Real Estate > Personal Finance > Mortgage

In the golden light of dawn, while much of Ontario still slumbers, thousands of commuters from suburbs like Whitby and Oakville embark on their daily pilgrimage to Toronto. This journey, often romanticized as a quest for better opportunities, comes with a hefty price tag – both in terms of time and money.

The Financial Cost of Commuting Broken Down

The Horribly Expensive 407 ETR

Commuting as a Percentage of Your Take Home Salary

Commuting Costs While Living Within Toronto

Time to Re-Consider Commuting Costs

General Rule of Thumb: Commuting Costs

Commuting Costs Are Higher for Women

Commuting’s Personal Finance Cost

Consider the Alternatives to Commuting

Political and Social Implications of Commuting

The Financial Cost of Commuting Broken Down

The financial cost of commuting is considerable. It is different depending on whether you GO Train or GO Bus it into Toronto and from where, or do you drive in via the 401 or take the most expensive toll highway in the world, the 407 ETR. It can also depend on how disciplined you are in terms of buying lunch or coffee, how much you pay for clothes, whether you need to also take the TTC or not. No matter how you slice it, commuting to work is extremely expensive.

Below is a breakdown of what it typically costs to commute to Toronto for work. Even if you live within Toronto (Intra-Toronto) you are still paying a lot to go to work; you just don’t have the costs of commuting into the city. However, what’s not be included in the table below is the cost of parking if you have to pay it.

If you live outside of Toronto, you have the cost of going into work (lunch, coffee, clothes, cleaning, TTC) which add up to over $9,000 per year, plus the cost of just getting to Toronto. In the GTA, just getting to Toronto is a big deal as GTA commuters travel the farthest distance of most commuters around the world at some of the highest costs. Consequently, if you commute into Toronto from Oakville via the GO Train your annual cost is around $8,114 to get to Toronto, plus another $9,360 once you are there for an annual total of $17,474.40. For similar commuters from Whitby, the cost is $18,328.80. Sadly, that’s about as cheaply as you can do it.

The Horribly Expensive 407ETR

The 407 ETR (Express Toll Route) in Ontario, Canada, is renowned for its cost, often considered the most expensive toll road globally. The cost of traveling on the 407 ETR varies based on factors like the time of day, vehicle type, and distance traveled. Peak rates can be quite high, with charges per kilometre that can exceed CAD 0.56. This means a 40-km trip could cost around CAD 22.40 plus H.S.T. for $25.31 or more, depending on these variables.

For a commuter coming in from Whitby, the annual cost of driving to the Yonge Street exit taking the 407ETR is $29,815.20 a year. This includes a Canada Revenue Agency adopted 68 cents per kilometer and the HST charged for the 407ETR. It doesn’t include other mandatory 407ETR costs and fees such as transponder charges, returned payment fees, enforcement fees, transponder replacement fees, account fees, trip toll charge, dispute fee, transponder security deposit fee, and so on.

For a commuter coming in from Oakville, the annual cost of driving to the Yonge Street exit taking the 407ETR is $44,805.60 a year. This includes a Canada Revenue Agency adopted 68 cents per kilometer and the HST charged for the 407ETR. It doesn’t include other mandatory 407ETR costs and fees such as transponder charges, returned payment fees, enforcement fees, transponder replacement fees, account fees, trip toll charge, dispute fee, transponder security deposit fee, and so on.

How 407ETR Compares to the World’s Most Expensive Highways

Commuting: An After Tax Cost

Lastly, keep in mind that the money you pay to commute to work just to make a living comes from your after tax income. Considering the median income for Canadians in 2024 is around $60,000 per year, you can literally eat up most if not all of your paycheque just commuting to work by taking the 407ETR. Here’s a breakdown of what you take home after taxes in Ontario:

