Collateral mortgages—such as the TD Home Equity FlexLine, BMO Homeowner ReadiLine, and Scotiabank STEP mortgage—differ significantly from conventional mortgages in several important ways. Understanding these differences can help homeowners decide which type best aligns with their financial strategies and personal goals.

Collateral and Readvanceable Mortgages

How Collateral and Readvanceable Mortgages Connect

Borrowing Capacity and Re-Advancement of Funds

Portability and Flexibility in Changing Lenders

Legal and Administrative Costs

Collateral and Readvanceable Mortgages

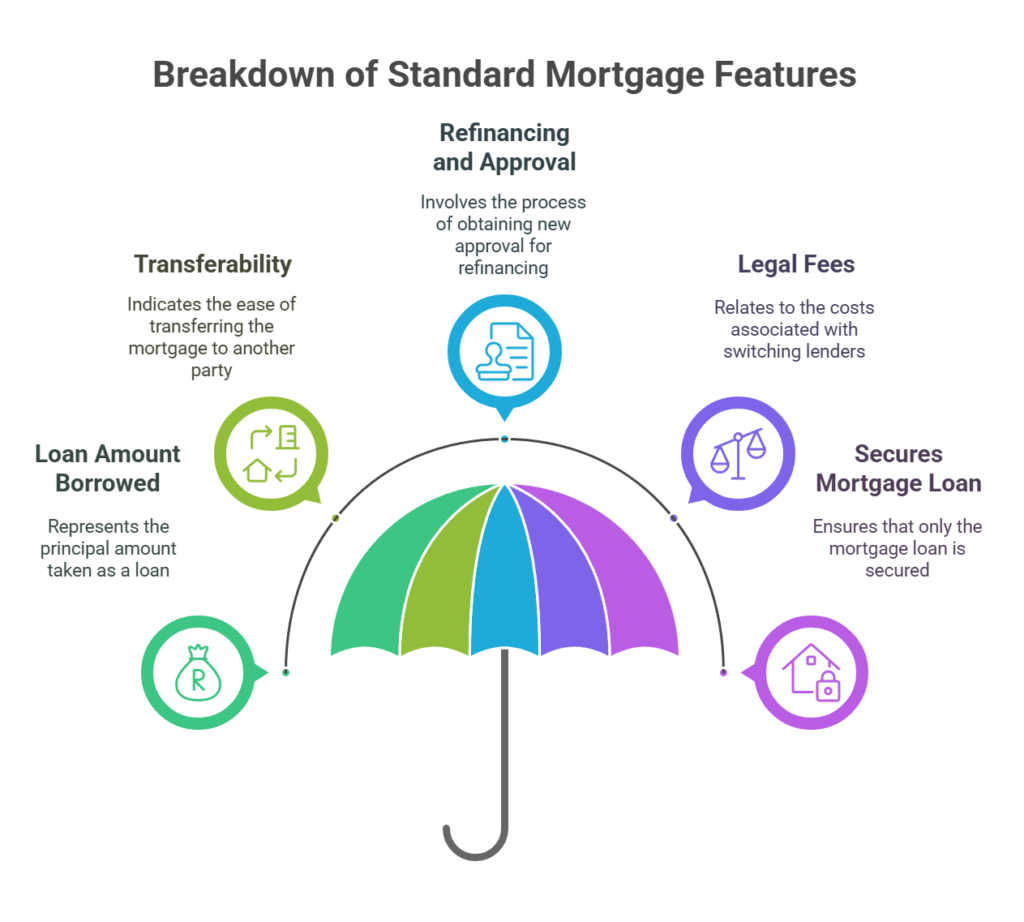

As these are collateral mortgages, they are flexible mortgage products where a property is pledged as collateral security for a loan that can potentially exceed the initial amount borrowed. This type of mortgage is registered on title for an amount typically higher than the actual borrowed funds. It enables the homeowner to access additional funds through refinancing or by setting up additional loan facilities without needing a new legal mortgage registration.

A readvanceable mortgage combines a mortgage with a line of credit component—often called a Home Equity Line of Credit (HELOC). As you pay down your mortgage principal, your available credit line automatically increases, allowing immediate access to equity without additional applications or legal work.

How Collateral and Readvanceable Mortgages Connect

Collateral mortgages provide the legal structure that makes the readvanceable feature possible.

Readvanceable mortgages specifically leverage the collateral charge to continuously readvance credit as equity grows.

Key benefits of readvanceable mortgages include flexibility, convenience, and the ability to leverage home equity strategically. Homeowners can easily access funds for investments, renovations, or to implement financial strategies such as the Smith Manoeuvre. Furthermore, because the mortgage is registered as a collateral charge, borrowers can draw on the built-up equity without incurring additional legal fees each time they access funds.

Structure and Flexibility

A collateral mortgage differs primarily in its structure and flexibility. Unlike a conventional mortgage, which registers only the exact amount borrowed, a collateral mortgage registers a higher amount—often up to or beyond the home’s current value. This higher registration facilitates easier access to additional funds without needing to re-apply or incur additional legal fees later.

Collateral mortgages typically combine multiple financial products into one flexible lending solution. For instance, with products like the TD Home Equity FlexLine or Scotiabank STEP mortgage, homeowners can simultaneously hold a fixed-rate mortgage, variable-rate mortgage, and a Home Equity Line of Credit (HELOC) under a single registered collateral charge.

