… Use my Primate Rate Change Calculator and KNOW!

If you’ve ever watched the news, heard “rates are moving,” and felt your stomach drop a little—yeah, you’re not alone. Most Canadians don’t actually need more opinions about interest rates. They need clarity. That’s exactly what my Prime Rate Impact Calculator is built to do: turn prime-rate chatter into real numbers you can understand, stress-test, and use to make smart decisions—without spreadsheets, guesswork, or fancy finance jargon.

Here’s the thing: variable mortgages aren’t “good” or “bad.” They’re dynamic. And when something is dynamic, you need a tool that shows you what changes, what doesn’t, and what happens next. This calculator does that in seconds.

After the introduction, here are the exact topics covered:

Why it matters more than the headline rate

The big fork in the road: adjustable vs static payment variables

Real-life scenarios where the calculator saves you money (and stress)

A story-based walkthrough with a step-by-step example

How clients can use it to make confident decisions

How I can help you apply the output to your mortgage strategy

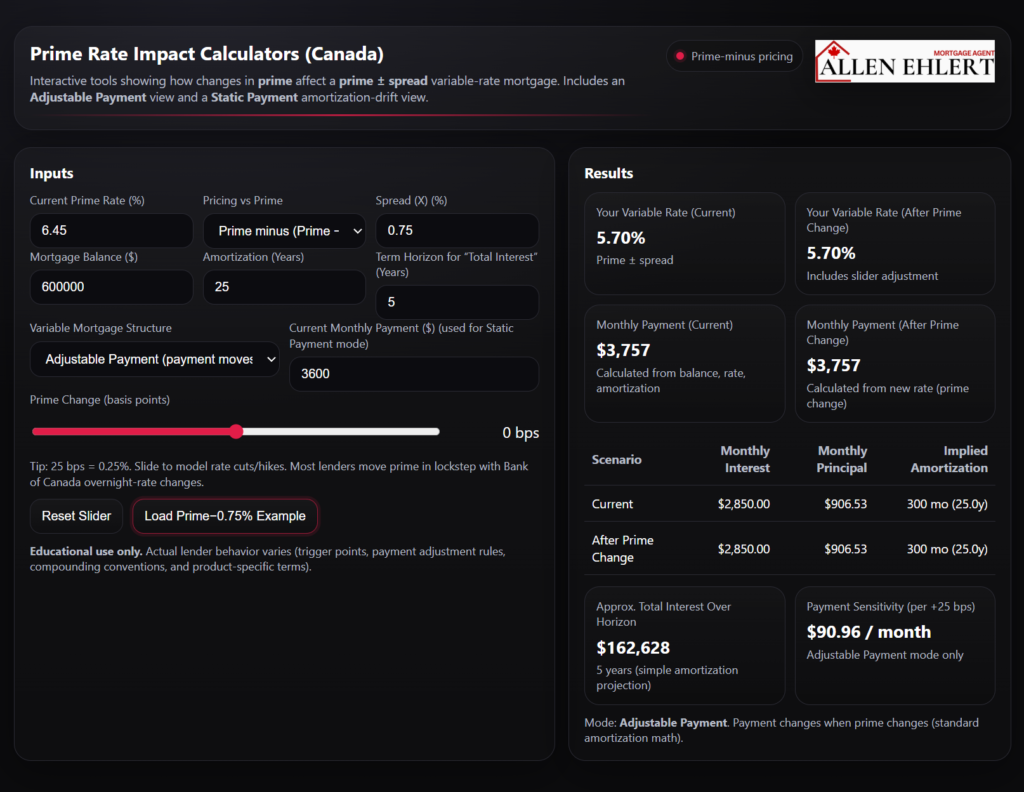

What the Calculator Does

This calculator shows you how changes in Canada’s prime rate impact a variable-rate mortgage priced as prime ± a spread (like Prime – 0.75% or Prime + 0.50%). It does three things most people never see clearly:

- It converts “prime moved” into your actual mortgage rate

- It shows how payments and amortization behave under rate changes

- It breaks down interest vs principal, so you can see what’s really happening behind the scenes

You’re not just looking at a rate. You’re watching the mortgage behave.

When You’d Use This Calculator

You use this tool any time you want to answer questions like:

- “If rates go up another 0.50%, what happens to my payment?”

- “If rates drop 1.00%, how fast do I start saving?”

- “My payment isn’t changing… so why does my mortgage feel like it’s going nowhere?”

- “Am I at risk of my amortization stretching out?”

- “Should I increase my payment now or wait?”

- “Is my variable mortgage adjustable-payment or static-payment—and what does that mean for me?”

If you’ve got a variable mortgage (or you’re considering one), this calculator is basically your dashboard.

Why This Matters More Than the Headline Rate

Most people shop mortgages the way they shop gas: “What’s the number today?”

But a mortgage isn’t gas. It’s a long-term contract with moving parts—especially when prime changes. The real risk (and opportunity) isn’t the starting rate. It’s how the mortgage behaves when the rate environment shifts.

That’s why this calculator focuses on:

- Payment impact

- Principal progress

- Amortization drift

- Interest cost over time

In other words: it shows you whether your mortgage is quietly becoming more expensive—or quietly getting easier.

The Big Fork in the Road: Adjustable vs Static Payment Variables

This is one of the most misunderstood parts of variable mortgages in Canada.

Adjustable Payment Variable (ARM)

When prime changes, your payment changes. Clean and obvious. If rates rise, payment rises. If rates fall, payment falls.

Static Payment Variable (VIRM)

Your payment stays the same, but the math underneath changes. If rates rise:

- more of your payment goes to interest

- less goes to principal

- amortization can stretch out

- and in extreme cases, you can hit a trigger where the payment doesn’t cover interest

This calculator makes that difference painfully clear—in a good way.

