipt of support payments, such as bank statements or transaction records. | Consistent records over a period of at least six months are usually required. |

By meeting these criteria and providing strong documentation, you boost your chances of getting a mortgage with support payment income.

Provincial Guidelines and Support Payments in Canada

Knowing about provincial guidelines is key when dealing with mortgages in Canada. Each province has its own rules for Canadian support payments. It’s important to know these rules in your area.

Support payment guidelines can change how much you get or pay. They also affect your mortgage applications and how much you can borrow. This is why it’s important to understand these rules.

Let’s look at how different provinces handle support payments:

| Province | Eligibility Criteria | Enforcement Mechanisms |

|---|---|---|

| Ontario | Based on income and number of dependents | Family Responsibility Office (FRO) |

| British Columbia | Determined by the Family Law Act | Family Maintenance Enforcement Program (FMEP) |

| Quebec | Calculated using the child support determination form | Revenu Québec |

| Alberta | Guided by the Federal Child Support Guidelines | Maintenance Enforcement Program (MEP) |

For help with support payment guidelines in your province, talk to legal experts or use provincial resources. This way, you’ll know how provincial guidelines affect your support payment eligibility. It makes applying for a mortgage easier.

Challenges and Solutions in Using Support Payments for Mortgages

When you’re looking for a mortgage, you might face issues with support payments. These issues include proving they are stable and will last. But, there are ways to tackle these problems.

A big challenge is showing that support payments are steady income. Lenders want to see payments for six months to a year. To prove this, keep detailed financial records. This includes bank statements and court orders for support payments.

Also, different lenders have their own rules for support payments. It’s important to look at your options with various lenders. Talking to mortgage experts can help you find the best one.

To underscore the importance of thorough documentation, one successful approach is maintaining a record that consistently demonstrates the receipt and stability of support payments over a significant time frame.

Another good idea is to look into mortgage plans made for support payment challenges. Work with mortgage advisors who know how to help you. They can make a plan that fits your financial situation and any hurdles you might face.

- Seek advice from mortgage professionals who are experienced in handling support payments.

- Maintain a detailed and updated record of your support payment history.

- Explore different lenders to find the ones with suitable support payment options.

By taking these steps, you can boost your chances of getting a mortgage despite the challenges with support payments.

Additional Factors to Consider with Support Payments

Understanding support payments in mortgages is key. Factors like mortgage rates and changes in support payment agreements affect how much you can afford. These changes are crucial for your financial health.

Impact of Mortgage Rates

Mortgage rates change often and affect how much you need to earn for a mortgage. When rates go up, so do your monthly payments. This means your support payments play a bigger role in your mortgage.

It’s important to keep an eye on rate trends. They can change your mortgage plans a lot.

Effect of Changed Support Payment Agreements

Changes in support payment agreements matter a lot. Whether it’s more or less money, it changes what lenders see as your income. Make sure to update your lenders about these changes.

This keeps your financial plan strong, even when support payments change.

| Factor | Impact on Mortgage |

|---|---|

| Mortgage Rates Impact | Higher rates increase monthly payments, reducing mortgage affordability. |

| Support Payment Adjustments | Changes in agreements can alter the recognized income, affecting mortgage qualifications. |

| Changed Agreements | Ensure any modifications in support agreements are well-documented for lender review. |

Conclusion

Understanding how support payments affect your mortgage eligibility is key in Canada. These payments play a big role in your financial planning. They help shape your strategy and make getting a mortgage easier.

When planning your mortgage, make sure to include support payments. This means keeping track of court orders and making regular payments. Lenders look at this when you apply for a mortgage.

By adding support payments to your income, you can make better financial choices. This can lead to better mortgage deals. It’s a complex process, but with the right approach, you can feel more confident about buying a home in Canada.

FAQ

What are support payments?

Support payments are regular money given by a court order or agreement. They help support a spouse, common-law partner, or kids. There are two types: spousal and child support. Each has its own tax rules and goals.

How do support payments impact mortgage eligibility?

Support payments can change the GDS and TDS ratios lenders look at. These ratios help figure out if you can get a mortgage. Changes in these ratios can affect how much you can borrow.

Are spousal support payments tax-deductible?

Yes, spousal support payments might be tax-deductible for the person paying them. They are taxed for the person getting them, under certain conditions. This affects your income and your chance of getting a mortgage.

Are child support payments tax-deductible?

Child support payments made after April 1997 aren’t deductible for the payer. They have special tax rules. This can change the income lenders see for your mortgage application.

What documentation is required for mortgages that consider support payment income?

You’ll need to show court orders or agreements when applying for a mortgage with support payments. Also, proof of consistent payments is needed to show the income is steady and reliable.

How can support payments affect mortgage affordability?

Support payments can change how much you can afford for a mortgage. There are online tools and calculators to help figure this out. They show how these payments affect your mortgage budget.

What criteria must be met for support payments to be accepted as mortgage income?

You must provide court orders or agreements that detail payment amounts and schedules. Also, proof of payments or deposits is needed. This proves the support payment is a steady source of income.

Are there provincial guidelines for support payments in Canada?

Yes, Canada has provincial rules for support payments. These rules affect who can get support, how much they get, and how it’s enforced. These rules also impact mortgage applications and what you can afford.

What challenges might arise when using support payments for mortgage applications?

You might struggle to prove that support payments are steady and will continue. Keeping good financial records and getting advice from mortgage experts can help overcome these issues.

Do fluctuating mortgage rates affect income requirements when support payments are involved?

Yes, changing mortgage rates can change how much you need to earn for a mortgage, even with support payments. Any changes in support payments can also affect your mortgage chances.