| Salary (Before Tax Income) | Take Home (After Tax Income) |

| $ 40,000.00 | $ 32,005.00 |

| $ 50,000.00 | $ 39,211.00 |

| $ 60,000.00* (Median) | $ 45,673.00* (Median) |

| $ 70,000.00 | $ 52,291.00 |

| $ 80,000.00 | $ 59,326.00 |

| $ 90,000.00 | $ 66,300.09 |

| $ 100,000.00 | $ 73,115.00 |

| $ 110,000.00 | $ 79,229.00 |

| $ 120,000.00 | $ 84,888.00 |

| $ 130,000.00 | $ 90,547.00 |

| $ 140,000.00 | $ 96,206.00 |

| $ 150,000.00 | $ 101,865.00 |

| $ 200,000.00 | $ 128,323.00 |

| $ 250,000.00 | $ 153,093.00 |

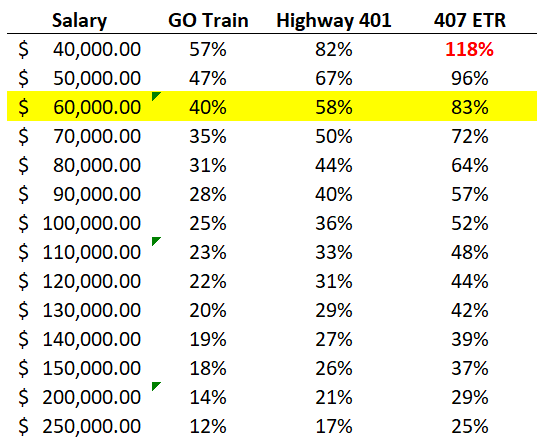

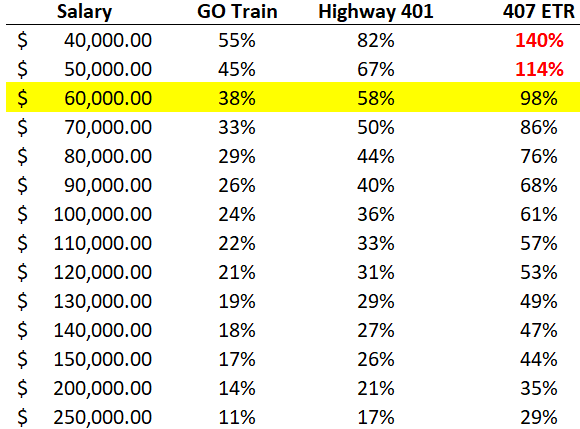

Commuting as a Percentage of Your Take Home Salary

A good way to look at how much commuting is costing you is to view commuting as a percentage of your take home salary. When you review your commuting costs as a percentage of your take home salary, you soon realize that for many people, commuting can be more expensive than what they pay for rent or a mortgage. It certainly is more expensive than what they pay for food.

Here are some tables that show the cost of commuting as a percentage of take home salary depending on the method you use to commute. The cost will be higher or lower depending on how far or close you live to Toronto but they provide some good ballpark percentages.

Whitby, Ontario

Oakville, Ontario

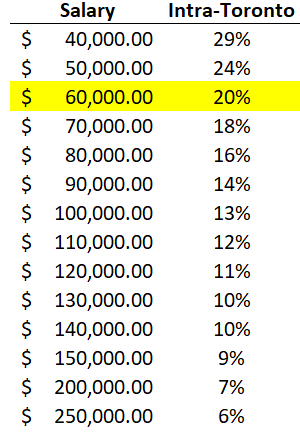

Commuting Costs While Living Within Toronto

Even if you live within the City of Toronto, it still costs you money to go into the office, you just don’t have to pay the commuting costs to get into Hogtown. Nevertheless, you still need to look and dress like a professional, you still need to eat lunch, grab some caffeine, and ride a crowded train or bus. The following is the cost of going into the office as a percentage of your take home salary if you live within Toronto, but doesn’t include some big costs like parking if you have to pay it or grabbing the occasional Uber or Taxi:

Within Toronto, Ontario

Time to Re-Consider Commuting Costs

It shouldn’t break the bank to go to work and make a living. For most people, when you take a hard look at the cost of commuting, and consider that the median salary is about $60,000 a year (meaning, half of Canadians make more than this while half of Canadians make less), commuting just doesn’t make economic sense.

General Rule of Thumb: Commuting Costs

As a financial consultant, a common recommendation is to keep transportation costs including commuting, car payments, insurance, and fuel to around 10-15% of your monthly income after tax or net income. This is part of the broader 50/30/20 budgeting rule, where 50% of your income goes to necessities, 30% to wants, and 20% to savings and debt repayment. What this means is if you make $80,000 a year and commute into Toronto from Oakville by taking the GO train, you should not be paying any more than about $6000 a year for going into the office.

Statistics Canada reports that less than 10% of Canadians make more than $100,000 a year. Unless you are making a six-figure salary, you are likely nowhere near following the general rule of thumb when it comes to your commuting costs, unless you live within the City of Toronto (and have someone give you a house or pay for the roof over your head).

Opportunities to Save Money

Your best opportunity to save money when commuting to work is to find employment where you don’t have to commute. Some ‘financial experts’ will tell you to bring your coffee and pack your lunch, but this is not always practical, as anyone who has ever commuted will tell you. First, how many bags do you want to have to carry? You are already carrying your computer or briefcase; if you are a woman, you will have a purse, you probably have other things you need in a backpack, and now you need to carry a thermos of coffee and a lunch bag as well? Then there is the time you have to spend making and packing your coffee and lunch every day not to mention the cleanup of tupperware afterwards. No matter how disciplined you are the fact is most people buy their lunch and coffee, that’s just the way it is because people who commute have very long days and very long weeks. People get tired.

Commuting Costs Are Higher for Women

Commuting to work is more expensive for women than it is for men. Women’s clothes are generally much more expensive than men’s clothes. A woman’s professional wardrobe is more diverse and aligned with the season, whereas men tend to wear the same things in January as they do in July. Not only are women’s clothes more expensive, but they also need more care. Further, a woman who works remotely doesn’t have to spend as much money on makeup and cosmetics; men don’t have to consider these things.