NOTE: Trigger Rate/Point

Static-payment variables have trigger rates

In a static-payment variable:

- The interest rate changes

- The payment stays fixed

- As rates rise, more of the payment goes to interest

- If rates rise far enough, the payment may no longer cover the interest

That specific rate — where the entire payment is consumed by interest and principal repayment drops to zero — is called the trigger rate.

Once reached, lenders intervene (the trigger point) by requiring one or more of the following:

- A payment increase

- A lump-sum payment

- A re-amortization or conversion

This risk exists because the payment does not move.

Why adjustable-payment variables do not have trigger rates

In an adjustable-payment variable:

- The interest rate changes

- The payment changes immediately

- Amortization stays intact

Because the payment adjusts upward as rates rise, interest is always covered and principal repayment continues. As a result, there is no trigger rate or trigger point in this structure.

Clean takeaway

- Static-payment variable → can have a trigger rate

- Adjustable-payment variable → no trigger rate

This is one of the most important—and least understood—distinctions in Canadian variable mortgages, and it’s exactly why modelling both structures side-by-side (as your calculator does) is so valuable.

Scenarios Where This Calculator Can Save You Money (and Stress)

Here are practical situations where you’d use it immediately:

At renewal when your lender pushes you into “whatever’s easiest”

Use the calculator to compare a variable option against your current structure and see what rate changes would do.

When you’re choosing between fixed and variable

Instead of guessing, you can simulate rate moves and see the risk range.

When you have a static-payment variable and your principal isn’t moving

This tool will show you whether your amortization is drifting and by how much.

When you’re thinking about prepayments or increasing your payment

You can model the impact and decide whether it’s worth it now—or later.

When you’re buying and want to understand affordability under real conditions

Not “best-case.” Real-case.

A Story to Illustrate It

Meet Jason and Priya. They’re good people—smart, organized, both working steady jobs. They picked a variable mortgage because the rate was lower and it seemed flexible. Easy win, right?

A year later, they call me and say:

“Allen… our payment hasn’t changed, but it feels like we’re barely paying anything off.”

That line tells me everything. They’re likely in a static-payment variable and their rate has risen enough that most of their payment is being eaten by interest. They’re not in trouble—but they’re flying blind.

So we pull up the Prime Rate Impact Calculator and do the simplest thing: we make the mortgage visible.

Step-by-Step Scenario Example Using the Calculator

Here’s exactly how Jason and Priya used it—so you can do the same.

First: Set the foundation

- Enter the current prime rate (whatever prime is today)

- Select Prime minus if your mortgage is discounted

- Enter your discount (example: 0.75%)

Second: Enter your mortgage reality

- Enter your mortgage balance

- Enter your amortization (example: 25 years)

- Set the term horizon (example: 5 years)

Third: Choose your variable structure

- If your payment changes when rates change, choose Adjustable Payment

- If your payment stays the same, choose Static Payment and enter your current payment

Fourth: Stress-test prime changes

- Move the slider +25 bps, then +50 bps, then +100 bps

- Watch what happens to:

- Monthly interest

- Monthly principal

- Implied amortization

- Warnings (if your payment stops covering interest)

Fifth: Interpret what you’re seeing

Jason and Priya saw something that finally clicked:

Their payment didn’t change—but their principal repayment collapsed as rates rose. Their amortization extended. That’s why it felt like “nothing was happening.”

Sixth: Make a strategy decision

Now they had options:

- Increase the payment to restore amortization

- Make a lump sum to reduce balance and interest drag

- Restructure at renewal into a product that fits their risk tolerance

- Or plan a conversion strategy if that aligns with their goals

The calculator didn’t “sell” them anything. It gave them clarity. And clarity makes decisions easier.

How Realtors Can Use This With Clients

If you’re a realtor, this tool is gold because it helps you:

- Set realistic expectations about monthly payments and risk

- Reduce buyer panic when rate headlines hit

- Frame affordability conversations responsibly

- Build trust by showing numbers, not opinions

Here’s the move:

Use it during buyer consultations to show what “a few rate changes” actually looks like for payment and amortization. Your clients will feel calmer—and better prepared to buy.

How Clients Can Use This to Make Confident Decisions

If you’re a borrower, this calculator helps you:

- Understand what you signed up for

- Test your budget against rate changes

- Decide whether to increase payments

- Avoid the slow-motion surprise of amortization drift

- Walk into renewal conversations with leverage

Instead of hoping things work out, you’ll know what the numbers say.

How I Help You Turn Calculator Outputs Into a Real Strategy

Numbers are great—but strategy is what changes outcomes.

If you want to use the calculator properly, I can help you:

- Identify whether your variable is static or adjustable

- interpret amortization drift and trigger risk

- Build a plan for payment increases or prepayments

- Compare fixed vs variable using realistic scenarios

- map out renewal and switch options (and avoid ugly penalties)

- structure your mortgage around your actual life—cash flow, goals, and risk tolerance

You don’t need to become an economist to make smart mortgage decisions. You just need the right tool—and a professional who can translate the results into action.

Allen’s Final Thoughts

Prime rate moves don’t have to feel like a rollercoaster. When you can see exactly how your mortgage behaves—payment, principal, amortization, and interest cost—you stop reacting to headlines and start making decisions with confidence.

That’s why I built the Prime Rate Impact Calculator: to give you a simple, visual way to stress-test your mortgage and choose a strategy that fits your real life. If you want, send me your current mortgage details and I’ll help you run the scenarios properly, explain what the results actually mean, and build a plan that makes your mortgage work for you—not the other way around.