.. Preparing for Hard Times in the Housing Market

Life has its ups and downs, and so do economies. Just like the seasons change, so too do financial cycles—sometimes we’re basking in the sunshine of growth, and sometimes we’re caught in the storm clouds of a recession. The truth is, hard times are not a fluke—they’re a normal, expected part of the economic cycle. If you own a home, or you’re planning to, being prepared for those stormy patches can make all the difference between riding them out comfortably or getting knocked off course.

Before I dive in, here’s what I’ll cover:

Contingency Reserves and Management Reserves

Why Overextending Is Dangerous

Housing Costs: Gross vs. Net Income

Employment Stability and Mortgage Planning

Fixed vs. Variable Mortgages: The Trade-Offs

Putting It Into Practice: Realtors and Clients

The Normalcy of Recessions

Recessions are like winter—they come whether you want them to or not. Historically, Canada has seen recessions roughly every 7 to 10 years, though the severity and length vary. The Great Recession of 2008–09 hit like a blizzard, while the COVID-19 downturn in 2020 was short but intense, more like an ice storm that knocked out power but passed quickly.

While COVID, Tariffs, and the like seem to be one offs or ‘black swans’, from an historical perspective they really aren’t. Things we can’t anticipate are always going to occur. That’s why I always begin every discussion about the future by saying, ‘no one has a crystal ball.’

If you accept that these hard times are inevitable, then you stop fearing them and start planning for them. That’s where financial resilience comes in. It is also why I walk my clients through a series of ‘what if’ questions to help them to start to think about, anticipate and plan for bad times.

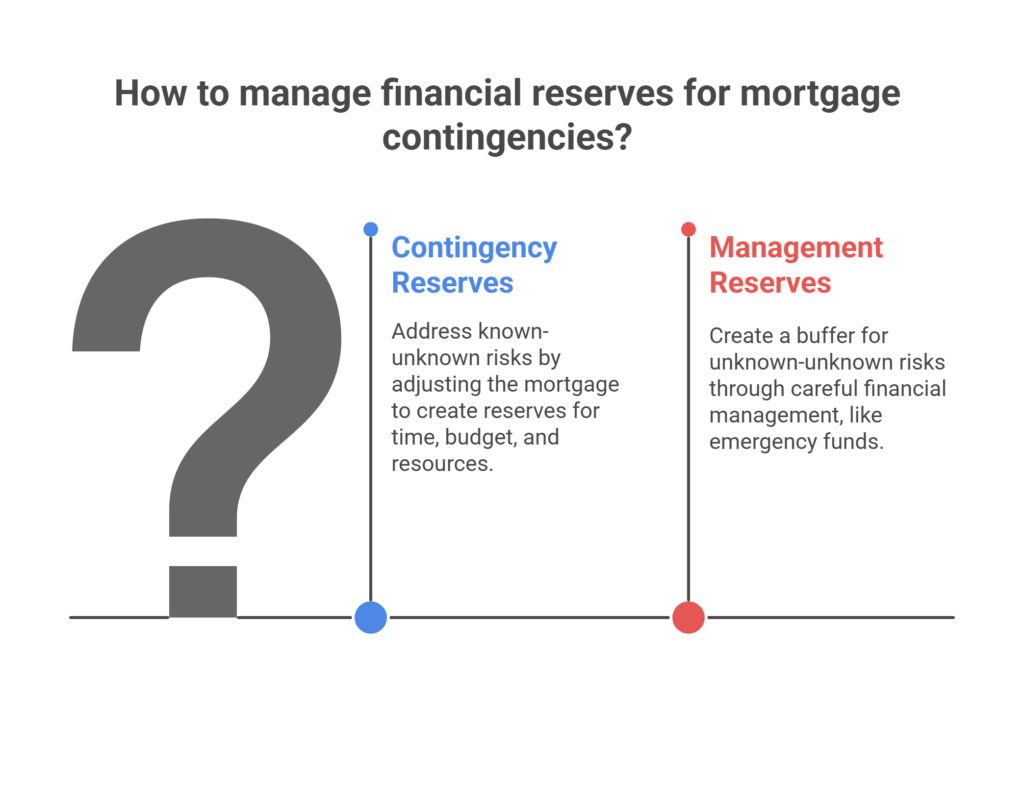

Contingency Reserves and Management Reserves

Essentially, I’m talking about incorporating Contingency Reserves and Management Reserves into Mortgage Financial Planning.

