… Position, Priority, and the Power—and Peril—of Layered Debt

Second mortgages sit in one of the most misunderstood corners of Canadian real estate finance. They’re powerful, flexible, and sometimes exactly the right tool. They’re also easy to misuse, easy to misunderstand, and unforgiving when structured poorly.

If you work in finance, real estate, or lending—or you’re a homeowner being advised by one of those professionals—you need to understand not just what a second mortgage is, but how mortgage position, lender policy, and legal priority quietly control what’s possible… and what can go very wrong.

Let’s get into it!

Mortgage Position: What It Is and Why It Matters

What a Second (or Third) Mortgage Is

Who Offers Second Mortgages and in What Forms

Chartered Banks vs Monolines vs Alternative vs Private Lenders

How Collateral Mortgages Impact Second Mortgages

What Needs to Be Done to Get a Second Mortgage

The Limits and Costs of Second Mortgages

What Happens If You Skip First-Lender Permission

Second Mortgages vs Other Refinance Strategies

Mortgage Position: What It Is and Why It Matters

Mortgage position is about priority on title, not intent, not fairness, and not what you “meant” to do.

When multiple mortgages are registered against a property, they are ranked by legal priority:

- First position gets paid first

- Second position gets paid only after the first is fully satisfied

- Third position waits behind both

This order controls:

- Who gets paid in enforcement

- Who carries the most risk

- Who has leverage in negotiations

- Who sets the rules

Position is established at registration and reinforced through legal agreements—not by handshake, assumption, or borrower preference.

What a Second (or Third) Mortgage Is

A second mortgage is any mortgage registered behind an existing first mortgage. A third mortgage sits behind both.

They are not inherently risky or predatory. They are simply junior claims on the same asset.

What changes as you move down the stack:

- Risk increases

- Interest rates rise

- Terms shorten

- Lender flexibility drops

- Exit planning becomes critical

A second mortgage doesn’t replace the first. It layers on top of it.

Who Offers Second Mortgages and in What Forms

Second mortgages exist in several common structures:

- Fixed-term second mortgages

- Interest-only second mortgages

- Short-term bridge-style seconds

- Home equity loans in second position

- HELOCs in second position (less common)

They are offered by different parts of the lending ecosystem, each with very different rules.

Chartered Banks vs Monolines vs Alternative vs Private Lenders

This is where many professionals—and clients—get tripped up.

Chartered banks

- Prefer to hold both first and second positions

- Rarely allow external seconds

- Often use collateral charges

- Risk-averse on priority sharing

Monoline lenders

- Focus on first mortgages

- Most allow seconds behind their own first mortgage, some allow seconds behind another lender’s first, but many do not

- Tend to restrict additional encumbrances

- Policy-driven, not discretionary

Alternative (B) lenders

- More flexible on structure

- More open to second mortgages, so easier to get but that ease comes with higher rates

- Still require first-lender consent (postponement agreement)

- Focus on equity, income reasonableness, and exit

Private lenders

- Most common source of second and third mortgages (so easiest to get but most expensive)

- Equity-driven underwriting

- Shorter terms, higher rates

- Very sensitive to title position and consent

- Need a strong exit strategy

The further you move from prime, the more structure matters more than credit score.

How Collateral Mortgages Impact Second Mortgages

Collateral mortgages change the game.

Unlike standard charges, collateral mortgages are often registered for:

- 125%–150% of property value

- Future advances

- Multiple obligations

This means:

- Even if the balance is low, the registered charge may fully occupy title

- The first lender can advance more funds later

- Second lenders face dilution risk

Without a postponement agreement, a second mortgage behind a collateral charge is often legally weak or practically unenforceable.

This is why collateral mortgages quietly shut down many second-mortgage strategies.

What Needs to Be Done to Get a Second Mortgage

At a minimum, a legitimate second mortgage requires:

First, confirmation of available equity based on appraised value (usually 80% loan to appraised value but may be as low as 65% depending on property and lender policy)

Second, review of the first mortgage type and charge

Third, first-lender consent, often via a postponement agreement

Fourth, a second lender willing to accept the risk

Fifth, a clear exit strategy

This is not a checkbox exercise. It’s coordination between:

- Lenders

- Lawyers

- Borrower expectations

- Policy constraints

The Limits and Costs of Second Mortgages

Second mortgages come with trade-offs:

- Higher interest rates

- Shorter terms

- Setup and legal fees

- Lender fees

- Renewal or exit pressure

Loan-to-value limits are tighter, and not all equity is considered usable.