Commuting’s Personal Finance Cost

Every nickel you pay to go into the office is a nickel you don’t have to put into your FHSA to buy your first home, your RRSP in case you want to retire one day, or your children’s RESP so they can have a future. The 50/30/20 rule where you save 20% to pay down debt and savings is completely inadequate especially when you consider your RRSP is 18%, 10% for your FHSA, and 7% for your RESP. You should be saving 35%, not 20% (I know, if only you could). I won’t bring up the $7,000 limit for your TFSA, which you should also be taking advantage of, that would be cruel. Truth is, people are spending more on commuting than they are on their future.

Consider the Alternatives to Commuting

The pandemic gave people the opportunity to see how much money they could save if they didn’t have to commute into work. Before the pandemic, people knew commuting was expensive, but it was just something they felt they had to pay for because there weren’t any alternatives. Today, more places than ever offer the opportunity to work remotely.

Many Canadians are learning how easy it is to work for American companies, either on a permanent or a contract basis, remotely while living in Canada. You don’t have to move to the United States anymore to work for an American company. This is a great arrangement for American companies because they can access the best talent in Canada while paying Canadians less than what they would need to pay an American resident (but still pay more than what Canadians get paid in Canada) and pay the Canadian person in Canadian dollars. No private American health care benefit costs to cover either. Besides, Canadian companies, like banks and technology firms, have been outsourcing Canadian work to countries like India for years; turnabout is fair play.

Before accepting any employment opportunity, consider the impact to your finances, ability to pay down your mortgage, and kind of house you and your family can have if your employer insists you come into the office.

If you lived in Whitby, and you could either take remote job A which pays $60,000 a year, or job B which requires you to commute to Toronto but pays $100,000 a year, and you have to take the 407ETR, which would be the better choice just on money alone? The answer is job A by over $10,000 a year (and that’s before we get into the massive amount of time you’d have to spend commuting every day, the impact to your health, and even the risk to your life). Let’s say you didn’t have to take the 407ETR, but you could take the GO Train into Toronto. Job B would still have to offer close to $90,0000 to compete financially with job A (but job B would still not be your choice because of all the difficulties and time expense that comes with commuting).

Commuting more often than not just doesn’t make financial sense anymore.

Political and Social Implications of Commuting

As more and more people come to understand the very high costs associated with commuting to work and witness those costs continuing to increase, they begin to make different choices that have profound political and social impacts.

All that money people pay to commute to work is going somewhere. It’s going to government in the way of taxes that you pay on everything including gasoline taxes and the carbon tax. When people don’t commute into Toronto or other big cities, government loose millions and millions of dollars in revenue. Governments need you in that car, on that bus, on that train. Empty downtown offices don’t generate the property taxes full offices do. Toronto is facing a $1.5 billion shortfall. Governments loose a lot of tax revenue when you don’t commute. Remote work is good for you, but bad for government.

Remote work is green work. All those thousands and thousands of cars inching along and frequently at a full stop on the 401 as people crawl into Toronto and crawl out again are burning fossil fuels and ruining our environment. Over 97% of the energy a car uses to take someone into the office is used to move the car, not the commuter. Are we moving people or cars? If governments cared about the environment, they would be promoting tax credits to empower people to work remotely, not forcing them to pollute the environment by forcing them into the office.

Remote work places less of a burden on housing, roads, hospitals, and infrastructure. When people don’t have to cluster in a few employment centres like Toronto and Vancouver, they can take advantage of Canada’s big open spaces and choose to live in communities where life is better, cheaper, and healthier. Remote work solves our housing affordability problem and goes a long way to solving Canada’s housing crisis.

Dozens of studies have demonstrated that remote workers are more productive and report higher efficiency. Without the distractions of a typical office environment and the ability to create a personalized workspace, many find it easier to focus and complete tasks. A study by Standford University found a productivity boost among remote workers equivalent to a full day’s work per week. Employees have improved morale and job satisfaction A Gallup poll indicated that remote workers feel more engaged in their jobs. For employers, remote work allows companies to hire the best talent regardless of geographical location. This leads to more skilled and efficient teams and reduced absenteeism.

Conclusion

Commuting to work is prohibitively expensive—more expensive than almost any other expense in your life. If you could take every dollar you spend on going into the office and put that towards saving for your house and your future, you and your family would be very secure. However, going into the office doesn’t just have a big financial impact; it also takes years off of your life, is the source of chronic stress, and impacts your well-being, not just on you but on your family and children as well.

Price of Commuting Lost Time, Lost Life

The decision to commute is a personal one, influenced by a variety of factors, including job opportunities, family needs, and lifestyle choices. But it’s important to be aware of the costs, both seen and unseen. As we navigate our daily lives, balancing work and personal life, it’s crucial to consider not just the financial implications but the impact on our time, our relationships, and our health.

In the end, it’s about finding a balance that works for you and your family. Maybe it’s negotiating remote work days or finding a job closer to home. Or perhaps it’s simply about making the most of the time you have, both on the commute and at home.

As the sun sets and the commuters return to their suburban homes, the journey reflects the choices we make and the prices we pay. It’s a reminder that in the pursuit of our careers and dreams, we must not lose sight of what truly matters: our health, our relationships, and our peace of mind.