Contingency Reserves are risks I’ve worked with the client to identify in advance. Let’s call them our ‘known-unknowns’ Once we’ve identified them, I suggest an alternation or adjustment of their mortgage to create a contingency reserve of time, budget, and resources to address these contingencies.

Then there are management reserves for risks we cannot anticipate. These I’ll call the ‘unknown of unknowns’. No one can plan for them directly, but through careful mortgage financial management, I create a buffer in case the sky falls in. Management reserves are like the “break glass in case of emergency” funds — you hope never to use them, but they’re there when the truly unexpected happens.

The Job Market Reality Check

During downturns, companies tighten belts, cut costs, and unfortunately, people lose jobs. Even strong performers can find themselves downsized because of nothing more than market forces. Think about 2020: many restaurants, gyms, and travel-related businesses closed their doors overnight.

This is why preparing isn’t about paranoia—it’s about prudence. When you plan your mortgage, you’re not just planning for today’s paycheque; you’re hedging against tomorrow’s “what if.”

Why Overextending Is Dangerous

It’s tempting to buy the biggest house the bank says you qualify for. But just because you can doesn’t mean you should. Overextending yourself—taking on a mortgage that eats up too much of your income—leaves you vulnerable when the economy takes a turn.

Imagine you’re on a rollercoaster with no lap bar. That’s what it feels like when housing costs are too high and your income suddenly dips. A smaller, more affordable mortgage is like that lap bar: it keeps you safe when the ride gets bumpy.

Housing Costs: Gross vs. Net Income

Financial planners in the U.S. often say, “Keep your housing costs under 30% of gross income.” That might work in Dallas or Phoenix, but here in Canada, where personal taxes bite much deeper, that advice doesn’t translate.

Instead, I encourage my clients to focus on 33% of net income—your actual take-home pay. It’s a more realistic measure of what you can comfortably afford without sacrificing essentials like food, transportation, and saving for a rainy day.

Employment Stability and Mortgage Planning

When you’re choosing a mortgage, ask yourself: “How stable is my income?” If you’re in government work or a unionized role, your job may be relatively secure. But if you’re in construction, tech, or sales, you may face more volatility.

This isn’t about being pessimistic—it’s about being honest. Factoring in employment stability helps you choose the right mortgage product and avoid sleepless nights when the economy shifts.

Fixed vs. Variable Mortgages: The Trade-Offs

Here’s where the rubber meets the road. Fixed-rate mortgages offer peace of mind—your payments don’t change, no matter what the Bank of Canada does. But that security comes with a big catch: penalties. Break a 5-year fixed mortgage after only two years, and you could be staring down a penalty in the tens of thousands.

Variable-rate mortgages, on the other hand, move with the market. Rates might rise, and your payments could increase. But if life throws you a curveball and you need to sell, refinance, or break your mortgage, the penalty is usually just three months’ interest—a fraction of the fixed-rate sting.

Putting It Into Practice: Realtors and Clients

Here’s a quick story. I once worked with a young couple, both working in the airline industry. They were excited to buy their first home, and the bank told them they could “afford” a $900,000 property. I walked them back and suggested something closer to $750,000, which kept their payments below 33% of net income.

That’s why only my calculators show not only what mortgage you can get, but what mortgage you can afford.

SEE MORE: Allen Ehlert’s Calculators

Sure enough, within two years, one of them was laid off when travel demand collapsed. Because they’d chosen wisely, they were able to keep their home on one income. Had they maxed out, they would’ve been forced to sell.

For realtors: Encourage clients to think beyond the sticker price and consider job security when searching for homes.

For clients: Look past what you’re approved for and ask yourself, “What would I still be comfortable paying if things went sideways?”

Allen’s Final Thoughts

Hard times aren’t an “if”—they’re a “when.” The question is whether you’ll be ready. By keeping housing costs in check, considering job stability, and choosing the right mortgage type for your situation, you build resilience. Think of it as putting on your financial seatbelt. You might not need it every day, but when the economy hits a pothole, you’ll be glad you have it.

As your mortgage agent, I’m here to help you think through these scenarios. I don’t just crunch the numbers—I look at your whole picture: your job, your income, your risk tolerance, and your future goals. Whether it’s finding the right mortgage, walking you through penalty risks, or giving you a second opinion before you buy, my role is to make sure you’re secure not just today, but five, ten, or twenty years from now.

When hard times come—and they will—you’ll know you’ve got someone in your corner.