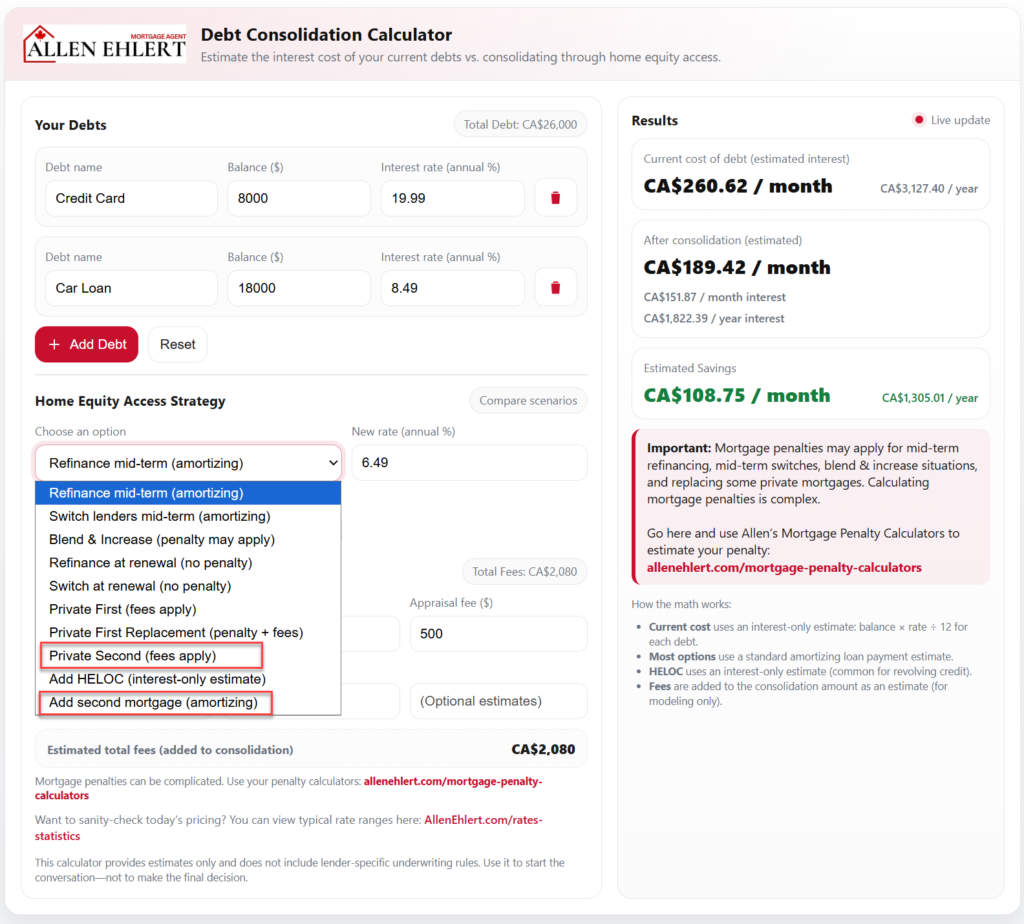

See the Debt Consolidation Calculator. In the ‘Home Equity Access Strategy’ panel, select either Private Second or Add Second Mortgage (amortizing) to discover the different types of fees depending on structure that could be applicable.

Second mortgages are best viewed as tools, not long-term foundations.

What Happens If You Skip First-Lender Permission

This is one of those questions where the legal answer and the practical outcome line up very tightly — and not in a good way.

Short answer:

You generally cannot safely or effectively place a second mortgage behind another lender’s first mortgage without a postponement agreement.

If it happens at all, it is almost always defective, unenforceable in practice, or immediately vulnerable.

Let’s unpack why.

What a postponement agreement actually does

A postponement agreement is not a courtesy document. It is the legal instrument that:

- Confirms priority on title

- Acknowledges the existence of the second lender

- Limits (or clarifies) the first lender’s rights ahead of the second

- Makes the second mortgage financeable and enforceable

Without it, the second lender has no protected priority — regardless of how the mortgage is registered.

What happens if a second mortgage is registered anyway

1. Registration does not equal enforceable priority

Land registry systems record documents; they do not validate lender consent.