In contrast, a conventional mortgage involves a fixed loan amount, defined repayment schedule, and does not automatically offer the ability to easily tap into the equity without refinancing, re-applying, or incurring additional costs.

Borrowing Capacity and Re-Advancement of Funds

Collateral mortgages offer borrowers the ability to continually access equity without requalifying, as long as they remain within the initial registered limit. As borrowers pay down the principal, available credit increases automatically, allowing ongoing access to funds through the HELOC portion. This feature, known as “re-advancement,” provides significant flexibility and is particularly advantageous for financial strategies such as debt consolidation, renovations, or investment purposes.

By contrast, conventional mortgages don’t automatically replenish credit. Once repaid, any new borrowing typically involves refinancing and requalification, with associated costs such as legal fees, appraisal fees, and possible penalties.

Portability and Flexibility in Changing Lenders

Collateral mortgages have specific implications for homeowners seeking to switch lenders at mortgage renewal. Since collateral mortgages are individually structured products, changing lenders can be more complex, often requiring legal fees, new appraisals, and additional paperwork. Consequently, borrowers with collateral mortgages may face barriers or additional costs when shopping around at renewal.

On the other hand, conventional mortgages are often simpler to transfer between lenders upon renewal, as they typically have standardized terms and conditions. This simplicity can allow homeowners to more easily take advantage of lower interest rates or better terms available in the marketplace.

Legal and Administrative Costs

Collateral mortgages generally involve higher initial legal and registration fees due to the broader scope and complexity of registering a higher amount on the property title. However, once established, they may save money in the long term by eliminating the need for repeated refinancing costs, provided borrowers regularly access their home equity.

Conversely, conventional mortgages usually incur lower upfront costs because only the actual loan amount borrowed is registered on title. However, refinancing to access additional equity later involves extra costs each time this process is repeated.

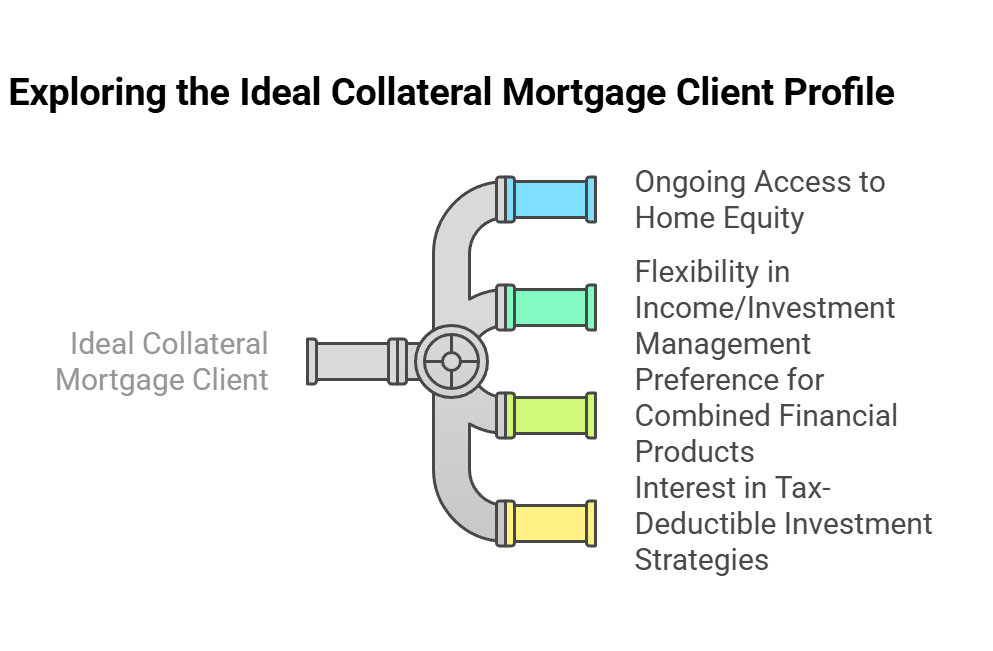

Ideal Client Profiles

Collateral mortgages like the the TD Home Equity FlexLine, BMO Homeowner ReadiLine, and Scotiabank STEP mortgage are ideal for homeowners who:

- Anticipate needing ongoing access to home equity.

- Desire flexibility in managing fluctuating incomes or investments.

- Prefer a combined financial product for simplicity and consolidated financial management.

- Want to leverage strategies such as the Smith Maneuver for tax-deductible investments.

A conventional mortgage suits homeowners who:

- Prefer simplicity, straightforward repayment, and predictable structure.

- Do not anticipate regularly accessing home equity.

- Value ease of lender portability at mortgage renewal for competitive interest rate shopping.

Summary

Understanding these differences is essential when choosing between collateral and conventional mortgages. Collateral mortgages offer substantial flexibility, ongoing equity access, and suitability for sophisticated financial strategies, but they come with complexities and potential renewal limitations. Conventional mortgages offer simplicity, easier portability, and predictability, but lack built-in equity access and flexibility.

Ultimately, the right choice depends on your financial priorities, lifestyle, and long-term goals.