So even if:

- The second mortgage appears on title

- The borrower signed valid documents

The first lender’s charge still dominates — especially if it is collateral.

2. The first lender can legally wipe out the second

Without a postponement agreement, the first lender can:

- Advance additional funds under a collateral charge

- Enforce default remedies

- Power of sale or foreclose

- Apply proceeds entirely to their own debt

The second lender may receive nothing, even if equity existed at the time of registration.

3. The second lender may have no right to notice

In many cases, without a postponement agreement:

- The first lender has no obligation to notify the second lender of default

- Enforcement can proceed without warning

- The second lender loses procedural protections

This is why sophisticated lenders simply won’t fund without consent.

4. Most lawyers will not close this deal

In real practice:

- The borrower’s lawyer will flag the issue

- The second lender’s lawyer will refuse to proceed

- Title insurers will decline coverage

If the deal closes anyway, it’s often:

- A rogue private lender

- A high-risk, high-rate transaction

- Or a structure that collapses at the first sign of trouble

Why collateral mortgages make this even worse

If the first mortgage is collateral:

- The registered amount often exceeds the current balance

- Future advances are permitted

- Priority is intentionally expansive

Without a postponement agreement, the second mortgage is not just junior — it is functionally unsecured.

From a risk standpoint, it behaves less like a mortgage and more like an unsecured loan with false comfort.

Regulatory and professional consequences

From a mortgage professional’s perspective, this structure raises serious red flags:

- Disclosure risk: Borrowers often don’t understand the implications

- Suitability concerns: The second mortgage may be illusory

- Enforcement risk: The lender cannot realistically recover funds

- Compliance exposure: Especially in regulated private lending

This is why reputable brokers avoid these deals entirely.

The professional takeaway

Putting a second mortgage behind another lender’s first without a postponement agreement is:

- Legally fragile

- Practically dangerous

- Professionally indefensible

If you ever hear:

“We’ll just register it — it should be fine”

That’s a signal to stop, not proceed.

What should be done instead

A competent mortgage strategy would explore:

- Obtaining first-lender consent properly

- Restructuring or refinancing the first mortgage

- Using a second lender that requires a postponement

- Timing equity access at renewal

- Considering a replacement or blended structure

This isn’t about creativity — it’s about respecting how mortgage priority actually works.

Second Mortgages vs Other Refinance Strategies

A second mortgage is not always the best move.

Alternatives include:

- Refinancing the first mortgage

- Blending and extending

- Replacing a collateral charge

- Using a HELOC

- Waiting for renewal

- Short-term bridge financing

A second mortgage makes sense when:

- You want to preserve a favourable first rate

- The need is temporary

- The equity is strong

- The exit is clear

- The structure is intentional

A Story From the Trenches

Imagine this.

Sam and Priya own a home valued at $1.2M. They owe $540,000 on a collateral mortgage with a major bank. Their rate is excellent, locked in two years ago.

Sam’s business needs $150,000 to bridge cash flow after a delayed contract. A refinance would trigger penalties and a higher rate.

A private lender offers a second mortgage—quick, interest-only, one-year term.

Here’s what goes right:

- Equity supports the loan

- The purpose is temporary

- The exit is planned

Here’s what nearly goes wrong:

- The bank’s collateral charge is registered at $900,000

- Without consent, the second lender would sit behind a charge that already fills title

- The deal almost closes without a postponement agreement

A professional intervention pauses the deal, secures consent, restructures the priority, and saves everyone from a legal mess.

Same numbers. Very different outcome.

Allen’s Final Thoughts

Second mortgages are not “bad” loans. They are advanced tools in a layered financial system.

When used thoughtfully, they:

- Preserve favourable first mortgages

- Solve timing problems

- Create flexibility

- Protect long-term strategy

When used carelessly, they:

- Create false security

- Expose lenders and borrowers

- Collapse under enforcement

- Damage professional credibility

This is where I come in.

As a mortgage agent, my role isn’t just to “find financing.” It’s to:

- Interpret lender policy

- Coordinate legal structure

- Stress-test exit plans

- Protect clients and referral partners from invisible risk

Whether you’re a financial professional advising a client, or a homeowner trying to make a smart decision under pressure, second mortgages demand structure, not shortcuts.

And that’s exactly what I help bring to the table.